BOA's New Gold Thesis: China Mandates, CB Buying Growth, and Trade Wars

Backdrop

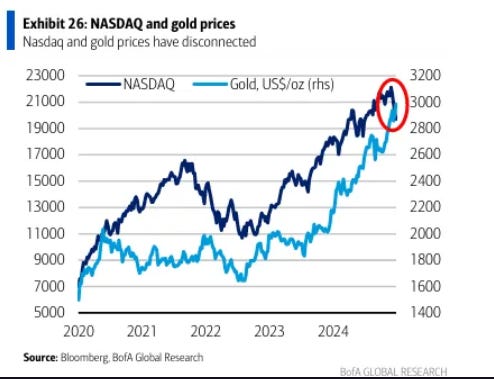

Last week, two important Bank reports covering gold were released almost simultaneously.one was by Bank of America; the other by Goldman Sachs. ZH Broke down both of these reports in Gold Surges Back To Record High As Goldman/BofA Hike Price Targets Notably, since those two reports were released (see pic), gold rallied a massive $120 in three trading sessions from $3,000 to $3120.

The Goldman report gave an upside scenario where $4,500 could be touched. The BOA report discussed and quantified new drivers that could give rise to such a price scenario. Today we breakdown the first of the reports against this backdrop of a North American reawakening to Gold and Silver as not just inflationary hedges but protection against the trade wars to come

Bank of America’s $3,500 New Gold Thesis: China Insurance, CB Buying Growth, and Trade Wars

Authored by GoldFix exclusively for ScottsdaleMint

Bank of America’s March 25th gold report, titled “Gold Plating Guns and Cannons,” presents a multi-faceted thesis for a sustained rise in the gold price. While the title leans metaphorical—there is no actual mention of gold plating, guns, or cannons—the framing is clear: gold is increasingly entangled with trade conflict, and geopolitical realignment. The bank raises its long-term price forecast for gold to $3,500/oz, and in doing so, provides a more quantified, institutional framework for understanding where the next leg of demand will come from.

This essay breaks down that thesis across three structural vectors: (1) the emergence of new sovereign and quasi-sovereign gold buyers, (2) the impact of trade and monetary policy on U.S. dollar weakness and reserve behavior, and (3) the rejection of legacy frameworks such as the Mar-a-Lago Accord. Bank of America’s language, while restrained, is revealing. The message is unambiguous: the world is rebalancing, and gold is at the center.

I. The Core Thesis: $3,500 with Structural Demand Expansion

The opening paragraph of the report formalizes Bank of America’s upgrade to a $3,500/oz gold price target, contingent on a 10% increase in investment demand. The headline target is straightforward, but the significance lies in how the bank quantifies that demand increase across three key cohorts:

-

Chinese Insurance Companies- new buyers with a 300 tonne mandate

-

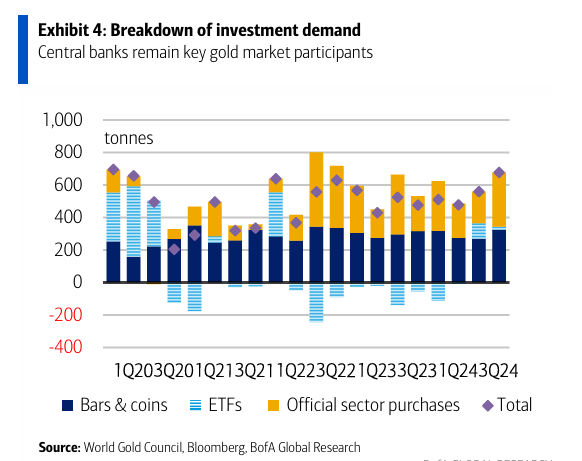

Central Banks- to triple total purchases over several years

-

Retail Investors- peak buying adds an additional $600 to price

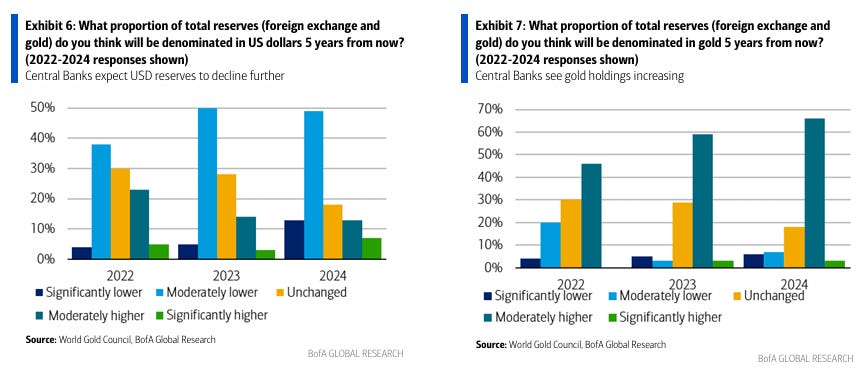

Each category is given a back-of-the-envelope estimate that, when combined, easily justifies the 10% demand increase. For example, the Chinese insurance industry is expected to allocate 1% of assets to gold, equivalent to 6.5% of the annual global gold market. Central banks, currently holding ~10% of reserves in gold, are projected to increase that allocation to 30%, based on portfolio optimization principles. Retail investor flows into physically backed ETFs have also resumed, up 4% year-to-date.

