SocGen: The Gold Market You Think Exists Doesn’t Exist Anymore

SocGen: Central Banks Are Price-Insensitive — That’s What’s Driving Gold

Authored by GoldFix

Gold’s price no longer responds to a single demand driver. The data shows shifting elasticities across jewellery, investors, ETFs, and central banks, and these shifts reveal where price discovery is actually happening today. Part 1 maps the new drivers that now define the market. By the way; This is the second bank to assert CB buying has become price insensitive, with DB (excerpted below as well) doing so just last week. Soc Gen goes a step further and compares banks to other cohorts for effect.

I. Overview: Sectoral Differences and the Demand Puzzle

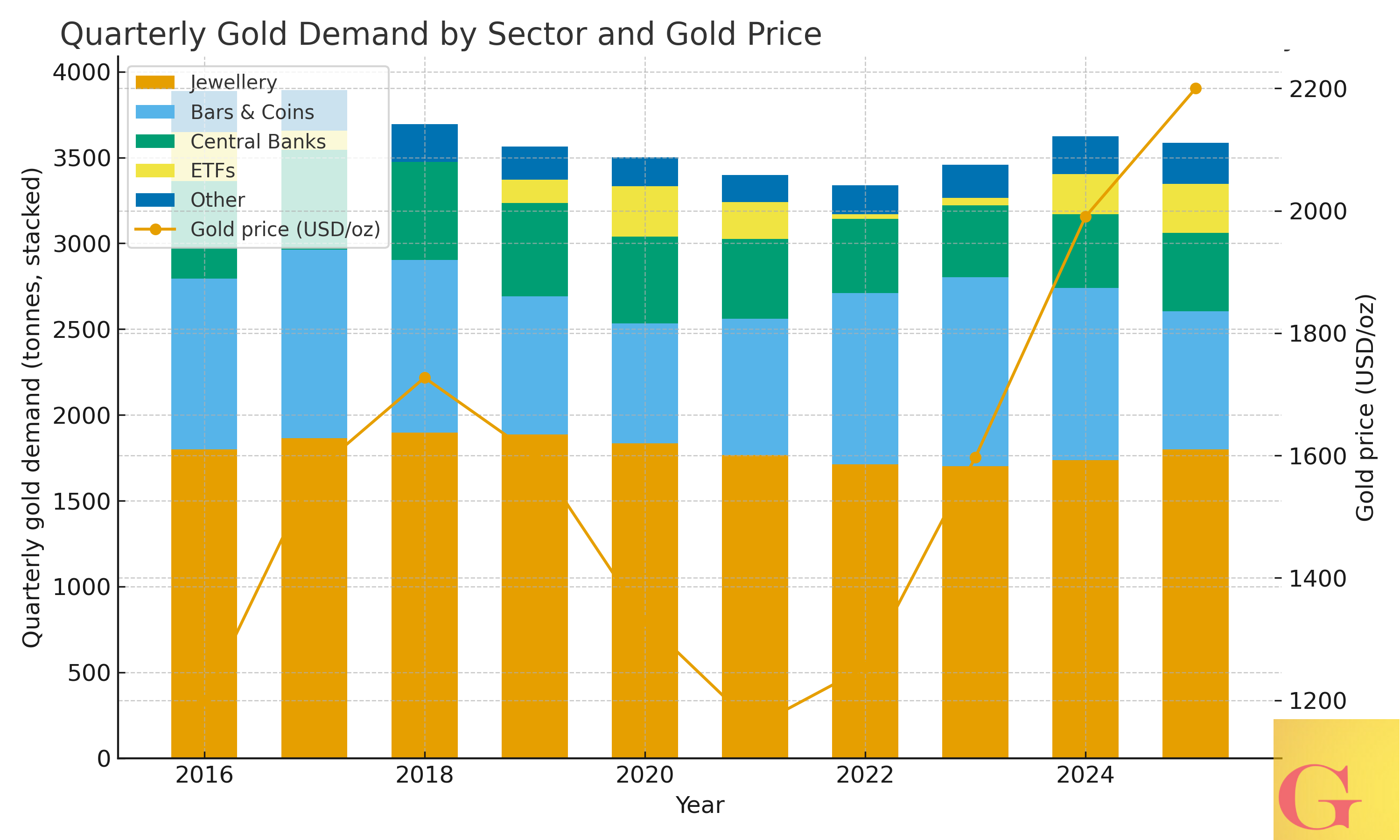

The relationship between gold demand and the price of gold is often treated as stable and intuitive, with jewellery consumption acting as the dominant and persistent anchor of physical demand. Since 2010, jewellery has consistently accounted for more than three hundred tonnes per quarter, followed by bars and coins. But…

