US equity futures trading flat going into the Christmas holidays - Newsquawk US Market Open

- Japan is to reduce its new issuance of super-long JGBs next fiscal year to around JPY 17tln, according to Reuters sources.

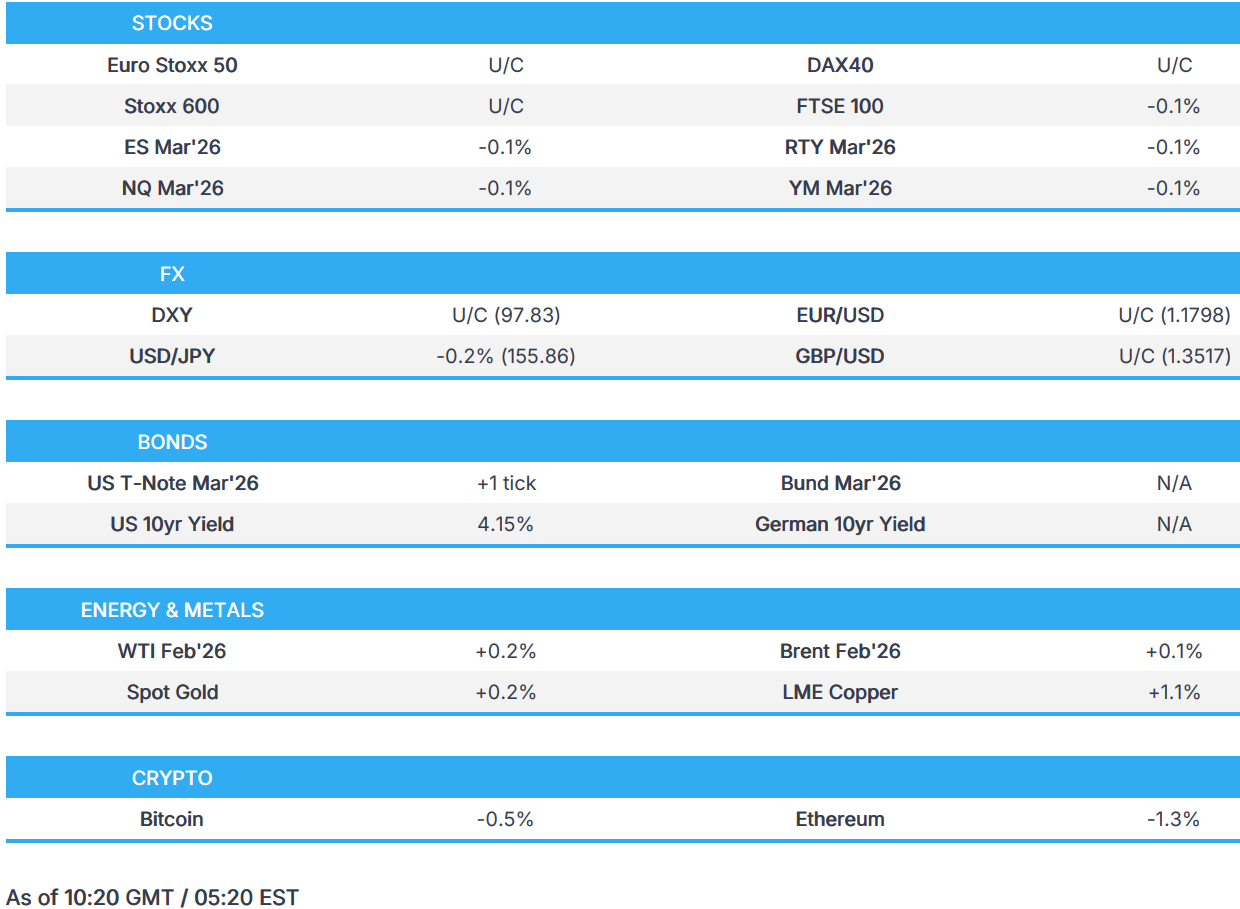

- European equity futures are closed as Eurex observes the Christmas Eve holiday. US equity futures are very modestly lower in thin conditions.

- DXY is flat, JPY is very mildly stronger continuing recent advances.

- JGBs soft overnight but have been driven higher in recent trade, USTs flat.

- Crude benchmarks are incrementally firmer, with spot gold also steady.

