Concerns raised on the Strait of Hormuz with the IRGC announcing ban on US Israel and European vessels - Newsquawk US Opening News

- Iran's Deputy Foreign Minister says Iran has not sent any messages to the US to end the conflict, but are instead focused on self defence efforts, according to Sky News Arabia.

- Deputy Commander of the Iranian Army Central Command said Iran has not closed the Strait of Hormuz; IRGC struck a US oil tanker while announcing US, Israeli and European vessels are not allowed through the strait.

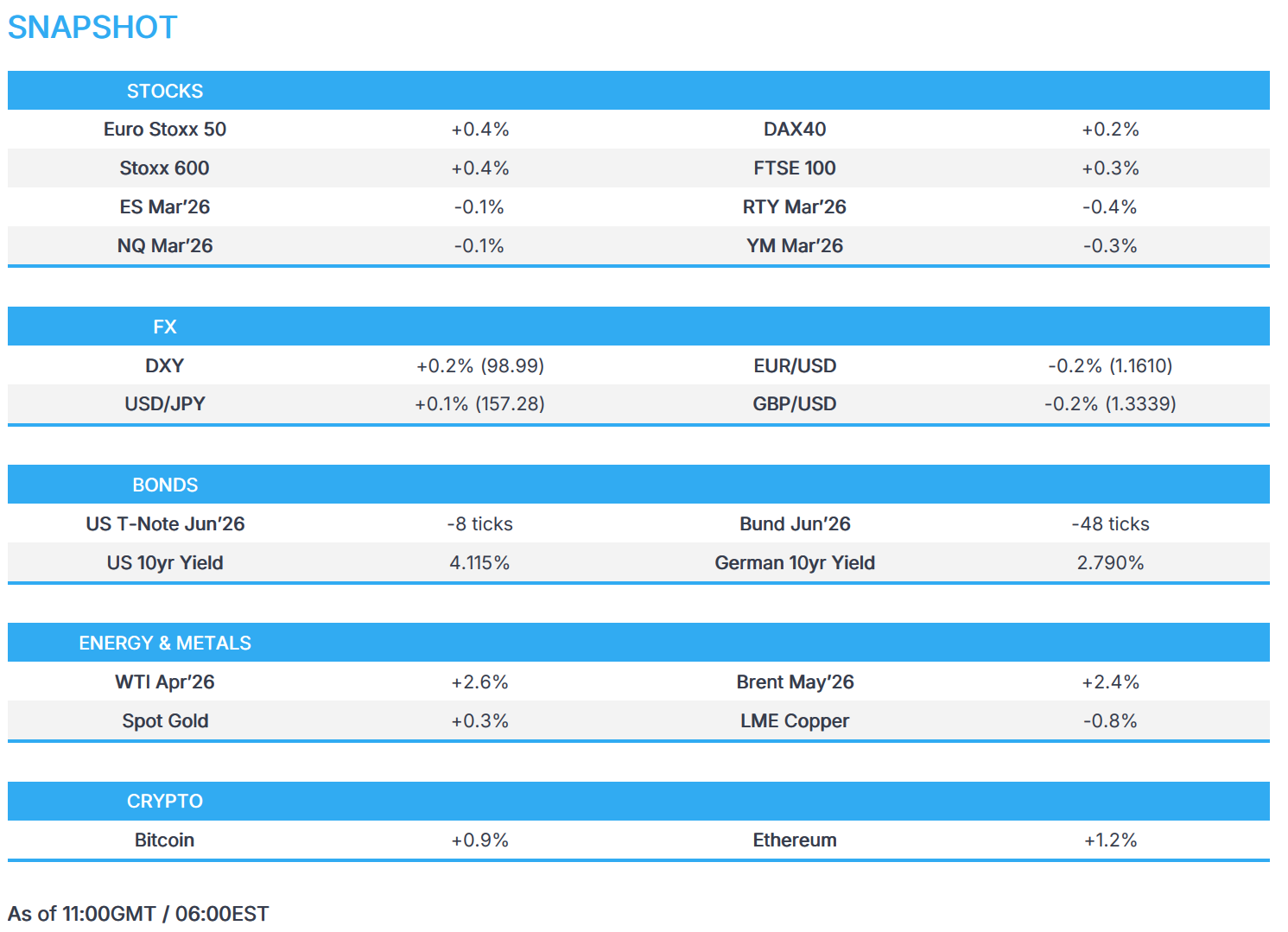

- European bourses trade mixed, STMicroelectronics surges on new chip; US equity futures softer despite positive AVGO earnings.

