Full Analysis Of The Supreme Court IEEPA Decision: How It Impacts The Economy, Policy And Markets

On Friday, the Supreme Court struck down the tariffs imposed under the International Emergency Economic Powers Act (IEEPA), including the “reciprocal” tariffs as well as tariffs applied to Canada, China, Mexico, and other countries under separate emergency declarations.

President Trump announced a 10% “global tariff” under Sec. 122 shortly after the ruling and raised that to 15% on Saturday, with details of the change not yet clear. This surcharge would remain in place until late July, followed by longer-lasting and potentially higher tariffs under Sec. 301.

What are the implications?

Below we excerpt from two just published reports (one from Goldman, one from Morgan Stanley, both available to pro subscribers), which discuss the consequences for the economy, markets, public policy and more. Here are the main highlights:

Goldman estimates that the combination of the Supreme Court ruling and the newly announced Sec. 122 tariff will modestly reduce the increase in the effective tariff rate since the start of 2025 from just over 10% to 9%. The policy changes were in line with expectations, and the bank's estimates of the effects of tariffs on inflation and growth are consequently little changed.

- Goldman's estimates of passthrough from tariff costs to consumer prices suggest that the bulk of the passthrough had already occurred before the Supreme Court ruling. Specifically, the bank believes that tariff passthrough increased core PCE prices by about 0.7% through January (extrapolating from CPI data for January) and will raise prices by a further 0.1% in the remainder of 2026.

- Refund picture still murky: The Court did not dictate whether the Trump administration has to repay the tariffs or do so over any specific timeframe. In his dissent, Justice Kavanaugh reiterated that the refund process "is likely to be a mess." That said, tariff collection likely stops immediately; given that the Supreme Court struck down the IEEPA tariff authority broadly, continued collections would lack legal basis. This will likely result in prolonged uncertainty as the question of refunds will be left to the deliberations of the lower courts. In the past, refunds were initially limited only to companies that proactively filed complaints or litigation through a process established by CBP or the Treasury, which may ultimately limit the scope of refunds. That said, since various politicized outlets have calculated that US consumers were impacted by 90% of the tariffs, this in effect allows Trump to pursue a mid-term stimulus payment to the US middle class, allowing him to direct deposit as much as $120BN (90% of the $133 in IEEPA tariff refunds) at some point ahead of the midterms. Call it the 2026 Trump Tariff Refund Stimulus.

- Other paths are available, but potential sector-specific tailwinds are under the surface: Trump has said he has a backup plan, and members of the administration have suggested that he will leverage other authorities to reimpose the tariffs. While many expected the SCOTUS announcement to be met with this response from the administration, the President will likely pursue a lighter-touch tariff policy under the surface. That means more exceptions, carve-outs, delays, etc., in line with recent steps taken by the administration in the past few months. That could provide a tailwind for countries and products that could eventually fall out of scope of new Sec. 232 or 301 investigations.

- In terms of the US economy, the decision does not come as a surprise and, given the administration's subsequent announcement that it will seek to recreate its trade policy under different – and likely more durable – legal authority, Morgan Stanley expects it to have little effect on economic activity. Under the assumptions that 1) the current tariff structure will move to different legal authority and largely remain in place and 2) refunds will be limited in size ($85bn assumed as the midpoint of the estimated range of outcomes), business intentions for spending or hiring will change much. In other words, if importers receive a rebate only to have to repay that rebate in the form of additional future tariffs on imports, then it is close to a status quo outcome. One factor that could change Morgan Stanley's base case view is whether the administration will use temporary legal authority to keep tariffs in place while it initiates new investigations under Sections 232 and 301. Other courses of action remain open: one way to address the affordability issue could be to let the effective tariff rate fall while new Section 232 and 301 investigations are completed, which would most likely occur later this year or in 2027. If this resulted in temporary downward pressure on inflation and delayed the paying of new import tariffs by the corporate sector into 2027, then it would lead to a more constructive view for growth in economic activity.