Central bank purchases and ETF flows have attracted growing attention in recent years as gold shifted into a more global role. Societe Generale’s Commodity Compass Analytics report examines whether the traditional elasticity relationships have evolved in a way that weakens the link between price and demand across these market segments.

The analysis relies on quarterly data from the World Gold Council and pricing from the London Bullion Market Association. The findings point toward significant sectoral variation, with elasticities that have shifted meaningfully since the onset of the Covid period and through the subsequent recovery cycle.

“The decline in jewellery demand over the past year appears to align with normal elasticity expectations rather than structural breakdown.”

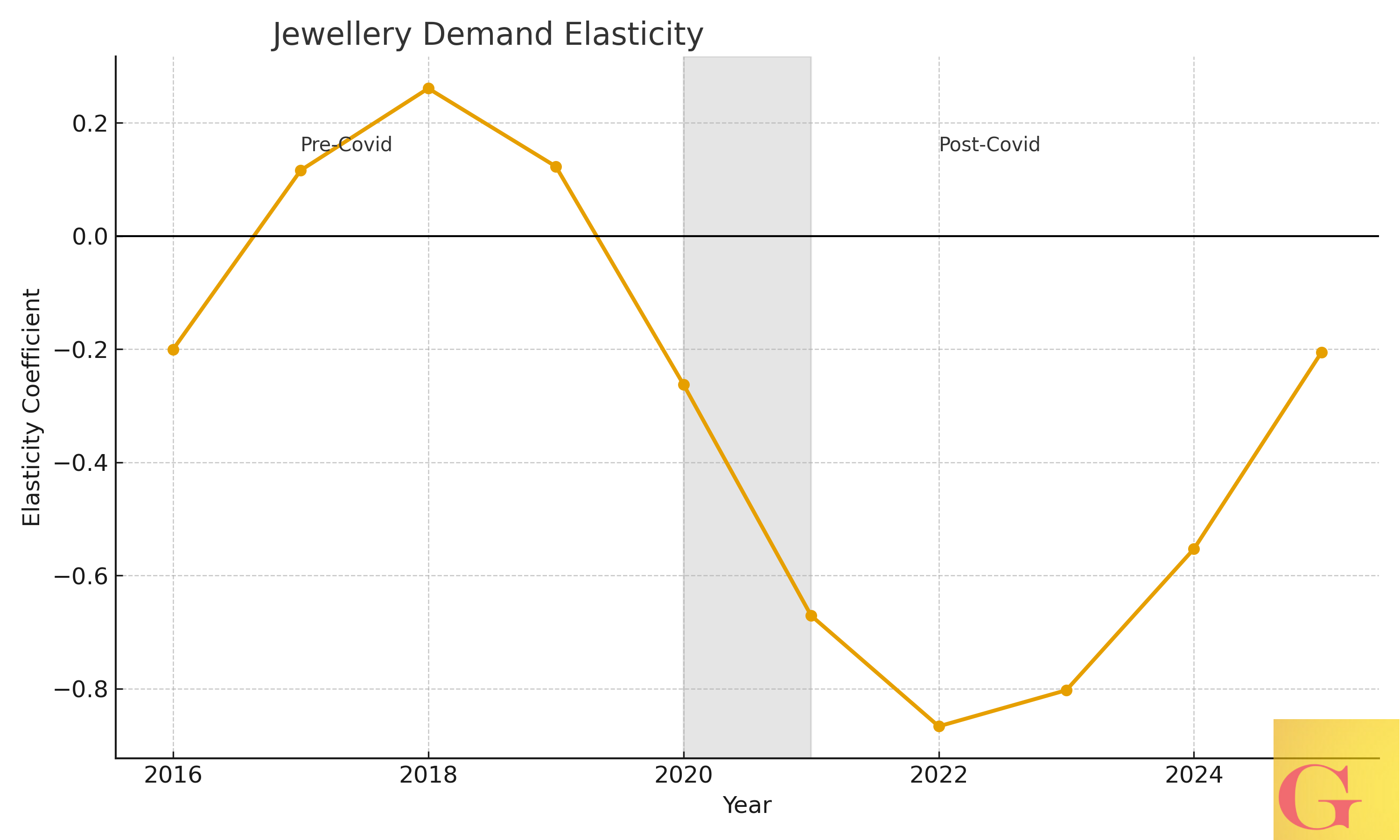

II. Jewellery Demand: A Retail Anchor with Predictable Elasticity

Jewellery demand follows classical price sensitivity more closely than any other gold segment. The report identifies a structural break during the pandemic period, when time-varying elasticity shifted from roughly negative 0.2 pre-Covid to nearly negative 0.7 immediately afterward. As the price of gold rose through 2024 and into 2025, the elasticity estimate stabilized around negative 0.4. Based solely on elasticity, one would expect jewellery demand to fall by approximately twenty percent; SocGen reports an actual decline of twenty-three percent, which remains consistent with the model’s predictions.

Part 2: The Death of Synthetic Gold- (The Wet Blanket is Gone)

The Soc Gen elasticity report we covered yesterday mapped the behavioral shifts across jewellery buyers, bar and coin investors, central banks, and ETF participants, and it confirmed what Gold bugs have been watching for three years. The data shows a market moving away from a single demand pattern and toward a set of distinct behaviors that reflect a deeper transition in gold’s role. Soc Gen presents the sectoral story clearly but leaves the structural implications unstated, and that is where this analysis begins.

Consumers continue to respond to higher prices by reducing discretionary jewellery spending or substituting for non-gold alternatives, a behavior that reinforces jewellery’s role as a retail, sentiment-sensitive category. While volumes remain significant, the potential demand destruction is smaller compared with the anticipated flows from investment-driven channels and central banks.

“Price remains the single most variable component of jewellery demand.”