- DXY back on a firmer footing, antipodeans lag on China's new growth target and metals prices.

- Fixed benchmarks lower as energy prices continue to drive price action.

- Crude benchmarks remain firmer; Spot gold trades slightly firmer, whilst base metals are lower after China forecasts lowest GDP figure since 1991.

- Looking ahead, highlights include US Challenger Job Cuts (Feb), US Export/Import Prices (Jan), Jobless Claims, South Korean CPI (Feb), ECB Minutes (Feb), Speakers including ECB President Lagarde & Fed's Bowman, Earnings from Marvell, Costco, Kroger & Victoria's Secret.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) are mixed, with the IBEX 35 (+1.0%) leading while the SMI (-0.2%) lags slightly as distributor Kuehne+Nagel (-1.9%) weighs on the index.

- European sectors are tilted positively, with Utilities (+1.1%) outperforming while Basic Resources (-0.6%) sit at the bottom of the pile despite gains in metal prices. Technology (+0.8%) has been benefiting today after STMicroelectronics (+5.6%) announced a new generation of MCUs to boost performance of tiny smart devices while meeting extreme cost, size and power limitations.

- US equity futures (NQ/ES -0.1%, RTY -0.4%) are slightly lower. Broadcom (+7.0% pre-market) reported quarterly earnings and revenue above expectations, and issued stronger-than-expected revenue guidance, driven by robust demand for AI chips.

- Foxconn (2317 TT) February (TWD) Revenue 596.8bln, +8.1% Y/Y; (prev. 730bln in January, +36% Y/Y); noted visibility into Q1 aligns with market expectations.

- JD.Com (JD) Q4 2025 (USD): EPS 0.08 (exp. 0.07), Revenue 50.4bln (exp. 50.7bln); announces annual dividend of USD 0.50/ordinary share or USD 1/ADS.

- Broadcom Inc. (AVGO) Q1 2026 (USD): Adj. EPS 2.05 (exp. 2.02), Revenue 19.3bln (exp. 19.22bln). To buy back shares for USD 10bln.

- NVIDIA (NVDA) reportedly refocuses TSMC (2330 TT) capacity as export controls stall China sales in which it is shifting output away from H200s intended for the Chinese market to Vera Rubin products, according to FT.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is mildly firmer this morning and currently trades within a 98.66 to 99.20 range; upside which follows on from some mild pressure in the prior session, as investors favoured risk assets. Haven inflow have resumed given the overall environment has not changed – the Gulf remains at war, and the Strait of Hormuz remains effectively shut, and there are currently little signs of easing. It is worth highlighting that Sky News Arabia reported commentary via the Iranian Deputy Foreign Minister who suggested that Iran “is prepared to abandon its nuclear program” on the condition that the US presents a rewarding alternative offer. This spurred risk-on trade, with the index falling from 99.08 to 98.75 over the course of around 15 minutes. Later Iranian press reported that Iran was prepared to get rid of its uranium stockpiles, in exchange for “something good” – though this proposal was made pre-war.

- EUR and GBP are once again pressured, as focus remains firmly on geopolitics and the inflationary/growth impacts of the net-importers. The pairs are off worst levels, following the aforementioned commentary via the Iranian Deputy Foreign Minister. There have been a few ECB speakers today, notably de Guindos suggesting that the ECB could change policy stance if inflation expectations change as a result of the war. For the GBP, ING points out the outperformance in the GBP against the EUR – the bank suggests that asset managers are unwinding previously held long EUR trades; moreover, markets have been pushing back calls for near-term cuts.