- Imports from countries that will experience meaningful tariff reductions from the latest policy changes are likely to pick up in coming months, but the impact on GDP should be largely offset by increased inventory accumulation and consumption, reduced imports from other countries through which trade had been rerouted, and small reductions in imports from countries whose tariff rate has risen. As an aside, Goldman is launching its Q1 2026 GDP tracking estimate at 3.4%, though this incorporates a 1.3% contribution from the end of the government shutdown in 2025 Q4 (as we calculated on Friday). Goldman also forecasts 2.5% GDP growth for 2026 Q4/Q4, a 0.3% acceleration from 2025 Q4/Q4 that partly reflects the fading drag from tariffs giving way to a boost from tax cuts

- Market Implications: Treasuries, US Treasury market implications: Provided the administration will leverage other existing authorities to reimpose tariffs, Morgan Stanley does not think investor expectations about the near-term path of the fiscal deficit will change. As it relates to refunds, the Supreme Court decision “said nothing today about whether, and if so how, the Government should go about returning the billions of dollars that it has collected from importers.” (per Justice Kavanaugh's dissenting opinion). Until investors come to understand the contours of the Supreme Court decision, as it relates to refunds, they may view the risk as skewing to higher, not lower, Treasury yields. Indeed, the first order market reaction is as expected, as investors sold Treasuries on the perception this will force Treasury to increase coupon sizes sooner.

- Market Implications: USD MS economists expect that 1) the current tariff structure will move to different legal authority and largely remain in place, and 2) refunds will be limited in size (assume $85bn as the midpoint of our estimated range of outcomes). Reduced latitude from the US administration to use immediate tariff authority as a tool of foreign policy may at the margin diminish the USD-negative risk premium associated with investor caution around maintaining US currency exposure. However, offsetting factors are likely to maintain (or even widen) this USD-negative risk premium, including geopolitical uncertainty and questions around US currency policy. Additionally, the mechanical positive effect on global growth (as tariffs using different authorities take time to be implemented, and may be implemented at lower levels) will likely boost global growth expectations, further weighing on the USD.

* * *

Next, we take a more detailed look at how Wall Street is reacting to the latest tariff news, starting with a comprehensive report from Goldman's chief political economist Alec Phillips (available here to pro subscribers), which looks almost entirely at the SCOTUS decision impact on...

US Economics

On Feb. 20, the Supreme Court ruled against the tariffs the Trump Administration imposed under the International Emergency Economic Powers Act (IEEPA), in a 6-3 decision. This includes the “reciprocal” tariffs applied on trading partners at various rates as well as tariffs applied to Canada, China, Mexico and other countries under separate emergency declarations, but it does not affect tariffs imposed under other laws (e.g., the metals and auto tariffs imposed under Sec. 232, or the 2018-2019 China-focused tariffs under Sec. 301). The court’s decision is silent on the question of refunds, which is likely to lead importers to seek repayment in a separate process in lower courts. To date, Goldman estimates IEEPA tariffs have collected around $180bn and that most of this will be refunded in increments over the next year or so.

As expected, President Trump responded by announcing a new “global tariff” under Sec. 122 of the Trade Act of 1974 to replace the prior reciprocal tariff regime. An executive order signed Feb. 20 imposed a 10% surcharge on imports from all countries, with essentially the same exemptions as the prior reciprocal tariffs (energy, precious metals, a number of other products subject to current or prospective Sec. 232 sectoral tariffs and USMCA-compliant imports from Canada and Mexico). Soon after, President Trump announced that he was raising the 10% surcharge to 15%, but as of this writing the White House has not released additional detail or a new executive order.

Tariffs under Sec. 122 are limited under law to 15%, which creates some near-term certainty as tariff rates cannot rise further without taking more administratively involved steps under other laws like Sec. 301. However, using Sec. 122 creates new uncertainty in two ways.

- First, it is not yet clear how trading partners with reciprocal tariffs under 15% would be treated, but it is safe to assume that this will mean an increase in the tariff rate, at least in the short run. Australia, Singapore, the UK, GCC countries, and many smaller economies faced a 10% reciprocal tariff rate prior to the court ruling, and this will rise to 15% if applied as an across-the-board surcharge, as seems likely. A few larger economies, notably the EU, Japan, Switzerland, and Taiwan, agreed to deals with the Trump administration that imposed a maximum 15% rate inclusive of the existing US tariff, which generally ranged between 0 and 2.5%. These trading partners look likely to face an incremental tariff increase assuming the 15% now “stacks” on top of the existing US tariff rate.

