US equities futures point to modest gains ahead of this week's flurry of central bank decisions - Newsquawk US Market Open

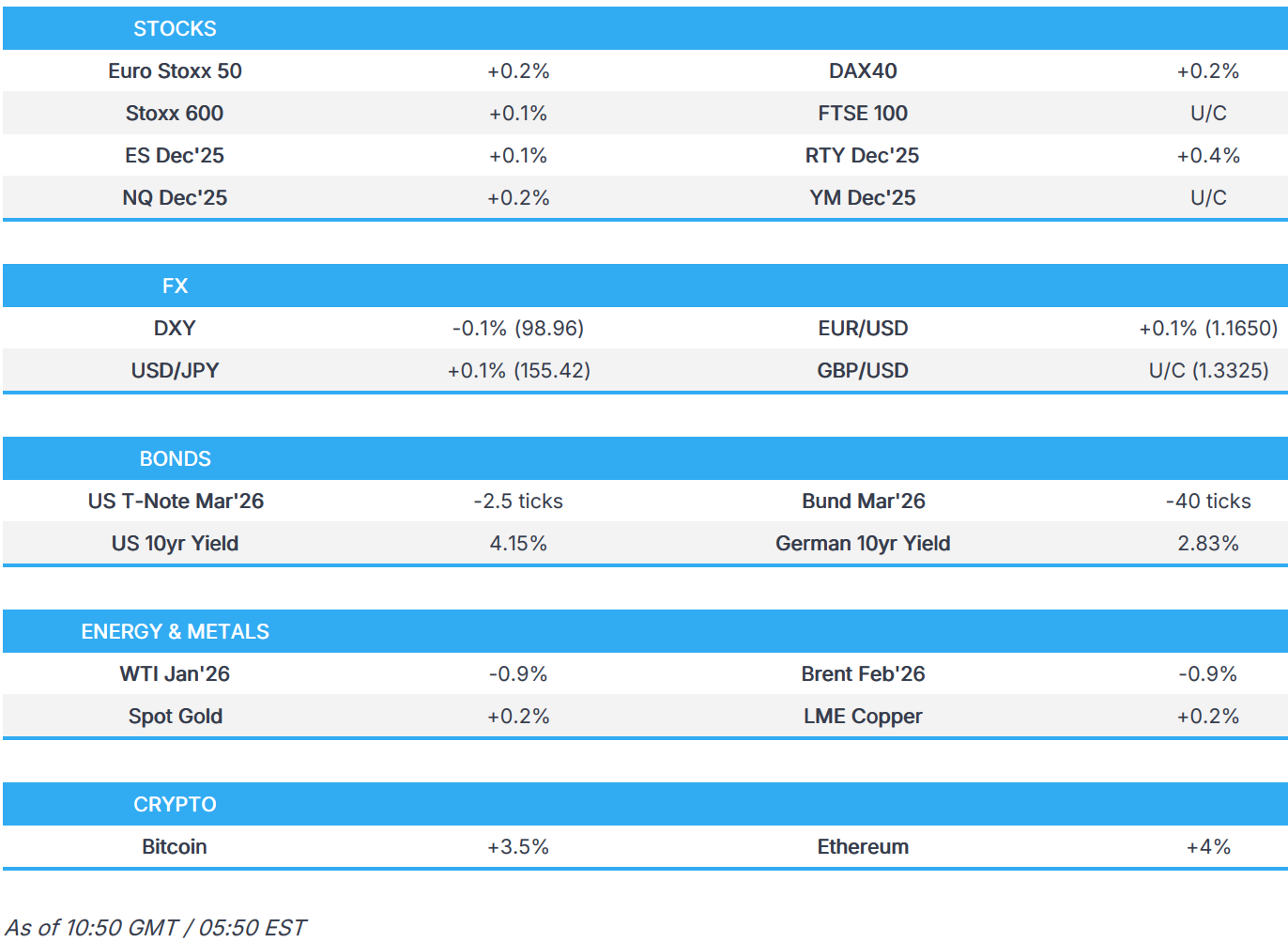

- European bourses attempt to move higher after initial pressure, US equity futures trade with modest gains.

- USD is flat, EUR and NZD manage to hold towards the top of the G10 pile.

- Global bonds pressured, Bunds hit on hawkish remarks via ECB's Schnabel, who said that she is 'comfortable' on bets that the next move will be a hike, albeit not any time soon.