- JPY is mildly lower, with USD/JPY currently trading within a 156.44 to 157.35 range. Some modest strength in the JPY was seen on Bloomberg reports that officials see little chance of a rate hike in March, but will not rule one out in April.

- Antipodeans underperform this morning, pressured by the downside across the metals complex and in the aftermath of mixed Australian trade data – a factor which has resulted in the Aussie lagging. Moreover, China set its 2026 GDP growth target at between 4.5-5% (as expected), nonetheless, the lowest since 1991, as Beijing seeks flexibility to manage economic challenges including weak consumption, a property-sector crisis, slowing population growth and global trade tensions.

FIXED INCOME

-- A bearish start for fixed with energy dynamics once again dictating price action. USTs and Bunds lower by 11 and over 50 ticks, respectively. In brief, the ongoing Middle East conflict is bolstering yields and, in turn, weighing on benchmarks themselves. USTs down to a 112-15+ low, notching an incremental new WTD base. If the move continues, we look to recent support at 112-06, 112-04, 111-31, 111-26, 111-13+.

- For the US, and generally, today's focus is firmly on any geopolitical updates, particularly around Iran's uranium stockpiles in light of recent reporting. That aside, the day features weekly claims (does not coincide with the BLS window), Challenger jobs in addition to the Revelio and Chicago Fed statistics. Of note for PCE, the latest export/import prices will hit. The speaker docket has Fed's Bowman (voter), and while we are not guided to a text, there will be a Q&A.

- Within Europe, the story is much the same. The docket ahead is headlined by the ECB Minutes, though given recent developments, they are likely even more stale than typical. No real reaction to supply from France or Spain. As it stands, Bunds are at a 127.67 trough, approaching the WTD 127.50 base.

- Gilts experienced another morning of catch-up trade, but this time with a bearish bias given the lead from peers and movements in energy prices. No reaction to the latest DMP, the views of which are now somewhat stale. Currently holding around 20 ticks off a 91.46 low, but still lower by over 40 ticks on the day.

- EU is said to considers joint defence bonds amid concerns around the Iran war, Welt reported; a proposal is to be presented; defence bonds could be backed by member states.

- UK sells GBP 3.5bln 4.00% 2029 Gilt: b/c 3.49x (prev. 3.66x), avg. yield 3.810% (prev. 3.821%), tail 0.4bps (prev. 0.3bps).

- France sells EUR 13.449 vs exp. EUR 11.5-13.5bln 3.50% 2035, 1.25% 2036, 2.50% 2043 and 4.10% 2046 OAT.

- Spain sold EUR 5.34bln vs exp. EUR 4.5-5.5bln 2.35% 2029, 3.00% 2033 and 3.50% 2041 Bono and EUR 0.592bln vs exp. EUR 0.25-0.75bln 1.15% 2036 IL.

- Japan sold JPY 530bln 30-yr JGBs; b/c 3.66x (prev. 3.64x), and average yield 3.398% (prev. 3.615%).

COMMODITIES

- Crude benchmarks remain underpinned by the ongoing geopolitical conflict in the Middle East, despite facing mild pressure during the early European session. WTI and Brent are trading at the upper ranges of USD 74.97-78.09 and USD 81.50-84.74/bbl, respectively. The crude complex faced some pressure during the early European session. Brent saw some pressure following news that the Deputy Commander of the Iranian Army Central Command said Iran has not closed the Strait of Hormuz and is currently handling ships passing through the Strait in accordance with relevant international rules and existing agreements, CCTV reported. Further pressure was seen, following comments from the Iranian Deputy Foreign Minister that Iran is ready to abandon its nuclear program on the condition that the US presents a rewarding alternative offer, Sky News Arabia reports; adds no message was sent to the US to end the conflict.