- Second, Sec. 122 limits these tariffs to 150 days “unless such period is extended by an act of Congress.” The Feb. 20 executive order specifies that the current rate expires July 24, and comments from President Trump and other administration officials suggest they intend to use other laws to impose new tariffs after that. In theory, the White House could briefly end the Sec. 122 tariffs after 150 days and restart them, though this seems likely to invite legal challenges.

The fact that the Sec. 122 tariffs are set at a higher rate than prior tariffs for some trading partners but a lower rate for others is likely to create new friction with trading partners and additional volatility in trade flows, with imports likely to rise from countries that temporarily face lower tariffs while volumes might fall from countries with temporarily higher tariffs. This raises the odds that the administration might seek to modify this new tariff regime through other authorities, like Sec. 301.

President Trump’s comments suggested that the US Trade Representative (USTR) will finalize Sec. 301 investigations into some trading partners during the 150-day period, but it is unclear how the White House will prioritize these investigations. The US already has Sec. 301 tariffs in place on imports from China and could easily adjust these to restore the tariffs struck down by the court, but this seems unlikely ahead of Trump’s visit to China in late March. For Canada and Mexico, we expect the administration to pursue the USMCA review process rather than imposing Sec. 301 tariffs on either US neighbor. These three countries accounted for 36% of US imports in 2025.

Several other trading partners accounting for just over half of imports in 2025 have agreements with the US and are also unlikely to be prioritized for Sec. 301 investigations (this includes Argentina, Australia, Bangladesh, Cambodia, Ecuador, El Salvador, the EU, Guatemala, India, Indonesia, Japan, Korea, Malaysia, Switzerland, Taiwan, Thailand, the UK, and Vietnam).

Goldman expects this to leave countries representing around 10% of US imports at greatest risk for near-term Sec. 301 investigations, including Brazil and South Africa. However, without any other obvious tariff authority to fall back on after July 24, the administration will likely rely on Sec. 301 to impose tariffs on most other trading partners after that point. For some trading partners, this could mean a rise in tariff rates back to what was imposed under IEEPA, while for others it could mean a reduction below 15%. It's also worth noting that Sec. 301 investigations related to a particular trade-related policy or sector could cover several countries at once.

Overall, Goldman expects that a rate similar to the 15% just announced will last through the end of the year with the same exemptions as the IEEPA tariffs, but that at the start of 2027, the administration will use Sec. 301 and other authorities to restore tariff rates to a level similar to what was in place prior to the Supreme Court ruling. The risks to these assumptions lie in either direction at different points, with risks leaning toward lower tariffs after July, as the administration might struggle to fully replace the expiring Sec. 122 tariffs using other authorities. But after the midterm election and by the start of 2027 the risks lean toward higher tariffs.

While President Trump didn’t raise this possibility explicitly, it is also possible that the administration could expand its use of Sec. 232 to impose tariffs on specific product categories. While the White House threatened such tariffs on several sectors (e.g., pharmaceuticals, semiconductors, etc.) over the last year, Goldman has removed tariffs from pending Sec 232 investigations from its baseline assumptions several months ago and does not expect any further sectoral tariffs this year.

The chart below (Exhibit 1) shows that we estimate that the changes will reduce the increase in the effective tariff rate since the start of 2025 from just over 10% to about 9% once the Sec. 122 tariffs are implemented. This is roughly in line with what we had expected prior to the ruling. The risks are tilted toward the increase in the effective tariff rate drifting a bit higher back toward 10pp over time, for example if the White House moves to limit exemptions or imposes larger tariffs using Sec. 301. But we assume that this risk is limited ahead of the midterm election.

The next chart provides Goldman's detailed estimates of how tariff rates for each country will change after the latest policy changes.