- Crude benchmarks retreat despite a lack of drivers, XAU grinds higher and 3M LME Copper benefits after positive Chinese exports data, though Imports disappointed.

- Looking ahead, highlights include ECB’s Cipollone, BoE’s Taylor & Lombardelli, Supply from the US.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

TARIFFS/TRADE

- US President Trump said we'll work it out, when asked if he would restart trade talks with Canada, while it was separately reported that the Canadian PM’s office said PM Carney agreed with US President Trump and Mexican President Sheinbaum to keep working together on the trade deal.

- USTR said China’s trade commitments are going in the right direction and that they are seen to be in compliance so far.

- French President Macron warned that the EU could hit China with tariffs if nothing is done to reduce its widening trade deficit with the EU, according to Les Echos.

- EU is to expand the carbon border tax to garden tools and washing machines, as it seeks to close loopholes in the law to prevent carbon-intensive imports, according to FT.

- US Embassy in India said US Under Secretary of State for Political Affairs Allison Hooker will visit New Delhi and Bengaluru, India, on December 7th-11th.

- German Foreign Minister said a lot of work is still needed to persuade China to issue general export licenses for rare earths.

- China's Vice Commerce Minister said he welcomes EU automakers to continue to invest in China. Urges Germany and the EU auto association to push the EU Commission to resolve the EV anti-subsidy case. On Nexperia, he said the root cause of chaos in the global semiconductor supply chains lies in the Netherlands.

EQUITIES

- European bourses (STOXX 600 +0.1%) began the morning mixed, with a slight negative bias. Since the open, indices have held an upward bias with some climbing marginally into the green.

- European sectors are mostly lower. Industrials and Tech hold towards the top of the pile, whilst Real Estate and Media lags a touch. In terms of a key story, BNP Paribas (+0.7%) is to sell its stake in AG insurance to Ageas (+2.2%) for EUR 1.9bln.

- US equity futures (ES NQ RTY) are trading on a slightly firmer footing, with some outperformance in the RTY. As for equity stories, some focus has been on comments via US President Trump, who voiced potential antitrust concerns regarding Netflix's planned USD 72bln acquisition of Warner Bros. Discovery. Trump cited the combined entity's potential market share as a "problem".

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY has now returned to flat territory after being dragged lower, but EUR strength as ECB hawk Schnabel said she is 'comfortable' on bets that the next move will be a hike, albeit not any time soon, according to Bloomberg. Little notable reaction was seen in ECB marking pricing throughout 2026, which remains unchanged for rates throughout the horizon, although the EUR strengthened and EZ yields rose.

- The Single Currency was also supported by surprisingly upbeat German Industrial Output data. EUR/USD hit a 1.1672 peak, matching Friday's high, before waning back towards 1.1650 levels. Subsequently, DXY fell to a 98.79 trough before trimming losses back towards near-99.00.

- GBP is subdued by the EUR/GBP cross, which briefly eclipsed its 50 DMA (0.8751) from a 0.8726 low on the back of the aforementioned ECB commentary and data. GBP/USD meanwhile closed around its 200 DMA on Friday and traded below the level (1.3331) throughout most of today's session. In terms of weekend UK newsflow, Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times.

- Other G10s are largely flat with Antipodeans mixed following the Chinese Trade Balance data, which showed a stronger-than-expected recovery in Exports but Imports disappointed. Thus, AUD is subdued ahead of the RBA decision tomorrow, whilst NZD is among the better performers as AUD/NZD falls back after meeting resistance at 1.1500.

- PBoC set USD/CNY mid-point at 7.0764 vs exp. 7.0747 (Prev. 7.0749)

FIXED INCOME

- USTs are trading lower by a couple of ticks, having held a negative bias throughout the European morning. Nothing really much driving things for US paper this morning, and action appears to be following peers and in a continuation of Friday’s losses. Traders await the FOMC meeting mid-week, where a 25bps cut is widely expected – but likely to be subject to dissent from several board members. Back to price action, USTs are trading within a narrow 112-14 to 112-19 range, with today’s trough a tick below that made on Friday. Further pressure could see a retest of the trough made on 20th November at 112-10+.

