UBS Has a 3 Pillared Thesis on Gold Miners

UBS Has a 3 Pillared Thesis on Gold Miners

The thesis rests on three reinforcing pillars: sustained gold demand, materially improved corporate fundamentals, and contained production costs.

-UBS

Authored by GoldFix

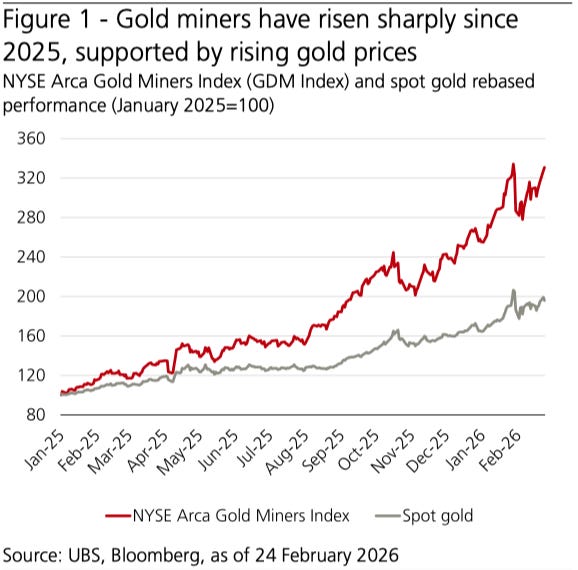

UBS (less specifically but equally bullish compared to the JPM outlook yesterday) sees gold mining equities are rebounding alongside strengthening bullion fundamentals, with gold projected toward $5,900/oz on sustained central bank demand, ETF inflows, and easing real rates. UBS has a 3-pronged thesis on why it should continue for 2026. Improved margins, falling leverage, and tighter capital discipline support valuations. Includes a list of miners meeting their criteria for this continued run.

Gold Mining Equities: Tactical Re-Engagement Within a Structural Bull Cycle

The constructive outlook begins with bullion itself.

“We continue to rate gold as Attractive and remain ‘long’ the metal within our global asset allocation.”

The expectation is for gold to trade around USD 5,900 per ounce by year-end. The support structure cited includes continued central bank demand, ongoing ETF inflows, declining real US interest rates, and persistent geopolitical risk. The authors characterize gold as being in the mid-to-late phase of its current bull market, a stage typically marked by new highs interspersed with mid- to high single-digit pullbacks.

Crucially, they argue that the macro conditions historically associated with the end of gold bull markets have not materialized.

“The conditions that have historically marked the end of gold bull markets—persistently elevated real interest rates, a structurally stronger US dollar, an improved geopolitical backdrop, and fully restored central bank credibility—have yet to materialize.”

With two additional Federal Reserve rate cuts expected this year, policy is viewed as remaining supportive. Real rate compression continues to serve as a tailwind rather than a headwind.

Demand data reinforces the positioning. World Gold Council figures indicate that total gold demand exceeded 5,000 metric tons for the first time in 2025. Investment flows and central bank accumulation remain core pillars of demand. The authors have revised their 2026 demand forecasts higher, citing expectations for stronger ETF inflows and resilient physical demand across bars, coins, and jewelry.

On the supply side, stagnation persists. Wood Mackenzie estimates that approximately 80 mines will exhaust their current production plans by 2028. This forward depletion dynamic introduces medium-term supply constraints that underpin price stability.

Within diversified portfolios, gold is framed as a strategic hedge rather than a momentum instrument. Allocations in the mid-single-digit range are described as appropriate for investors with structural affinity for the asset class.

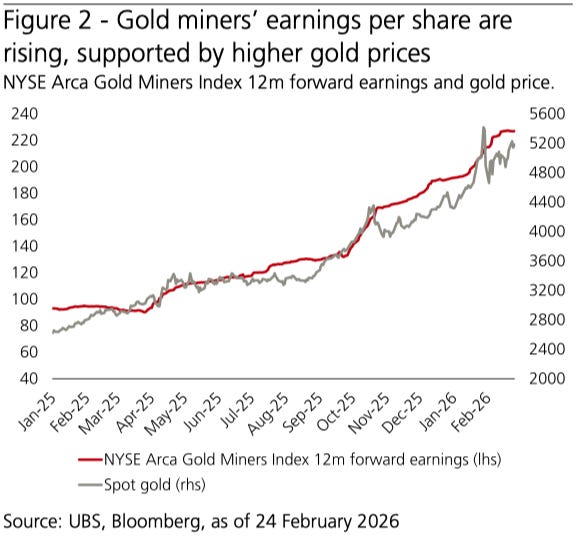

Improved Corporate Fundamentals and Capital Discipline

The second driver centers on corporate evolution within the mining sector.

Historically, mining equities frequently underperformed bullion. Operational inefficiencies, aggressive leverage, and value-destructive acquisitions undermined shareholder returns. The authors argue that the sector’s profile has shifted materially.

“Margins have improved substantially in recent months, their ability to generate cash has increased, and financial leverage has been falling.”

Rising bullion prices have expanded margins, while production cost growth has remained comparatively contained. Cash flow generation has strengthened. Balance sheets have improved, with the sector projected to move toward an aggregate net cash position by year-end.

Capital expenditure plans remain measured. Management compensation structures across leading producers appear aligned with shareholder return metrics, discouraging excessive M&A and promoting capital discipline. The structural shift in governance is presented as a differentiating factor relative to prior cycles.

Chart: The Buying Gets More Impatient pic.twitter.com/encEkLTULA

— VBL’s Ghost (@Sorenthek) February 27, 2026

Earnings expansion supports this transformation.

Continues here