Equities mixed despite positive Nvidia earnings; Third round of US-Iran talks awaits - Newsquawk EU Market Open

- APAC stocks are mostly positive as the majority of the region took its cue from gains on Wall Street, where tech led the advances, and NVIDIA posted stronger-than-expected earnings.

- US equity futures initially saw support following NVIDIA's earnings results, as the world's most valuable company beat on top and bottom lines, although gains were pared as NVIDIA ultimately returned to flat territory after hours.

- BoJ's Governor Ueda said there is no change from January to the BoJ’s projected timing for hitting its price target, and inflation is expected to re-accelerate from the current slowdown.

- US VP Vance said they see evidence that Iran is trying to build a nuclear weapon; US Secretary of State Rubio said Iran poses a grave threat and seeks nuclear capability.

- European equity futures indicate a slightly lower cash market open with Euro Stoxx 50 futures down 0.2% after the cash market closed with gains of 0.9% on Wednesday.

- Looking ahead, highlights include EZ Consumer Confidence Final (Feb), US Jobless Claims, Japanese Tokyo CPI (Feb), Retail Sales (Jan). Speakers include ECB's Lagarde, BoE's Lombardelli & Fed's Bowman. Supply from Italy & US. Earnings from CoreWeave, Intuit, Vistra Energy, Autodesk, Dell, Baidu, Warner Bros Discovery, Munich Re, Schneider Electric, AXA, Engie & Saint-Gobain.

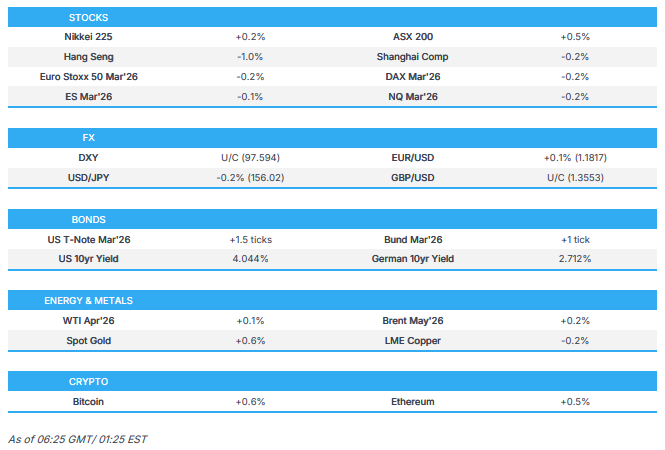

SNAPSHOT

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks continued to advance as tailwinds from the recent easing of AI disruption fears persisted. As such, the Nasdaq outperformed its major peers with tech and financials leading the gains, as tech was buoyed by gains in software, while NVIDIA (NVDA) shares were also supported heading into earnings after-hours, which proved to be better-than-expected and added a further lift to futures.

- SPX +0.81% at 6,946, NDX +1.41% at 25,329, DJI +0.63% at 49,482, RUT +0.41% at 2,663.

- Click here for a detailed summary.

TARIFFS/TRADE

- NVIDIA (NVDA) confirmed it was granted a US licence in February to ship a small amount of H200 chips to China-based customers, and it stated that H200 chips face 25% tariffs.

- China's DeepSeek withholds its upcoming model from NVIDIA (NVDA) and AMD (AMD), while it granted early access to Huawei and others in China.

- UK Foreign Secretary Cooper is to announce a critical minerals deal with Kazakhstan today and will announce agreements with the other countries covering carbon capture and higher education, as the West seeks to diversify supply chains away from China, according to POLITICO.

NOTABLE HEADLINES

- Fed's Musalem (2028 voter) said inflation is almost a full percentage point above target and the labour market is cooling in an orderly way. Musalem said the base case outlook is that the economy grows at or above 2%, while he added that financial conditions are accommodative and that there is deregulation and fiscal tailwinds. He also stated that inflation could stay higher for longer, although this is not his baseline, and policy is neutral now in real terms and is balancing appropriately.

- Fed Vice Chair for Supervision Bowman did not address monetary policy or the economic outlook in prepared testimony.

- White House official said Amazon (AMZN), Google (GOOGL), and Oracle (ORCL) are to sign data centre agreements.