- Bunds are also pressured, and to a larger magnitude than USTs (but less so than UK paper). The benchmark followed US paper overnight, and held a negative bias, before taking a leg lower on comments via Schnabel. The arch-hawk, speaking on Bloomberg, said that she is 'comfortable' on bets that the next move will be a hike, albeit not any time soon. In an immediate reaction, Bund Mar’26 fell from 127.98 to 127.80 over the course of around 5 minutes, before then extending to a trough of 127.74; from a yield perspective, the 10-year rose 3bps to 2.83%, levels not seen since March. Elsewhere, other ECB members have not impacted assets quite so much, with Rehn suggesting that “inflation expectations have remained quite well anchored around the 2% target.”, via Econostream. And finally on the data front, German Industrial Output M/M rose more than expected; ING’s Brzeski said “there are at least tentative signs of a bottoming out” in the German economy.

- Gilts underperform vs peers, and are currently down by around 40 ticks. Price action has been fairly muted this morning, gapped lower at the open and has resided at the bottom end of a 90.90 to 91.11 range. Pressure today in tandem with US/German paper, but with underperformance perhaps explained by ongoing domestic political updates. Focus has been on reports that Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times. Moreover, perhaps some focus on political instability within the Labour Party as PM Starmer floats the return of Angela Rayner. Elsewhere, a KPMG/REC survey showed the UK labour market weakened further in November.

COMMODITIES

- WTI and Brent oscillated in a tight USD 59.98-60.27/bbl and USD 63.63-63.94/bbl, respectively, throughout the APAC session. As the European session got underway, benchmarks failed to extend the highs of the APAC session and reversed lower to dip below USD 60/bbl and USD 63.50/bbl, despite a lack of crude-specific newsflow. Currently, benchmarks are extending on session lows as progress on a potential peace deal between Ukraine and Russia remains in focus.

- Spot XAU edged higher throughout the APAC session amid a weaker dollar ahead of Wednesday's FOMC rate decision, in which the Fed is expected to cut rates by 25bps at its meeting on Wednesday. XAU hit a low of USD 4191/oz as the APAC session commenced and gradually traded higher to a peak of USD 4219/oz as the European session got underway. Data over the weekend showed that the PBoC increased its gold reserves for a 13th consecutive month.

- 3M LME Copper extended to a new ATH of USD 11.75k/t as China's Politburo reiterated its stance that monetary policy is to be moderately loose, setting domestic growth as its top economic priority. This comes amid new demand, fuelled by AI infrastructure build and EVs, coming up against a tight global supply. China's exports also rose in November to 5.9%, compared to the expected 3.8% and the October figure of -1.1%.

- UAE Energy Minister said overall demand for energy will increase, fossil fuels will be "a percentage of it". Adds that natural gas is important and they intend to not only satisfy their local demand but also grow exports of their LNG. Agrees that natural gas demand is more than the projects they are seeing.

- Russia's Kremlin said India buys energy where it is profitable to; as far as Russia understands, India will "continue to do that".

- EU to delay proposals on carbon border tariff and proposals for automotive sector, including Co2 emissions to December 16th, according to a document seen by Reuters.

NOTABLE DATA RECAP

- EU Sentix Index (Dec) -6.2 vs. Exp. -7.0 (Prev. -7.4)

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer said former Deputy PM Angela Rayner will return to the cabinet after resigning in September, while he described her as “hugely talented”.

- Tony Blair is reportedly exploring alternative Labour leadership options amid frustration with UK PM Starmer’s direction, according to The Times.

- ECB's Schnabel said she is 'comfortable' on bets that next move will be a hike. Later on, she also said she would be ready to succeed President Lagarde if she were asked to, via Bloomberg. She said the euro economy is on course to grow above potential despite the headwinds, and the economic outlook has brightened and the downside risks to growth have been reduced significantly, and uncertainty has come down quite quickly, which should further support future economic activity. The global economy and global trade have proven to be more resilient. On inflation, she said it’s in a good place. It’s currently around 2%, and we also project medium-term inflation to be around 2%. Volatile energy prices and related base effects may push headline inflation temporarily below our target. Services inflation has been much stickier than expected. The downward pressure on goods inflation due to a stronger euro, lower energy prices and potential trade diversion from China has been weaker than expected. On policy, she said interest rates are in a good place. Rather comfortable with those expectations of the next move being a rate hike. A first rate hike in June 2026 remains very uncertain.

- ECB's Rehn said the ECB is concerned about central bank independence in the US, via Econostream. Adds that Fed independence is an important issue for "all of us globally". On an insurance cut, said "we are not in the insurance business, not in December, March or June". Inflation expectations have remained quite well anchored around the 2% target. German spending to have a "formidable positive impact" on Germany and the Euro area.