Because the change in the effective tariff rate looks likely to be quite close to Goldman's previous assumption, the bank's estimates of the effects of tariffs on inflation and GDP growth have not changed meaningfully. Separately, the December PCE price data were also released on Friday. Exhibit 2 shows that Goldman now estimates that tariff passthrough to consumer prices reached just over 60% after 10 months on the goods that have faced tariffs for that long. It also shows that incremental tariff passthrough beyond the first five months has been modest, suggesting that the bulk of the passthrough had already occurred before the Supreme Court ruling. The bank assumes that the passthrough rate will peak at 70%, though for some goods this is now 70% of a slightly lower tariff cost after the latest policy changes.

Based on its tariff and passthrough assumptions, Goldman estimates that further impact on consumer prices will be minor from here. The left side of Exhibit 3 shows that GS estimates that tariff passthrough increased core PCE prices by about 0.7% through January (extrapolating from CPI data for January), similar to or a touch smaller than other estimates, and will raise prices by a further 0.1% in the remainder of 2026. The right side of Exhibit 3, however, shows that a large gap will persist in year-over-year terms through the middle of this year between the official inflation rate and estimates of the rate excluding tariff effects.

The reason Goldman does not expect a net disinflationary impact in the remainder of 2026 despite the small decline in the effective tariff rate is that companies will not lower prices in response to tariff reductions nearly as quickly as they increased them in response to tariff increases. By the same token, future price increases on most goods facing tariff reductions will be smaller than usual — otherwise profit margins would remain permanently wider — but this has only a very small impact on Goldman's near-term inflation forecast.

On the activity side, the latest changes will most directly affect US imports. Tariff rates on some countries, notably China, will decline meaningfully following the Supreme Court ruling. As a result, imports from these countries in Q1 and Q2 are likely to rebound somewhat from depressed levels, though the impact on GDP should be largely offset by increases in inventory accumulation and consumption, reduced imports from other countries through which trade had been rerouted, and small declines in imports from countries that will experience tariff increases.

Taking that on board as well as the 2025 Q4 GDP report and the December consumer spending data also released on Friday, Goldman has launching its 2026 Q1 GDP tracking estimate at 3.4%. The forecast includes a 1.3% contribution from the end of the lengthy government shutdown in 2025Q4, meaning that the underlying growth pace net of that special factor is a more moderate 2.1%. Goldman is penciling in a 2.0% pace of consumption growth and a moderate drag from net trade roughly offset by a pick-up in inventory accumulation, which remained negative in 2025 Q4 but seems likely to turn positive because most companies have likely exhausted stockpiles built up from frontloading ahead of tariffs.

As a result, Goldman's GDP growth forecast for 2026 Q4/Q4 remains 2.5%, with risks tilted a bit to the upside. This would represent a 0.3% acceleration from 2.2% growth in 2025 on a Q4/Q4 basis, in part reflecting the positive swing in the policy impulse shown in Exhibit 5 as the tariff drag gives way to a tax cut boost. While the remaining tariff drag in 2026 shown in the exhibit is now a bit smaller, Goldman's latest immigration assumptions imply a slightly larger drag on growth, and the two changes are roughly offsetting.

Turning to Morgan Stanley, the bank agrees with Goldman that in terms of its outlook for the US economy, the decision does not come as a surprise and, given the administration's subsequent announcement that it will seek to recreate its trade policy under different – and likely more durable – legal authority, it is expected to have little effect on economic activity.

Under the assumptions that 1) the current tariff structure will move to different legal authority and largely remain in place and 2) refunds will be limited in size (MS assumes $85bn as the midpoint of its estimated range of outcomes), then Morgan Stanley does not think business intentions for spending or hiring will change much. In other words, if importers will receive a rebate only to have to repay that rebate in the form of additional future tariffs on imports, then it is close to a status quo outcome.

What could change our view? The main factor that could change the baseline view is whether the administration uses temporary legal authority to keep tariffs in place while it initiates new investigations under Sections 232 and 301. It is most likely that it will, but other courses of action can not be ruled out. For example, one way to address the affordability issue could be to let the effective tariff rate fall while new Section 232 and 301 investigations are completed, which would most likely occur later this year or in 2027. If this resulted in temporary downward pressure on inflation and delayed the paying of new import tariffs by the corporate sector into 2027, then MS would have a more constructive view for growth in economic activity.

