Continues here Founders can preview the whole manuscript

The Return of Real Money

Introduction to “As Good As Gold"

Authored by Vince Lanci of GoldFix

Intro: The Hidden Architecture of Money

The modern financial system runs on an assumption that few people ever pause to examine. Governments around the world hold trillions of dollars in U.S. Treasury securities. Central banks accumulate them as reserves. Banks borrow against them in repo markets. Derivatives contracts are margined with them. Institutional portfolios treat them as the safest asset in global finance.

These securities are not simply investments. They are the foundation of the system. Yet a simple question rarely gets asked:

Why do these assets hold the global financial system together?

Most explanations of the international monetary system focus on currencies. Analysts debate the strength of the dollar, the rise of the euro, or the long-term ambitions of the Chinese yuan. Policymakers discuss interest rates, trade balances, and exchange rate regimes. These discussions are important, but they often miss something more fundamental.

The international monetary system is not built primarily on currencies.

It is built on collateral.

Collateral is the asset that supports financial trust. It is what banks pledge when they borrow, what institutions use to secure derivatives contracts, and what central banks accumulate to defend their currencies during moments of crisis.

Without reliable collateral, credit cannot expand and financial markets cannot function.

Seen from this perspective, the global monetary system becomes easier to understand. It is not simply a network of currencies competing for dominance. It is a hierarchy of assets that supports the balance sheets of governments, financial institutions, and markets.

Those assets change over time. And when they change, monetary systems change with them.

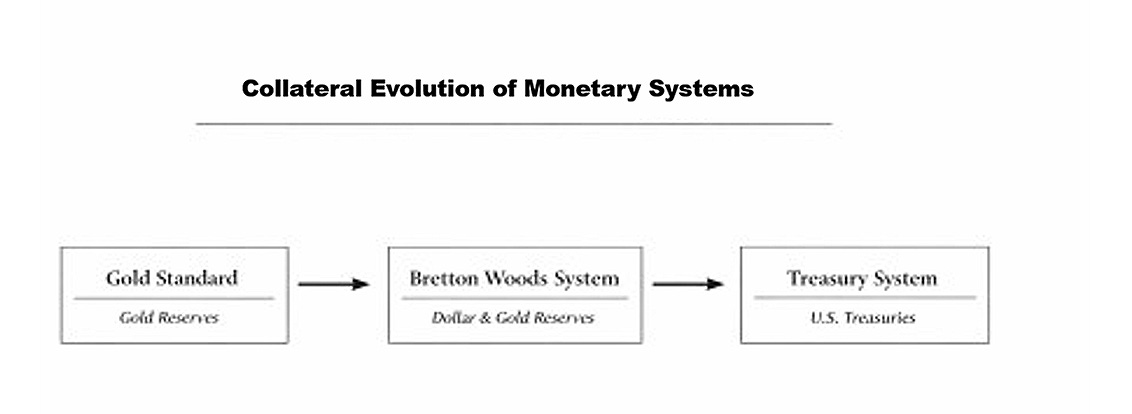

For much of the nineteenth and early twentieth centuries, gold served as the foundation of international finance. Governments held gold reserves because the metal possessed characteristics that allowed it to function as neutral collateral across borders. Gold had no issuer, carried no counterparty risk, and was widely trusted as a store of value.

After the Second World War, the Bretton Woods system introduced a hybrid structure. The U.S. dollar became the primary currency used in global trade, while gold remained the ultimate settlement asset between central banks.

When the United States suspended gold convertibility in 1971, the system did not abandon the need for collateral. Instead, financial markets adapted. Over time, U.S. Treasury securities gradually assumed the role that gold had previously played within the architecture of global finance.