- ECB’s Rehn said they must be aware of upside and downside inflation risks, while he added that inflation risk is slightly tilted to the downside in the medium-term. Furthermore, he said they should not impose unnecessary bars or floors on policy, and that the position on interest rates is not fixed.

- French President Emmanuel Macron called for a change in the ECB’s approach to monetary policy to boost the single market and protect it from the risks of a financial crisis, while he commented that reasserting the value of the European internal market means it can't let inflation be its sole objective, but also growth and employment.

- European Commission may announce a package to support the auto industry on December 16th, according to industry sources.

- German Chancellor Merz and French President Macron are set to discuss the fate of the Franco-German fighter jet project FCAS in the week of December 15th, according to an industry source.

- Germany's auto industry body VDA said it expects 2026 registrations to rise 2% to 2.9mln. Electric car sales in Germany to jump 17% to 979k in 2026. Expects the nation to remain the world's second-largest EV producer in 2026.

- French Socialist Party (PS) leader Faure said the party will vote for the French budget's social security programme.

NOTABLE US HEADLINES

- US President Trump said the Netflix (NFLX)-Warner Brothers (WBD) deal has to go through the process, while he will be involved in the decision, and said it represents a big market share, which could be a problem.

- US President Trump signed a Presidential Memorandum directing the HHS to fast-track a comprehensive evaluation of the vaccine schedules from other countries around the world, and better align the US vaccine schedule.

- White House said it will establish food supply chain security task forces to protect competition.

- US Treasury Secretary Bessent said the US will finish the year with 3% GDP growth.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu said he will meet with US President Trump this month, while he said they believe there is a path to a workable peace with their Palestinian neighbours and that the sovereign power of security from the Jordan River to the Mediterranean will always remain in Israel’s hands. Furthermore, he said political annexation of the West Bank remains a subject of discussion, and the status quo in the West Bank will remain for the foreseeable future, as well as noted that they are close to the second phase of Trump’s Gaza plan.

- Palestinian PM Mustafa said Israel is stepping up the ‘creeping annexation’ of the West Bank and is intensifying efforts to make the West Bank unliveable and drive people out of the occupied territory, according to FT.

- Turkey’s Foreign Minister said Hamas is ready to hand over the Gaza administration to the Palestinian committee to advance the Gaza ceasefire deal. He also commented that Hamas disarmament in the first phase of the Gaza deal may not be a realistic and doable objective, while other steps are needed first.

- US, Israel and Qatar were reportedly holding a trilateral meeting in New York on Sunday to rebuild relations, according to Axios.

- A US official said the US is pushing Ukraine to agree "faster" to the peace plan, according to AFP.

RUSSIA-UKRAINE

- Ukraine's President Zelensky says no accord so far on Ukraine's Donbas in US talks, via Bloomberg.

- Ukrainian President Zelensky said he had a substantive call with US envoy Steve Witkoff and Jared Kushner, while he stated they agreed on the next steps and format for talks with America, as well as noted that Ukraine is determined to continue working honestly with the US side in order to bring real peace. Zelensky separately commented that talks with US representatives on a peace plan were constructive but not easy.

- Ukrainian military conducted a strike on Russia’s Ryazan oil refinery.

- Russian Defence Ministry said Russian forces captured Kucherivka in Ukraine’s Kharkiv region and completed the capture of Rivne in Ukraine’s Donetsk region, while they carried out a group strike on Ukraine’s transport infrastructure facilities, fuel and energy complexes, and long-range drone complexes.

- Russia and China held their third joint anti-missile drills on Russian territory.

- Japanese Chief Cabinet Secretary Kihara said China’s claims about the Japan Self-Defence Force’s dangerous flight are inaccurate, while he added it is very important to gain an understanding of other countries, including the US, regarding Japan's stance.

- Japan is reportedly frustrated at the Trump administration’s silence over the row with China and urged the US to give PM Takaichi more public support, according to FT.

- Australia’s Defence Minister Marles said they are deeply concerned about the actions of China following the air incident near Japan, while Marles discussed with Japanese Defence Minister Koizumi common serious concerns about the situation in the South China Sea and East China Sea. Furthermore, they discussed how to work together to maintain a free and open Indo-Pacific, while Marles also commented that they want the most productive relationship they can achieve with China.

- Pakistan and Afghanistan exchanged heavy fire in a border region on Friday.