- Spot gold initially edged higher but then stalled near the vicinity of USD 5,200/oz. Price action was relatively tame compared to recent moves, and there was little reaction to news that Venezuela's Minerven inked a multimillion-dollar deal with Trafigura to sell up to 1,000 kilos of gold destined for US markets. XAU and XAG are trading in the upper end of USD 5120.82-5158.77/oz and USD 80.523-85.545/oz, ranges respectively.

- Base metals are trading slightly lower, with 3M LME copper trading in the lower range of USD 12.87-12.96k/t. Sentiment for the red metal has been weighed down by China, its biggest market, which set its lowest GDP growth target since 1991. Elsewhere, JPMorgan said if increased headlines indicate material disruptions to Middle East supply, then aluminium prices have the potential to quickly run toward USD 4,000/mt.

- Saudi Aramco diverts more of its crude exports to the Red Sea port to bypass the Strait of Hormuz, WSJ sources reports.

- China's state iron ore buyer reportedly summons traders on BHP (BHP AT) restrictions following months of long standoff talks between CMRG and BHP over long term contracts on China's mills, Bloomberg reported.

- EU reportedly mulls aid to fix Ukraine's oil plant at centre of its loan delay, according to sources.

- Deputy Commander of the Iranian Army Central Command said Iran has not closed the Strait of Hormuz; Iran is currently handling ships passing through the Strait in accordance with relevant international rules and existing agreements, CCTV reported.

- Iranian Revolutionary Guard said it hit a US oil tanker earlier this morning, SNN reported; Tanker hit in North Persian Gulf and is now burning; US, Israeli and European vessels are not allowed in the Strait of Hormuz.

- India's MRPL has reportedly shut a crude unit and some secondary units at its 300k BPD refinery due to crude shortages.

- India is reportedly in talks with the US for ship insurance and in talks with the IEA and OPEC over the situation on crude oil supply, according to sources.

- Petronet (PLNG IS) reportedly issues force majeure.

- Kpler data shows 10mln/bbl of crude loading from Al-Muajjiz (Saudi) between March 1st and 4th, which if sustained would be a record pace, Kpler's Bakr reported. Adding, a minimum of three VLCCs in the Red Sea are signalling to Yanbu and more heading there.

- China's government urges companies to suspend signing new contracts to export refined fuel.

- Trump officials reportedly brokered a large US-Venezuela gold deal, with the Venezuela state gold miner inking a multi-million dollar deal on Monday to sell up to 1,000 kilos of gold destined for US markets to Trafigura, according to Axios sources.

NOTABLE EUROPEAN DATA RECAP

- EU Retail Sales YoY (Jan) Y/Y 2.0% vs. Exp. 1.7% (Prev. 1.8%, Rev. From 1.3%, Low. 1.4%, High. 2.1%)

- EU Retail Sales MoM (Jan) M/M -0.1% vs. Exp. 0.3% (Prev. 0.2%, Rev. From -0.5%, Low. -0.1%, High. 0.6%)

- UK S&P Global Construction PMI (Feb) 44.5 vs. Exp. 47 (Prev. 46.4).

- Italian Retail Sales YoY (Jan) Y/Y 2.3% (Prev. 0.9%).

- Italian Retail Sales MoM (Jan) M/M -0.8% vs. Exp. 0.2% (Prev. -0.8%).

- French Industrial Production MoM (Jan) M/M 0.5% vs. Exp. 0.5% (Prev. 0.5%, Rev. From -0.7%, Low. 0.2%, High. 1.0%).

- Spanish Industrial Production YoY (Jan) Y/Y 0.3% vs. Exp. 1.7% (Prev. -0.3%).

- Swedish CPIF MoM Prel (Feb) M/M 0.6% vs. Exp. 0.8% (Prev. 0.3%).

- Swedish CPIF YoY Prel (Feb) Y/Y 1.7% vs. Exp. 1.8% (Prev. 2.0%).

- Swedish Inflation Rate MoM Prel (Feb) M/M 0.6% vs. Exp. 0.8% (Prev. 0.1%).

- Swedish Inflation Rate YoY Prel (Feb) Y/Y 0.5% vs. Exp. 0.6% (Prev. 0.5%).

