Naked 'Private Credit' Swimmers Exposed, Payrolls Plunge As Trump Sparks Week Of "Total, Global F**king Chaos"

Tl;dr: this week was 'extra' as the Millennials say... no way to shorten it up much better than this brief comment from an old friend (options trader in Chicago):

"Trump unleashed total, global, fucking chaos... and then the tide went on private credit's naked swimmers... and then jobs collapsed... I'm ready for a beer!"

Oil to the moon, Nattie to the sun; Dollar up bigly on the week (best week since Oct 2024) - enough to pressure precious metals down; stocks and bonds down (vols up for both); bitcoin unch as it soaked up geopolitical risk like a champ.

First things first... the attack on Iran triggered the biggest weekly jump in WTI crude since... ever (going back to 1990)...

...surging from around $65 last Friday to $90 today...

...to its highest since Oct 2023 (so much for the interventions - insurance/military support of tankers thru Strait of Hormuz, SPR release, easing sanctions, etc)...

...and as we said earlier "higher oil screams higher vol" and judging from the last major geopolitical crisis, there is more pain... and more vol... to come before any reflexive 'ceasefire/settlement' or 'global recession threat' brings an end to it...

Options traders are betting on more with November $100 calls are seeing increased activity, with open interest building even in $120 strikes -- a sign some traders see risks extending beyond a multi-week flare-up.

On a side-note, Vanda Research points out that today saw The United States Oil Fund ETF's (USO) biggest day of retail net buying ($40mn*) – suggesting that long oil may be emerging as the next 'meme theme' for retail investors.

Today surpasses the previous high seen in Apr 2020 when oil prices famously turned negative.

This would lift 5-day net retail buying in USO to $82mn, well above the $67mn peak recorded during the Apr 2020 episode.

It was worse for EU NatGas which exploded higher by over 100% at its peak on the week...

All of which sparked the biggest weekly jump in VIX since Liberation Day (though VIX remains lower than its recent peak in Oct 2025)...

As Goldman Sachs trader, Chris Hussey, summed up, a lot is going on in markets currently, but oil may be the only thing that matters for now... until it doesn't.

Today's Payrolls report came in much weaker than expected with non-farm Payrolls declining by 92K and the unemployment rate ticking up to 4.4%. The implications of declining employment (slower growth) is now weighing on 10-year Treasury yields which are ~5bp lower than they were prior to the Payrolls release.

Also this week, we continue to get more news on the AI disruption trade. Ronnie Walker highlighted how several more companies reporting results over the past 2 months have indicated that AI is saving them money. And Gabriela Borges highlighted how Claude Cowork and OpenClaw are now providing people with active user interfaces that should help to accelerate the adoption of AI as a general intelligence layer in the software stack.

But overshadowing these cyclical (payrolls) and secular (AI) themes this week has been of course oil. About 20% of global oil supply flows through the Strait of Hormuz on the border of Iran, and the conflict that escalated last weekend has significantly reduced this flow this week. Front-month Brent oil is up ~$20/bbl this week to almost $92/bbl, reflecting the supply squeeze underway in the energy complex. Similarly, Dutch nat gas (TTF) has risen by almost 50% this week, reflecting supply shutdowns in Qatar.

Bottom-line: time is of the essence in a market with limited inventory and continuous demand like oil and gas. On Wednesday, we raised our 2Q26 average Brent oil forecast by $10, under the assumption that we will see 5 additional days of very low (15% of normal) Strait of Hormuz (SoH) exports followed by a gradual recovery over 28 days. But that takes us only into early next week.

Stocks ended the week lower... but perhaps not as much as one might have expected. The Dow and Small Caps were the biggest losers (down 3-4%) while Nasdaq (benefiting from some safe-haven flows into the Mega-Caps) outperformed (still down 1-2% of the week)...

Ugly end to the day/week on this HL: "*ORACLE AND OPENAI END PLANS TO EXPAND TEXAS DATA CENTER SITE" dragging ORCL and the AI names lower...

We "broke the box" again today but just as we saw on Tuesday, dip-buyers stepped in...

CTAs in focus: Goldman Sachs traders warned to watch out for the medium-term CTA trend level of 6762, closing below this level today will unlock more supply.

Over the next week, CTAs are sellers in all tape scenarios. In a down tape, they are sellers of $190B, $63.7B of that out of the US.

They also noted 'no reprieve for technicals'.

ETF percent of the tape still extremely elevated at 43% vs YTD avg of 28% (stringly suggesting much more macro positioning/hedging than stock selection).

Top of book liquidity stands at just $3mm vs YTD avg of $10mm.

Risk off sentiment prevails with asset managers currently sitting at a whopping 10% sell skew, seeing notable supply in the financials and industrials sectors.

Mixed bag at the sector level with Energy outperforming (as one would expect) followed by Tech (safe haven flows) and Materials the big laggard (global recession/margins). Defensives like Healthcare and Staples were ugly though (higher yields)...

Mag7 names outperformed the S&P 493 on the week...

Private Credit names were hammered as BlackRock gated funds...

Quite a flip-flop in dispersion this week as correlation-one macro moves dominated with index vol surging more than underlying component vols...