- Looking ahead, highlights include US Jobless Claims (w/e 20 Dec), Supply from the US.

- Note: The Newsquawk desk will run until 18:05GMT/13:05EST on Wednesday, 24th December. FOMC Minutes on 30th December 2025 will be covered. Normal service will resume at 0700GMT/02:00EST on Friday 2nd of January 2026 for the beginning of the European Session.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EQUITIES

- The FTSE 100 (-0.1%) is incrementally this morning, whilst the CAC 40 is posting marginal gains; cash trade for DAX 40, FTSE MIB and the SMI remain shut on account of Christmas Eve.

- US equities futures are slightly lower, with limited catalysts in quiet trade. Italy's Competition Authority has ordered Meta (META) to suspend the terms excluding competing AI Chatbots from WhatsApp.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is essentially flat and trades within a narrow 97.74 to 97.96 range. Nothing really driving things for the index this morning, given the usual holiday-lull. Traders will await Jobless Claims later today, but aside from that the docket is void of anything pertinent from a Dollar perspective. G10s are also broadly little changed vs the USD, aside from the JPY which is the marginal outperformer this morning.

- JPY marginally strengthened against the USD in overnight trade, but without a specific catalyst. The strength likely a continuation of the more aggressive jawboning heard via Finance Minister Katayama earlier in the week, where she stated they had a “free hand” to take bold action in the FX market. Thereafter, in the European session, Reuters reported that Japan is to reduce its new issuance of super-long JGBs next fiscal year to around JPY 17tln. A source report which comes after PM Takaichi rejected any "irresponsible bond issuance or tax cuts". USD/JPY currently trading at the lower end of a 155.57 to 156.28 range.

- South Korean Presidential office said they are closely watching FX.

- South Korea's pension fund said to implement strategic foreign exchange hedging measures, according to Reuters sources.

- Brazilian Central Bank to offer USD 2bln in Dollar auction with repurchase agreements on 26th December.

FIXED INCOME

- EGBs closed.

- JGBs were firmer for much of the overnight session but spent it drifting lower, paring recent Takaichi-inspired gains. The main move came in the European morning as Reuters reported that Japan is set to cut 2026 ultra-long JGB issuance by around JPY 17tln, a report that in a somewhat delayed reaction, lifted JGBs by around 20 ticks to a test of 133.00 to the upside. Reminder, BoJ's Ueda is tentatively scheduled to speak on Christmas Day.

- USTs in a thin 112-08 to 112-12+ band. Docket ahead features US weekly jobless claims and then a 7yr auction after the 5yr auction on Tuesday, a tap that was mixed overall with a better tail though the b/c was below the prior.

- Gilts opened flat just above 91.00 before dipping to a 90.80 trough and then rebounding back to the figure with specifics light.

- Japan is to reduce its new issuance of super-long JGBs next fiscal year to around JPY 17tln, according to Reuters sources. JGB Mar'26 lifted from 132.78 to a test of 133.00 to the upside in the 15-minutes from 09:10GMT following this report.

COMMODITIES

- As Christmas Eve trade gets underway, WTI and Brent briefly pulled back to USD 58.25/bbl and USD 62.22/bbl before extending on Tuesday’s gains to peak at USD 58.76/bbl and USD 62.76/bbl as the European session continues.

- Spot XAU briefly extended above USD 4500/oz, continuing the gains made in the metal space this year, before a sharp pullback as traders take profit going into Christmas. XAU peaked at USD 4526/oz early in the APAC session before the sharp pullback to USD 4471/oz. Thus far, the yellow metal continues to hover just below USD 4500/oz as light European trade continues.

- 3M LME Copper is set for its best year since 2009, helped by the near 7% gains made in December. After setting a new ATH of USD 12.17k/t in Tuesday’s session, the red metal opened just shy of the ATH but pulled back to a trough of USD 12.06k/t, filling the price gap. Just as the European session got underway, 3M LME Copper surged higher to a new ATH of USD 12.28k/t and holds above USD 12.2k/t as the European morning continues.

- Naftogaz announces that Russia attacked Ukraine's oil and gas infrastructure overnight.

- Shell's (SHEL LN) manufacturing centre, Corunna, reported potential for increased flaring and noise for the next few hours due to process interruption.