- Swiss Unemployment Rate (Feb) 3.2% (Prev. 3.2%, Low. 2.9%, High. 3.0%).

CENTRAL BANKS

- Bank of Japan officials see little chance of a rate hike this month but still on track to raise interest rates, with the possibility of April not ruled out, according to sources cited by Bloomberg.

- ECB's Nagel says it is too soon to draw any monetary policy conclusion from the volatile Iran situation.

- ECB's Rehn said it is likely to raise inflation in the short-term; this kind of conflict tends to dampen demand and leads to more subdued growth.

- ECB's de Guindos said outlook for Europe is shaped by war in Iran, balance of risks was two-sided before the war. Baseline scenario is that it will be a short conflict, with other scenario being that of a more protracted one. ECB could change policy stance if inflation expectations change as a result of the war. Will look out for any steady modification of inflation and inflation expectations.

- ECB's Villeroy does not see a reason today why the ECB should raise interest rates.

- ECB's Villeroy said the ECB are following energy prices and markets very closely; financial stability is not at risk.

- BoE DMP (Feb): 1yr ahead CPI expectation 3.00% (prev. 3.10%), 3yr ahead CPI expectation 2.8% (prev. 2.9%).

- BoE is to scenario plan the potential economic and financial impact of an AI shock amid concerns of jobs cuts, according to Bloomberg.

- CNB's Prochazka tells Ekonom that he sees potential for 25bps rate cut to 3.25%, said the CNB may cut rates once more this year. NOTE: The interview was conducted prior to the Middle East conflict this week.

- Morgan Stanley expects the ECB to keep interest rates steady in 2026 vs the prior forecast of two 25 bps cuts each in June and September; Morgan Stanley expects the ECB to resume rate cuts in 2027 with two 25 bp cuts each in June and September.

NOTABLE US HEADLINES

- US Treasury Secretary Bessent reportedly informed House Republicans that they should “take the lead” to “pass our own housing affordability” legislation, in order to prevent Democrats from controlling the issue, Semafor reports citing sources

- Judge orders Trump admin to finalise goods entering US without assessing tariffs that were struck down by the SCOTUS; order could impact millions of shipments.

- US Senate Republicans await the endorsement of President Trump in the Texas Republican Senate runoff between Cornyn and Paxton, Politico reported; billed as a choice between an established Republican candidate, and a MAGA firebrand.

- BofA card spending, week to Feb 28th: +1.8% (prev. 4.4% W/W), slowdown driven by the Northeast is which spending fell sharply due to the second snowstorm.

GEOPOLITICS

MIDDLE EAST

- Iran was prepared to get rid of uranium stockpiles in US talks for something good in exchange, according to Iranian press.

- Iran's Deputy Foreign Minister said Iran is ready to abandon its nuclear program on the condition that the US presents a rewarding alternative offer, Sky News Arabia reported; adds no message was sent to the US to end the conflict. Focused on self defence efforts.

- Iran's ambassador to India said Tehran is not ready for negotiations with the US and Israel, while Iran does not want war but has the capability to respond.

- Deputy Commander of the Iranian Army Central Command said Iran has not closed the Strait of Hormuz; Iran is currently handling ships passing through the Strait in accordance with relevant international rules and existing agreements, CCTV reported.

- Iranians have been sending messages to the Trump admin in recent days through Gulf states and other countries in the region, Axios reported, citing US sources; but the US has not responded, "We treated those messages as bullshit".

- Iranian military denies firing any missiles at Turkey and affirms respect for its sovereignty.

- Iranian media report that Iran has bombed Kurdish headquarters in Sulaymaniyah, Iraq, according to Al Arabiya.

- Iranian semi official SNN reported Iran missiles hit Tel Aviv and that Israeli air defences failed.

- US officials have discussed sending special operations teams into Iran to target senior Iranian Revolutionary Guard Corps (IRGC) officials and people familiar with Iran's nuclear programme, Middle East Eye reported overnight citing a Gulf official.