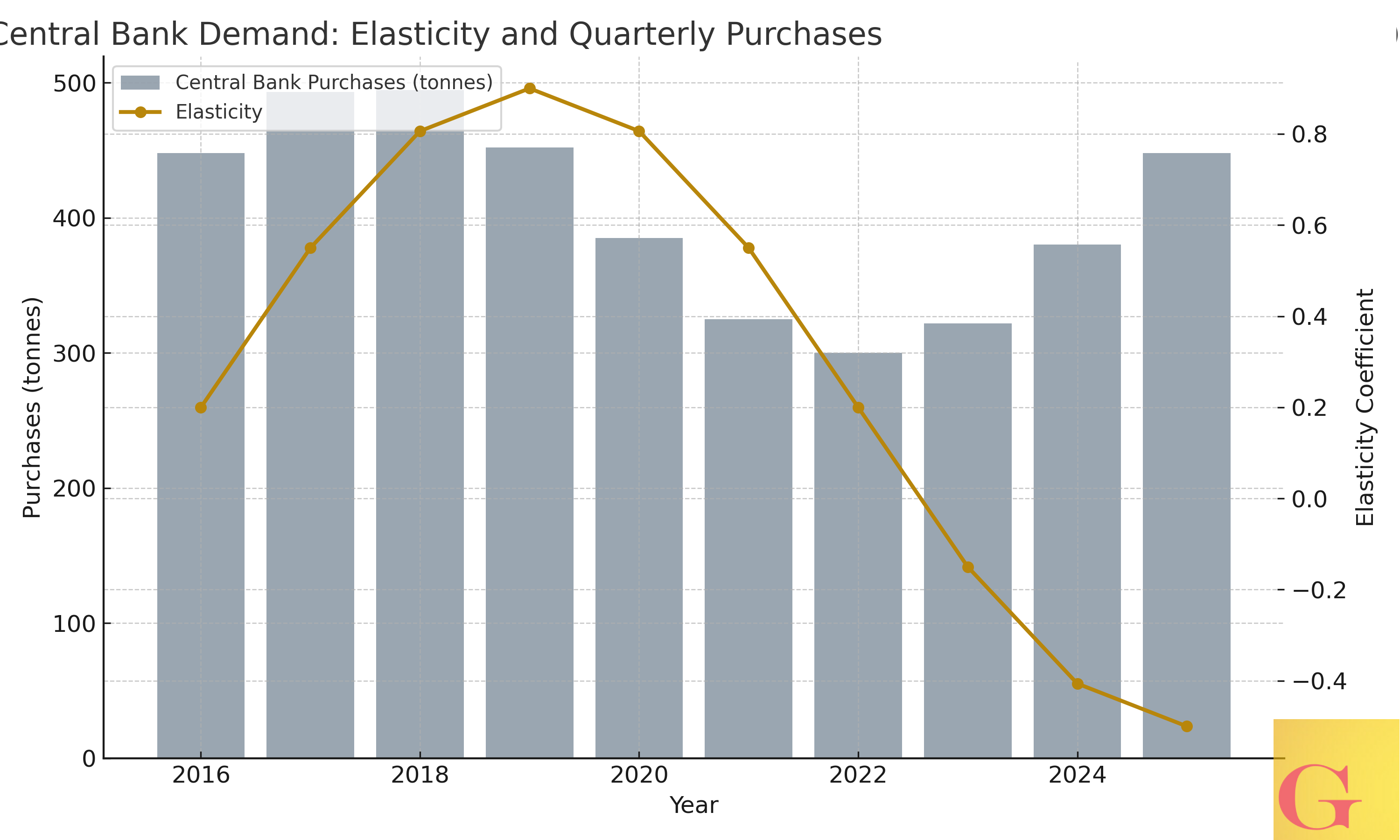

III. Central Banks: Strategic Buyers with Mixed Elasticity Signals

Central bank accumulation reflects strategic reserve objectives. Prior to the pandemic, central bank demand displayed slightly positive elasticity, indicating steady buying regardless of price moves. During the Covid period, elasticity fell sharply, yet by 2023–2025 the estimate had returned to a positive territory near 0.9. The implication is that a one percent increase in the gold price is associated with a comparable increase in central bank purchases, at least in the short term.

DB: Sovereigns Print Fiat to Buy Gold Now

Deutsche Bank’s renewed focus on “inelastic demand” signals a deeper change in the gold market. Sovereigns now plan in ounces, not money, and their accumulation has become strategic, persistent, and price insensitive. The dynamic points to a rising floor for gold and further towards a quiet return to monetary gold across the globe.

SocGen emphasizes that traditional demand modelling techniques offer limited explanatory power for central bank flows. Decisions are motivated by reserve diversification, geopolitical hedging, liquidity preference, and long-term macro considerations. These factors dominate price sensitivity and reduce the usefulness of elasticity as a predictive tool.

“Central bank buying is influenced by strategic factors rather than purely economic ones.”