- US Private Inventory (bbls): Crude +2.4mln (exp. -2.4mln), Distillate +0.7mln (exp. +0.4mln), Gasoline +1.1mln (exp. +1.1mln), Cushing +0.6mln.

- US Private Inventory Expectations (bbls): Crude (exp. -2.4mln), Distillate (exp. +0.4mln), Gasoline (exp. +1.1mln).

TRADE/TARIFFS

- Chinese Commerce Ministry holds roundtable with foreign trade firms.

- China's Foreign Ministry said we firmly opposes the indiscriminate use of chip tariffs and unreasonable suppression of China by the US. Urges the US to correct its wrong practices. Will take corresponding measures to safeguard rights and interests if the US persists.

- Japan and US agree to expedite the USD 550bln investment project, according to Bloomberg, citing a statement.

CENTRAL BANKS

- BoJ Oct 29–30 meeting minutes (two meetings ago): Members agreed the BoJ will continue to raise rates if economic and price forecasts materialise. Many members said the likelihood of economic and price forecasts materialising has heightened, but must maintain policy to confirm whether positive wage-setting behaviour will not be disrupted. One member said the timing of a rate hike is approaching, but authorities should wait a bit longer to scrutinise the direction of the new administration’s policies.

NOTABLE US HEADLINES

- US President Trump posted "Growth is up and Inflation is down in President Trump’s first year".

- US NEC Director Hassett said President Trump has "a bunch of great Fed chair candidates", via Fox Business; Precious metals are skyrocketing for good reason.

NOTABLE US EQUITY HEADLINES

- Italian Competition Authority has ordered Meta (META) to suspend the terms excluding competing AI Chatbots from WhatsApp. "Meta’s conduct appears to constitute an abuse, since it may limit production, market access or technical developments in the AI Chatbot services market, to the detriment of consumers. Moreover, while the investigation is ongoing, Meta’s conduct may cause serious and irreparable harm to competition in the affected market, undermining contestability.".

- Snowflake (SNOW) is reportedly in talks to purchase Observe for around USD 1bln, according to The Information.

- Apple (AAPL) CEO reportedly bought some USD 3mln of Nike (NKE) stock, according to Barrons.

- Lockheed Martin (LMT) awarded USD 10bln modification to previously awarded US Air Force contract, according to Pentagon.

- Boeing (BA) awarded USD 2bln contract by US Air Force, according to Pentagon.

GEOPOLITICS

RUSSIA-UKRAINE

- Russia's Kremlin announces that Special Envoy Dmitriev has reported to Putin on the trip to the US; On peace deal, says Russia will now formulate its position and continue contacts in very near future.

- Naftogaz announces that Russia attacked Ukraine's oil and gas infrastructure overnight.

- Ukrainian President Zelensky said we are significantly closer to finalising a plan with the US but mainly split on territorial issues. Ukraine expects an answer from Russia on Wednesday to end the war. Draft plan opens the way for 'potential' demilitarised zones and freeze combat on current lines. Plan does not require Kyiv to formally renounce NATO bid.

- Ukrainian drone attack sparks fire at industrial site in Russia's Tula region, according to the regional governor.

MIDDLE EAST

- Russian President Putin said Russia "reject Israel's repeated violations of Syrian territory", via Al Arabiya.

CRYPTO

- Bitcoin is a little lower and trades around USD 87k whilst Ethereum holds around USD 2.9k.

APAC TRADE

- APAC stocks traded mixed and within narrow ranges following a largely positive lead from Wall Street. APAC lacked conviction amid light newsflow and anaemic volumes as markets wound down ahead of the holidays.

- ASX 200 edged lower, with weakness in Tech and Healthcare outweighing strength across the mining complex.

- Nikkei 225 held onto modest gains, oscillating around the 50.5k level despite JPY strength, supported by a calmer domestic bond market.

- Hang Seng and Shanghai Comp varied, with little in the way of fresh domestic catalysts. Price action broadly reflected the indecisive regional risk tone.

NOTABLE APAC HEADLINES

- Earthquake of magnitude 5.50 hits Taipei, via Reuters witnesses.

NOTABLE APAC DATA RECAP

- Japanese Leading Index Final (Oct) 109.8 (Prelim. 110).

- Korea (Republic of) Consumer Sentiment Ind (Dec) 109.9 (Prev. 112.4).

Loading...