“Having hit our long-term price target of $3,000 per ounce, we believe gold could rally to $3,500 if investment demand increases by 10%." — BofA

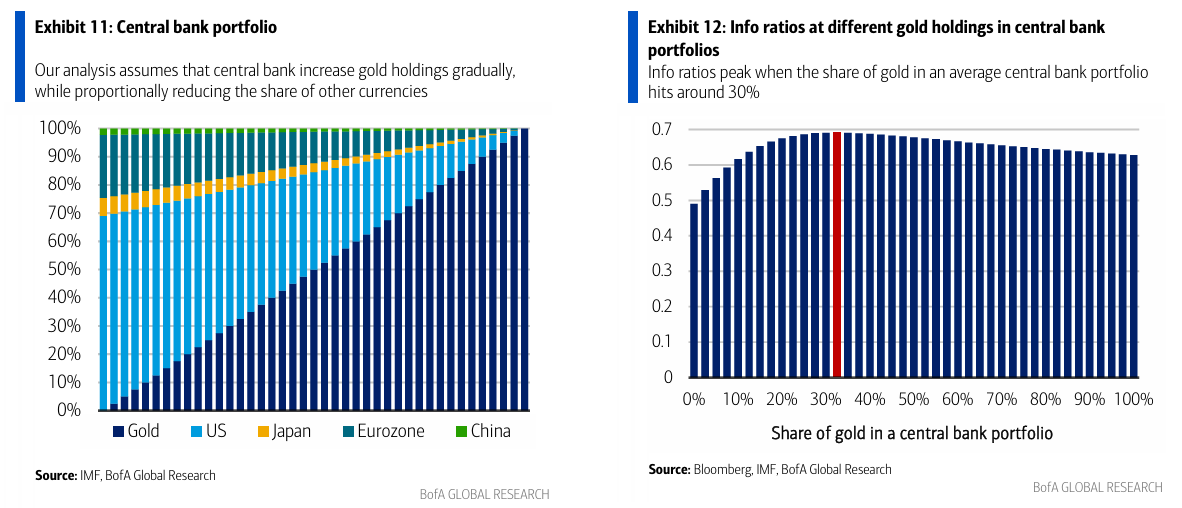

II. Central Bank Buying: Portfolio Optimization and the Efficient Frontier

The most analytically rigorous section of the report is the treatment of central bank gold accumulation. The bank explicitly states that central banks may pursue a 30% gold reserve allocation—up from the current 10%—as part of a broader portfolio optimization exercise. Utilizing efficient frontier theory, Bank of America argues that increasing gold exposure enhances risk-adjusted returns for central bank portfolios, particularly in an environment of deglobalization, weaponized finance, and sanction risk.

“Central banks currently hold around 10% of their reserves in gold, which could raise this figure to 30% to make their portfolios more efficient.”

This is a marked departure from prior analyses that focused solely on flow data or backward-looking trends. Instead, Bank of America offers a destination projection, more compatible with Goldman Sachs’ flight path approach than the other bank commentaries.

III. The Twin Deficits and Policy Dislocation: A Gold Catalyst

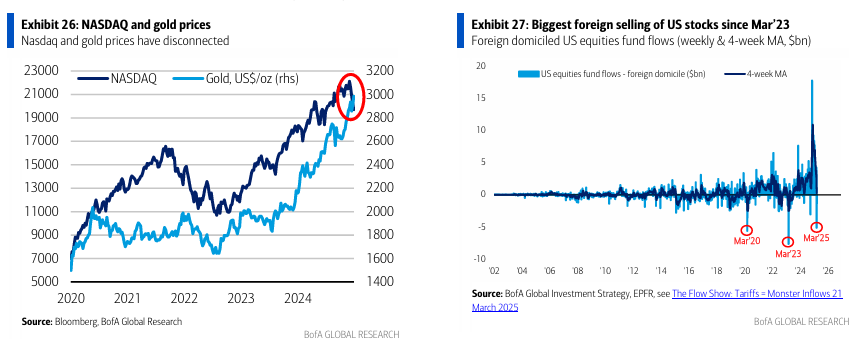

Bank of America argues that America’s twin deficits—budget and current account—are direct catalysts for dollar debasement and gold appreciation. Trump-era trade policies, particularly tariffs, are not seen as temporary distortions but as the beginning of a structural adjustment.

“There is no silver bullet to reduce U.S. twin budget and current account deficits… A shift from America First to America Alone may lead central banks to further reduce dollar holdings, with gold as a beneficiary.”