- US government is to meet with robot-makers as China competition intensifies, according to Semafor.

- NVIDIA Corporation (NVDA) Q4 2026 (USD): Adj. EPS 1.62 (exp. 1.54), Revenue 68.1bln (exp. 66.12bln)

APAC TRADE

EQUITIES

- APAC stocks are mostly positive as the majority of the region took its cue from gains on Wall Street, where tech led the advances and NVIDIA posted stronger-than-expected earnings after hours.

- ASX 200 mildly gained as the outperformance in tech, telecoms and healthcare offset the losses in energy and industrials, while better-than-expected private capex data also provided some encouragement.

- Nikkei 225 initially rallied to a fresh all-time high north of the 59,000 level but then pulled back from record levels as the yen gradually strengthened and after BoJ hawkish dissenter Takata called for gradually hiking rates.

- Hang Seng and Shanghai Comp were ultimately mixed with the Hong Kong benchmark the laggard amid weakness in tech, consumer discretionary and insurers, while the mainland was indecisive as price action was contained with very little in the way of fresh catalysts.

- US equity futures initially saw support following NVIDIA's earnings results as the world's most valuable company and AI darling beat on top and bottom lines, although gains were pared as NVIDIA ultimately returned to flat territory after hours.

- European equity futures indicate a slightly lower cash market open with Euro Stoxx 50 futures down 0.2% after the cash market closed with gains of 0.9% on Wednesday.

FX

- DXY slightly softened in rangebound trade with demand constrained after weakening alongside the heightened risk appetite during US trade and amid a light data calendar. There was also very little impact seen following the latest Fed comments, including from Musalem who stated that inflation could stay higher for longer, although this is not his baseline, while he noted that policy is neutral now in real terms and is balancing appropriately.

- EUR/USD was slightly firmer after returning to 1.1800 territory owing to a softer buck, but with further gains limited by a lack of catalysts from the bloc.

- GBP/USD took a breather after advancing in tandem with cyclical peers and following comments from BoE's Greene, who said there is a strong case for the Bank to do exactly the opposite of what the Fed is doing, and it does not make sense to set domestic policy based on another central bank.

- USD/JPY continued to pull back after climbing to its best levels in over two weeks yesterday following the Takaichi government's reflationist picks for the BoJ board, with the pair not helped by the lack of fresh drivers and absence of tier-1 data from Japan, while there were comments from BoJ Governor Ueda who reiterated the hiking bias, and hawkish dissenter Takata also stated that they must conduct further rate hikes in a gradual manner.

- Antipodeans kept afloat overnight following the recent outperformance that was facilitated by their high-beta statuses and hot Aussie CPI data, while quarterly capex data from Australia also topped forecasts, which feeds into next week's GDP release.

- PBoC set USD/CNY mid-point at 6.9228 vs exp. 6.8605 (Prev. 6.9321).

FIXED INCOME

- 10yr UST futures eked slight gains, albeit with price action contained ahead of US supply, including a 7yr auction.

- Bund futures struggled for direction amid recent indecision with very few fresh catalysts from the bloc.

- 10yr JGB futures languished near this week's trough after yesterday's selling pressure and curve steepening on stronger growth prospects after the Takaichi government nominated two staunch reflationists for the BoJ board. There were also recent comments from BoJ officials who reiterated that the basic stance is to continue hiking interest rates if the chances of reaching the BoJ's targets increase, while hawkish dissenter Takata stated that the BoJ should make a further “gear shift” on rates and communicate on the assumption its price target is almost achieved.

COMMODITIES

- Crude futures were rangebound following the recent choppy performance and substantial build in crude stockpiles, while the attention remains on geopolitics with the US and Iran set to resume talks in Geneva today.

- Spot gold kept afloat and retested the USD 5,200/oz level, but with price action relatively contained in comparison to the early swings in silver.

- Copper futures held on to most of the prior day's spoils but with upside capped overnight as Chinese markets lagged behind regional peers.

CRYPTO

- Bitcoin ultimately climbed higher in choppy trade and gained a firm footing above the USD 68,000 level.