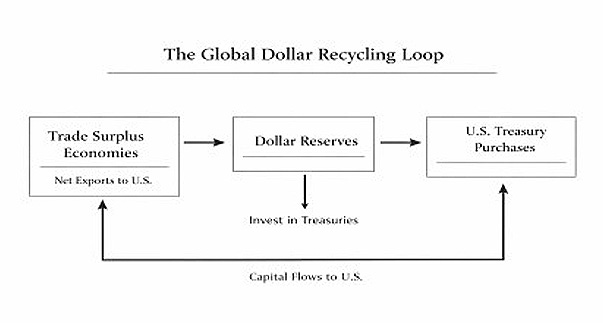

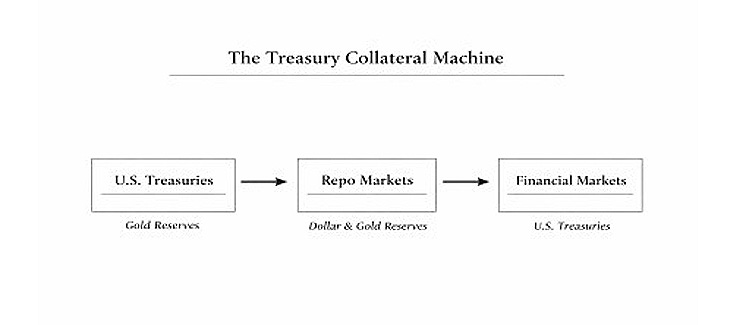

Treasuries offered liquidity, legal certainty, and a large supply of safe assets capable of supporting rapidly expanding financial markets. Repo markets grew around them. Derivatives markets used them as margin. Central banks accumulated them as reserves. Global trade flows recycled dollars into Treasury markets, reinforcing demand for the asset that anchored the system.

By the early twenty-first century, the international monetary system had evolved into something rarely described explicitly.

It had become a Treasury-collateral system.

This structure explains several features of modern finance that might otherwise appear unrelated. It shows why safe assets are so important to financial stability, why fiscal deficits influence global liquidity, and why trade imbalances often return to U.S. financial markets.

It also explains why certain geopolitical events can reverberate through the global financial system.

When governments begin to question the safety of their reserve assets, they are not simply adjusting their portfolios. They are reconsidering the foundations of the system itself.

Monetary systems rarely collapse suddenly. They evolve gradually as the assets supporting financial trust begin to change. Gold once served as the foundation of international monetary order. Treasury securities eventually replaced it as the dominant collateral asset of modern finance.