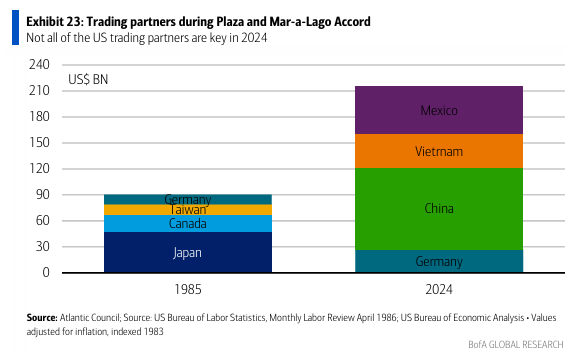

IV. Rejection of the Mar-a-Lago Accord: An Implausible Solution

The report decisively dismantles the so-called “Mar-a-Lago Accord,” a proposed modern version of the 1985 Plaza Accord. The proposal envisioned a coordinated weakening of the U.S. dollar alongside extending Treasury maturities to 100 years.

“In contrast to the Plaza Accord, not all U.S. trade partners are allies… The proposed Treasury maturity extension is effectively a default through the back door.”

Bank of America dismisses the Accord on three grounds: lack of multilateral alignment, reputational damage from Treasury manipulation, and an absence of geopolitical trust.

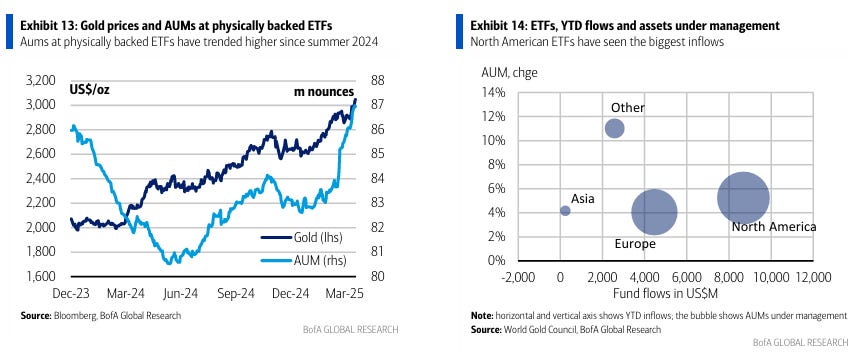

V. ETF Flows and Retail Participation: The Swing Variable

While sovereign and institutional demand forms the structural base, ETF flows represent the tactical driver. BofA notes a 4% YTD increase in physically backed ETF assets.

Assuming no significant decline in CB buying, and no increase either; Price will increasingly track Global ETF purchases Therefore next time ETF money approaches levels seen in July 2020 or Feb 2022, we should see an additional $600, and possibly $1,285 on top of current prices; Placing the Price between $3600 and $4285 if/when those ETF levels are reached. Circumstances matter: It must be noted, ETF buying will be even more panicky in getting to those prior levels if stocks are dropping, implying much more impulsive moves and likely massive price rallies in miners.

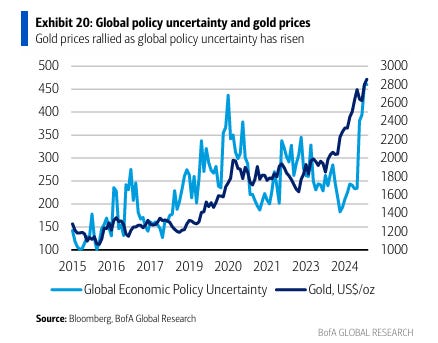

VI. Macro Landscape: Policy Misalignment and the Powell Dilemma

The Fed remains in a “wait-and-see” stance, navigating between inflation control and recession avoidance. Trump’s tariffs complicate the equation, introducing policy misalignment between fiscal and monetary arms.

“Differing views highlight again that U.S. authorities are implementing a set of policies that are at stages not entirely aligned. One reason gold keeps pushing higher.”

This misalignment injects policy-driven volatility into risk markets, reinforcing gold’s role as a stabilizer.

Conclusion: Higher Equilibrium, Institutional Validation

Bank of America’s report is not just a price upgrade; it’s an institutional validation (an admission and a confirmation) of gold’s structural bull market. Its value lies not in the price target alone, but in the methodology: quantified, multi-sourced, and historically anchored. Whether through sovereign reserve diversification, insurance industry mandates, or a shifting macro landscape, the case for $3,500 is grounded in the realignment of global capital.

The Mar-a-Lago Accord is dismissed as theatrics. The real accord is already happening—between inflation risk, geopolitical fragmentation, and the rise of multipolar monetary policy regimes. Gold, in this view, is no longer a hedge. It is monetary ballast in a world shifting beneath its feet.(See Analysis: The BOA $3500 Price Target Report Breakdown for complete walkthrough)

///END///////////////////////////

RELATED:

- Gold “Unshackled”: Major Banks Race to Raise Price Targets. [Unlocked]

- We will break down the Goldman analysis later this week

Free Posts To Your Mailbox