While geopolitical uncertainty (proxied by oil vol) soared, we also saw cross-asset implieds jumping notably with bond vols back to 3 month highs, and FX vol elevated...

Treasuries ended the week with a modest reprieve as dismal jobs data trumped a further surge in oil prices (is this the start of a 'global recession' being priced or just a US-centric kneejerk?)...

...nevertheless, it was an ugly week for bonds with the long-end outperforming as the belly lagged...

A wild week for STIRs with rate-cut odds plunging all week... and spiking today after payrolls...

The dollar saw massive safe-haven flows Monday and Tuesday to end with its best weekly gain since Oct 2024...

...with EUR bearing the brunt of the selling pressure...

The dollar's strength was enough to offset any safe-haven flows into precious metals which had a very tough week (source of funds?) with silver and platinum hit hardest. But we do note that - like the dollar - most of the action was Monday and Tuesday with PMs treading water 'off the lows' since...

We did note that gold's decline stopped dead at $5000 on Tuesday and has waffled sideways to higher since (mirroring the dollar)...

Perhaps most surprising was bitcoin ending the week unchanged as it refused to track big-tech into the abyss and soaked up the more typical geopolitical selling-pressure notably well...

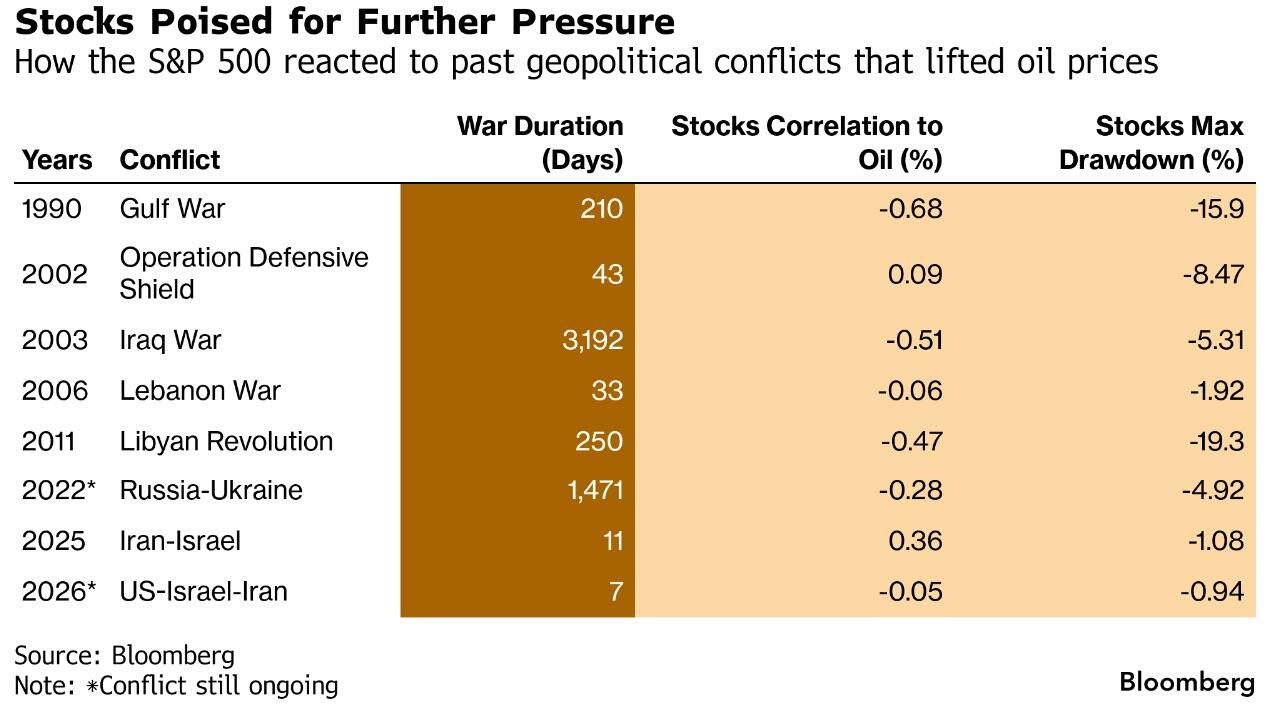

Finally, circling back to where we started, as oil prices keep pushing higher amid the Middle East disruptions, stocks have further reckoning to do if history is any guide.

As Bloomberg strategist Tatiana Darie reports, the table aims to capture some of the major geopolitical events since 1990 that have had an impact on oil prices. Stocks have rarely escaped unscathed, with their correlation to oil flipping negative as energy costs increased. The analysis measured the trough in the S&P 500’s correlation with WTI futures on a 60-day basis during the conflict, or shortly after it began for the lengthier episodes.

As you can see, the reading is barely negative now, with the jump in crude prices just starting to weigh on risk assets. The headline numbers don’t tell the full story either. WTI crude above $85 a barrel means that prices have already surged by more than 50% since their December lows... to their most overbought since 1990...

The upshot from the various studies is that stocks face more downside risk, especially if oil prices approach the much-feared $100 price tag.