2. US Public Policy

Refund picture still murky: The Court did not dictate whether the Trump administration has to repay the tariffs or do so over any specific timeframe. In his dissent, Justice Kavanaugh reiterated that the refund process "is likely to be a mess." That said, tariff collection likely stops immediately; given that the Supreme Court struck down the IEEPA tariff authority broadly, continued collections would lack legal basis. This will likely result in prolonged uncertainty as the question of refunds will be left to the deliberations of the lower courts. In the past, refunds were initially limited only to companies that proactively filed complaints or litigation through a process established by CBP or the Treasury, which may ultimately limit the scope of refunds.

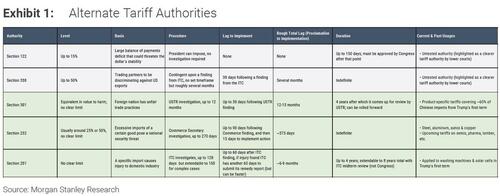

Other paths are available, but potential sector-specific tailwinds are under the surface: President Trump has said he has a backup plan, and members of the administration have suggested that he will leverage other authorities to reimpose the tariffs.And while Trump promptly announced a hike in Section 122 tariffs to first 10% and then 15%, Morgan Stanley still expects the President to pursue a lighter-touch tariff policy under the surface. That means more exceptions, carve-outs, delays, etc., in line with recent steps taken by the administration in the past few months. That could provide a

tailwind for countries and products that could eventually fall out of scope of new Sec. 232 or 301 investigations (i.e., low-tech goods from countries that are difficult to accuse of trade misconduct). See the exhibit below for more details.

A trade-off between more uncertainty in the near term and a lighter tariff regime in the medium to long term: Morgan Stanley sees an opportunity for the President to alleviate some components of the existing tariff regime over time, but in the nearer term, uncertainty will likely prevail in terms of which authorities will replace the existing tariffs, which sectors/countries will face more legally durable tariffs (Sec. 232/301 after months of investigation), and most importantly, what happens to the bilateral framework deals that are currently in place. That means the broader macro impact could be modest in the context of these two competing factors.

3. Market Implications

US Treasury market implications: Provided that the administration will leverage other existing authorities to reimpose tariffs, it is unlikely that investor expectations about the near-term path of the fiscal deficit will change. As it relates to refunds, the Supreme Court decision “said nothing today about whether, and if so how, the Government should go about returning the billions of dollars that it has collected from importers.” (per Justice Kavanaugh's dissenting opinion). Until investors come to understand the contours of the Supreme Court decision, as it relates to refunds, they may view the risk as skewing to higher, not lower, Treasury yields. The first order market reaction is as expected, as investors sold Treasuries on the perception this will force Treasury to increase coupon sizes sooner.

- Morgan Stanley does not expect this reaction to be long-lived, as most investors eventually come to understand that the potential issuance increase necessitated from this ruling will be comprised of short-dated T-bills. Another important consideration for investors is that although Treasury may face an additional obligation, it need not wait until the time for refunds to begin the process of building up the Treasury General Account (TGA). Therefore, Morgan Stanley thinks the second order and more lasting reaction is investors “buy the fact” and send yields lower, as their focus returns to the downside risks to inflation.

USD implications: Morgan Stanley expects that 1) the current tariff structure will move to different legal authority and largely remain in place, and 2) refunds will be limited in size (assuming $85bn as the midpoint of our estimated range of outcomes). Reduced latitude from the US administration to use immediate tariff authority as a tool of foreign policy may at the margin diminish the USD-negative risk premium associated with investor caution around maintaining US currency exposure.

However, offsetting factors are likely to maintain (or even widen) this USD-negative risk premium, including geopolitical uncertainty and questions around US currency policy. And the mechanical positive effect on global growth (as tariffs using different authorities take time to be implemented, and may be implemented at lower levels) will likely boost global growth expectations, further weighing on the USD. Therefore we continue to expect USD declines.

Much more in the full Goldman and Morgan Stanley reports, both available to pro subscribers.