NOTABLE ASIA-PAC HEADLINES

- BoJ's Governor Ueda said the basic stance is to continue hiking interest rates if the likelihood of economic and price forecasts materialising heightens, while he added that underlying inflation has not yet fully reached 2% and policy will be guided to get underlying inflation to around 2%, while avoiding it exceeding 2% on a sustained basis. Ueda also stated that there is no change from January to the BoJ’s projected timing for hitting its price target, and inflation is expected to re-accelerate from the current slowdown, according to Yomiuri.

- BoJ Board Member Takata (hawkish dissenter) said fears of Japan's economy returning to deflation have been dispelled and he believes it's necessary to move the BoJ's focus more to the upswing in prices. Takata noted that real short-term interest rates have been significantly negative in Japan even after the December rate hike, and that he proposed a rate hike in January on the view that the BoJ must continue adjusting real interest rates, which remain significantly lower than the rates seen overseas. He also commented that they must conduct further rate hikes in a gradual manner and should take time and be prudent in reducing its JGB purchases, as well as commented that the BoJ should make a further “gear shift” on rates and communicate on the assumption that its price target is almost achieved.

- Bank of Korea kept its base rate unchanged at 2.50%, as expected, with the decision made unanimously, while it stated it will make policy decisions supporting a recovery in economic growth and that growth momentum is to remain favourable, with strong chip exports supporting growth. BoK also commented that housing prices around Seoul have slowed, and it is necessary to remain cautious about risks related to housing prices, household debt and FX volatility. In terms of forecasts, it raised the 2026 GDP growth forecast to 2.0% from 1.8% and sees 2027 growth at 1.8%, as well as raised the 2026 CPI forecast to 2.2% from 2.1% and sees 2027 CPI at 2%. Projections also showed that 16 of 21 policy rate forecasts by board members saw the policy rate at 2.50% over the next six months, 1 projection saw the policy rate at 2.75%, and 4 forecasts saw the policy rate at 2.25% during that period. Furthermore, BoK Governor Rhee said the conditional rate projection for a 25bps cut by a board member assumed the local property market is to stabilise in six months time and that no board member expects rates to be increased in three months time.

DATA RECAP

- Australian Private Capital Expenditure QQ (Q4) 0.4% vs. Exp. 0.0% (Prev. 6.4%)

- Australian Private Capital Expenditure for 2026-27 (AUD)(Estimate 1) 158.4B

- Australian Private Capital Expenditure for 2025-26 (AUD)(Estimate 5) 199.3B (Prev. 191.3B)

GEOPOLITICS

MIDDLE EAST

- US VP Vance said they see evidence that Iran is trying to build a nuclear weapon.

- US Secretary of State Rubio said Iran poses a grave threat and seeks nuclear capability, while he added that Iran poses a conventional weapons threat designed to target the US. Furthermore, he said that talks on Thursday will focus on the nuclear programme, and he does not think diplomacy is ever off the table.

- US Envoy Witkoff said any Iran nuclear deal should last indefinitely, according to Axios.

- White House officials argued it would be best if Israel made the first move on striking Iran, according to POLITICO

- Iranian Foreign Minister Araghchi said if the US decides to attack Iran, US bases in the region will be legitimate targets as they consider them US bases, not the soil of their neighbours or the territory of any other country.

- Israeli diplomatic sources estimate that the new Iranian outline does not meet the American threshold conditions and one source estimated that there is a high chance that the US will launch an attack on Iran, according to Ynet.

RUSSIA-UKRAINE

- Ukrainian President Zelensky said he spoke with US President Trump, and Special Envoys Witkoff and Kushner, while they discussed issues representatives will address on Thursday in Geneva during the bilateral meeting, as well as preparations for the next trilateral meeting.

OTHER NEWS

- US Secretary of State Rubio said the US will investigate a deadly speedboat shooting off Cuba after the Cuban Interior Ministry reported its forces killed four people who allegedly opened fire from a Florida-tagged vessel.

- China's consulate warned Chinese citizens to avoid travel to Japan.

EU/UK

NOTABLE HEADLINES

- UK government debt sales are anticipated to decline for the first time in four years, as large banks forecast GBP 247bln of gilt issuances in the approaching fiscal year as Chancellor Reeves seeks to rein in borrowing, according to FT.

Loading...