- Israel announced it is conducting a fresh widespread wave of strikes in Tehran; subsequently, blasts reported in Tehran and Karaj.

- Sirens sound in Tel Aviv after an Iranian missile attack, while Sky News Arabia reported rockets were intercepted in the sky of Tel Aviv.

- Explosions heard in Jerusalem following warning about rocket fire from Iran, while Lebanese media reported two Israeli raids on the town of Tol in southern Lebanon.

- Israel Home Front gives all clear for central region, while sirens sound in Kiryat Shmona, according to N12.

- IDF said rockets were fired from Iran towards Israel and defense systems are intercepting the threat.

- Israel conducts a second raid on the southern suburbs of Beirut, according to Sky News Arabia.

- Sirens sound in Upper Galilee, Northern Israel, amid fears of drone infiltration, according to Sky News Arabia.

- Iraqi Kurdish sources deny involvement in the Iran war and said the Kurdistan region won't be a part of the war with Iran, according to ISNA.

- Iran's strikes will intensify and expand in the coming days, according to Nour News, citing a statement by the IRGC.

- US bases in Doha, Qatar, have been attacked, Iranian media reported.

- Explosions heard in Doha, Qatar, Sky News Arabia reported citing AFP.

- US Central Command has asked the Pentagon to send intelligence officers to its headquarters in Florida to support the war for at least 100 days.

- US Senate blocks efforts to force Trump to end Iran's strikes without Congress approval; final vote count at 53-47.

RUSSIA-UKRAINE

- Russia's Kremlin said there's no sign that Europe has changed its position on the Nord Stream, but that the EU is thinking of delaying imposing ban on LNG imports from Russia.

- Russian Foreign Minister Lavrov said they are ready for further Ukraine talks, but have not yet seen the Western security guarantees and as such cannot approve them.

- Russian Ambassador Alipov said they are always open to oil supplies to India.

CRYPTO

- Bitcoin oscillates around USD 72,500 while Ethereum holds above USD 2,100.

APAC TRADE

- APAC stocks rebounded from yesterday's sell-off as the region took impetus from the positive handover from Wall Street, where the Nasdaq led the advances on tech strength, while geopolitics remained in focus.

- ASX 200 was led higher by tech strength, but with gains capped by losses in the commodity-related sectors and after mixed trade data, which showed a contraction in monthly exports.

- Nikkei 225 surged at the open but is off today's best levels after giving back the 56,000 status and with some headwinds from a stronger currency and firmer yields.

- KOSPI firmly rebounded from the prior day's drastic sell-off and surged by over 11% in the first few minutes of trade.

- Hang Seng and Shanghai Comp followed suit to the gains in regional peers, but with gains initially contained in the mainland as the attention was on the Government Work Report, in which China set the 2026 GDP target at between 4.5%-5.0%, its slowest growth target on record since 1991.

NOTABLE ASIA-PAC HEADLINES

- China targets 2026 GDP growth at 4.5%-5.0%, as expected, while it sees 2026 CPI at around 2%. To add, China is to issue CNY 800bln yuan of new policy financing tools.

- Chinese Premier Li Qiang said solid progress in modernisation and successful conclusion of the 14th Five-Year Plan, while China aims to boost consumption in its 15th Five-Year Plan.

- South Korea President Lee said need to counter volatility increase in financial markets and need to pay attention to energy prices and supply, reiterates KRW 100tln program is on standby to stabilise markets.

NOTABLE APAC DATA RECAP

- Australian Balance of Trade (Jan) 2.631B vs. Exp. 3.9B (Prev. 3.373B).

- Australian Imports MoM (Jan) M/M 0.8% (Prev. -0.8%).

- Australian Exports MoM (Jan) M/M -0.9% (Prev. 1%).

- Japanese Stock Investment by Foreigners (Feb/28) 973.9 (Prev. 399.7, Rev. From 402).

- Japanese Foreign Bond Investment (Feb/28) -673.1 (Prev. -1900.8, Rev. From -1898.8).