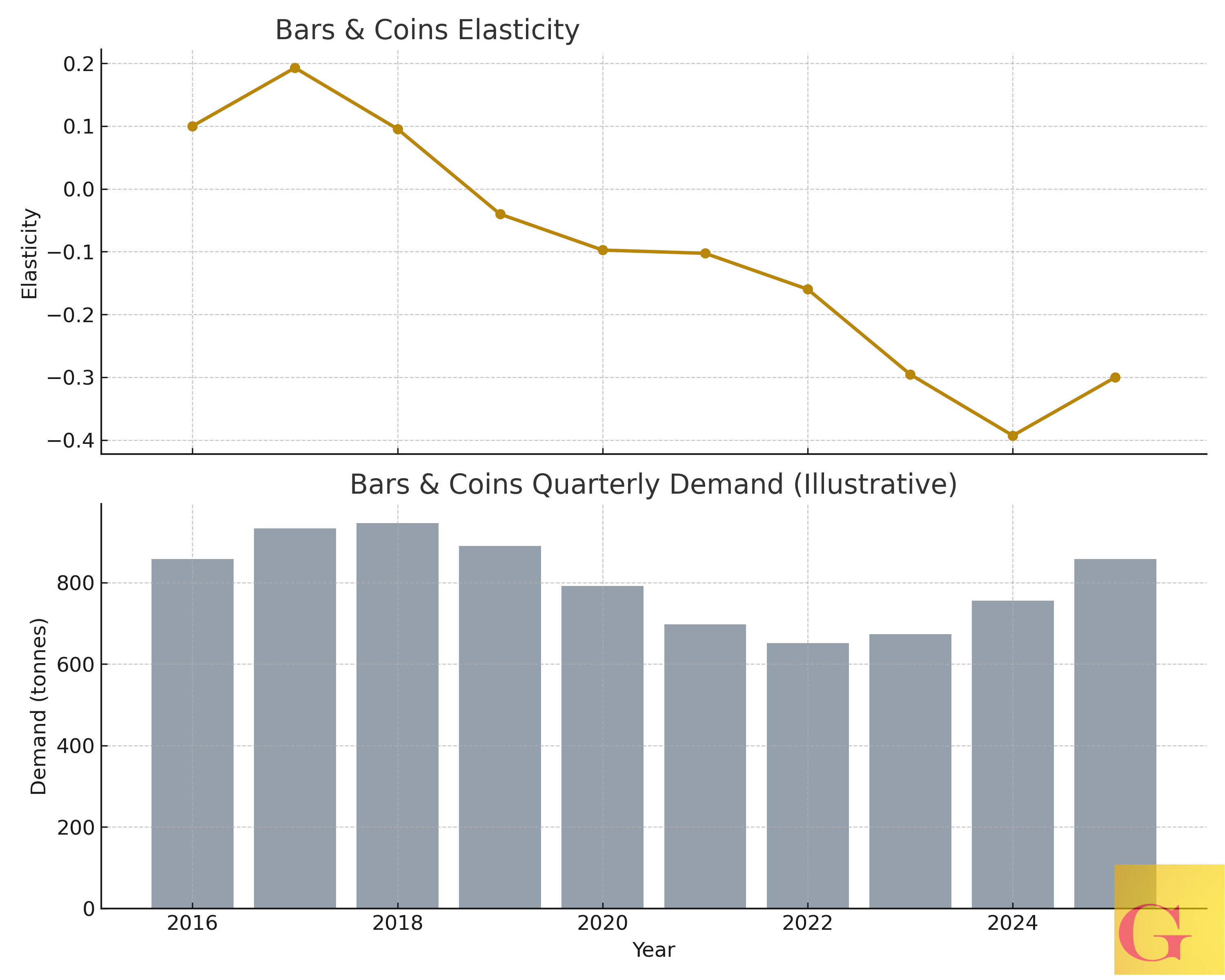

IV. Bars and Coins: Investor Behavior and Positive Elasticity

Bars and coins display behavior characteristic of investment-driven demand. As of late 2025, the elasticity estimate sits near 0.4, meaning investors increase purchases as prices rise. SocGen attributes this to momentum-driven psychology, with buyers attempting to maintain exposure during rally conditions and avoid missing further upside.

The segment’s elasticity normalized in 2023–2024 after the distortions of the pandemic, returning to levels similar to those observed before 2020. Bars and coins therefore act as an amplifier when prices rise and serve as an accessible entry point for retail investors seeking gold exposure when macro uncertainty increases.

V. ETFs: Mixed Elasticities and Regional Divergence

ETF flows remain the most complex and fragmented demand category. Globally, the elasticity of ETFs is close to zero in 2025, a pattern that resembles the pre-Covid era. However, the global figure masks substantial regional variation.

Europe and North America retain elasticizes that can meaningfully influence the price formation process, whereas China and India show almost no price responsiveness. These two Asian markets account for only eight percent of global ETF tonnage, limiting their capacity to affect global prices.