- Thai Army spokesman said their military launched airstrikes in the disputed border area with Cambodia.

- The Chinese Foreign Ministry said China believes both countries can win from cooperation on the new US defence strategy. Also said it stands ready to work with the US to improve ties and that China will firmly defend its sovereignty.

- Rapid Support Forces confirms control of Heglig oil field, the largest oil field in Sudan, according to Sky News Arabia.

- Russia’s Kremlin said it welcomed the removal of Russia from the list of US direct threats in the new national security strategy.

OTHER

- Japanese Defence Minister Koizumi said Chinese military planes directed radar at Japan's self-defence forces twice. It was separately reported that Japanese PM Takaichi said the incident involving Chinese fighter jets directing radar at Japanese planes is extremely regrettable, while she said they will respond calmly and resolutely to the development.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 92k, whilst Ethereum gains to a larger magnitude and climbs to USD 3.2k.

APAC TRADE

- APAC stocks were mixed following a lack of major macro drivers over the weekend and with markets tentative ahead of this week's risk events, while participants also digested data, including the latest Chinese trade figures.

- ASX 200 was subdued amid somewhat mixed trade data from Australia's largest trading partner and as the RBA kick-started its 2-day policy meeting.

- Nikkei 225 traded indecisively following a slew of mixed data from Japan, including firmer-than-expected Labour Cash Earnings and disappointing revisions to Q3 GDP, while sentiment was also clouded by geopolitical tensions after Japan accused Chinese fighter jets of aiming military radar at Japan's Self-Defence Force jets.

- Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark underperforming as gains in tech were overshadowed by losses in the big banks, while participants also digested the latest Chinese trade data, which showed a stronger-than-expected recovery in Exports but Imports disappointed.

NOTABLE ASIA-PAC HEADLINES

- China's Politburo held a meeting on the economy and reiterated its stance that monetary policy is to be moderately loose, with fiscal policy being more proactive, while it stated that the economic operation is generally stable and it will implement more active macro policies. Furthermore, it will continue to prevent and resolve risks in key areas, as well as stabilise employment, markets, and enterprises' expectations.

- Hong Kong held its legislative election on Sunday to elect 90 Legislative Council members from the 161 government-vetted candidates.

- Australia Treasurer Chalmers said they will not extend electricity rebates and that the mid-year review will not be a mini budget, while he added that the review will include savings.

- BoJ Governor Ueda to attend Japan's lower house budget committee from 05:35-06:05 GMT on Tuesday, according to a parliamentary source cited by Reuters.

- Chinese President Xi held a meeting with non-party members on the economy, according to Xinhua, and said China to stabilise jobs and markets. said 2025 has been unusual and will smoothly meet the main targets. To reinforce economic growth momentum. Economic goals will be achieved this year. To drive reasonable economic growth.

- China's auto industry body CPCA said China sold 2.24mln passenger cars in November, down 8.5% Y/Y; Tesla (TSLA) exported 13,555 China-made vehicles (prev. 35,491 in October).

- Indonesian Finance Minister said the nation is to impose a coal export tax near year between 1% and 5%.

- China to cut retail gasoline price by CNY 55/t, and to cut retail diesel price by CNY 55/t

DATA RECAP

- Chinese Trade Balance (USD)(Nov) 111.68B vs. Exp. 100.15B (Prev. 90.07B)

- Chinese Exports YY (USD)(Nov) 5.9% vs. Exp. 3.8% (Prev. -1.1%)

- Chinese Imports YY (USD)(Nov) 1.9% vs. Exp. 3.0% (Prev. 1.0%)

- Chinese Trade Balance (CNY)(Nov) 792.57B (Prev. 640.49B)

- Chinese Exports YY (CNY)(Nov) 5.70% (Prev. -0.80%)

- Chinese Imports YY (CNY)(Nov) 1.70% (Prev. 1.40%)

- Japanese GDP Revised QQ (Q3) -0.6% vs. Exp. -0.5% (Prev. -0.4%)

- Japanese GDP Rev QQ Annualised (Q3) -2.3% vs. Exp. -2.0% (Prev. -1.8%)

- Japanese Labour Cash Earnings (Nov) 2.6% vs Exp. 2.2% (Prev. 1.9%, Rev. 2.1%)

- Japanese Real Cash Earnings YY (Oct) -0.7% vs Exp. -1.2% (Prev. -1.4%, Rev. -1.3%)

Loading...