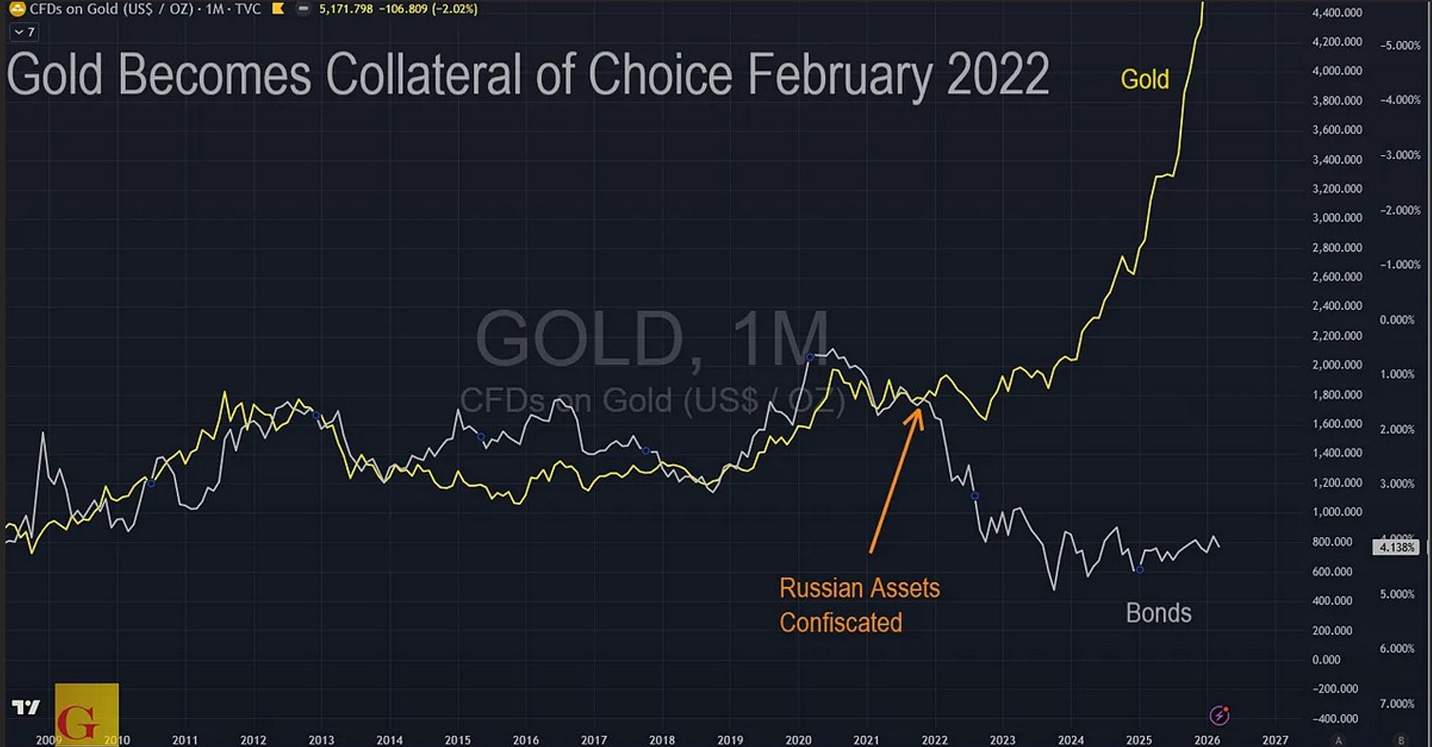

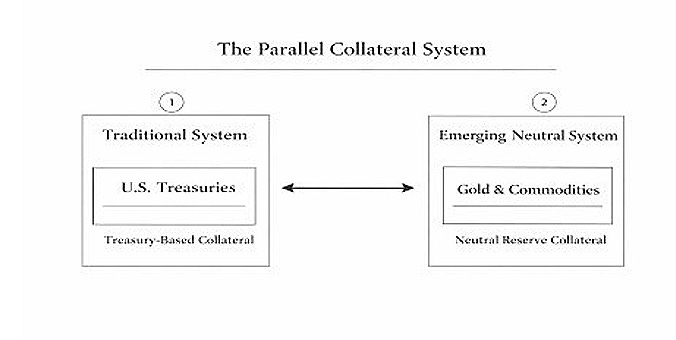

Today, the global economy continues to operate on Treasury collateral. Yet new pressures are beginning to appear. Financial markets demand ever-greater quantities of truly safe collateral. Governments are reconsidering how they structure their reserves. Geopolitical tensions are raising questions about the neutrality of financial infrastructure pursuant to the confiscation of Russian assets in 2022

These developments do not necessarily signal the end of the existing system. But they do suggest that the architecture of global finance may be entering a period of transition.

Understanding that transition requires looking beneath currencies and examining the assets that support financial trust. This book explores that hidden structure. It traces the evolution of the global monetary system from gold-based settlement to the Treasury-centered financial order that dominates modern markets. It examines the mechanisms that sustain this system today, including repo markets, reserve management, and the recycling of global trade flows into U.S. financial markets.

Finally, it considers how changes in collateral preferences could shape the next stage of the international monetary order.

Currencies may dominate the headlines.

But the true architecture of the monetary system lies deeper.

It lies in the assets that the world trusts as collateral.

//////////End Introduction//////////////

Table of Contents

Part I — The Foundations of Monetary Trust

-

Chapter 1 — The Architecture of Trust

-

Chapter 2 — Gold as Global Collateral

-

Chapter 3 — The Dollar System Emerges

Part II — The Treasury Collateral System

-

Chapter 4 — After Gold

-

Chapter 5 — Treasuries as Global Collateral

-

Chapter 6 — The Collateral Pyramid

-

Chapter 7 — Global Dollar Recycling

Part III — Stress in the System

-

Chapter 8 — The Limits of the Treasury System

-

Chapter 9 — The Weaponization of Reserves

-

Chapter 10 — The Search for Neutral Collateral

Part IV — The Emerging Monetary Order

-

Chapter 11 — A Parallel Collateral System

-

Chapter 12 — The Next Monetary Order

Free Posts To Your Mailbox

Contributor posts published on Zero Hedge do not necessarily represent the views and opinions of Zero Hedge, and are not selected, edited or screened by Zero Hedge editors.

Loading...