The AI Ouroboros

The Week In AI

While markets argue about rates, geopolitics, and whether the Fed is “done,” the real story is happening elsewhere — quietly, relentlessly, and with very little regard for old rules.

Welcome to our new series "The Week in AI", where this week examines how capital concentration accelerates, valuations detach from reality, and Big Tech starts investing in all sides of the same trade.

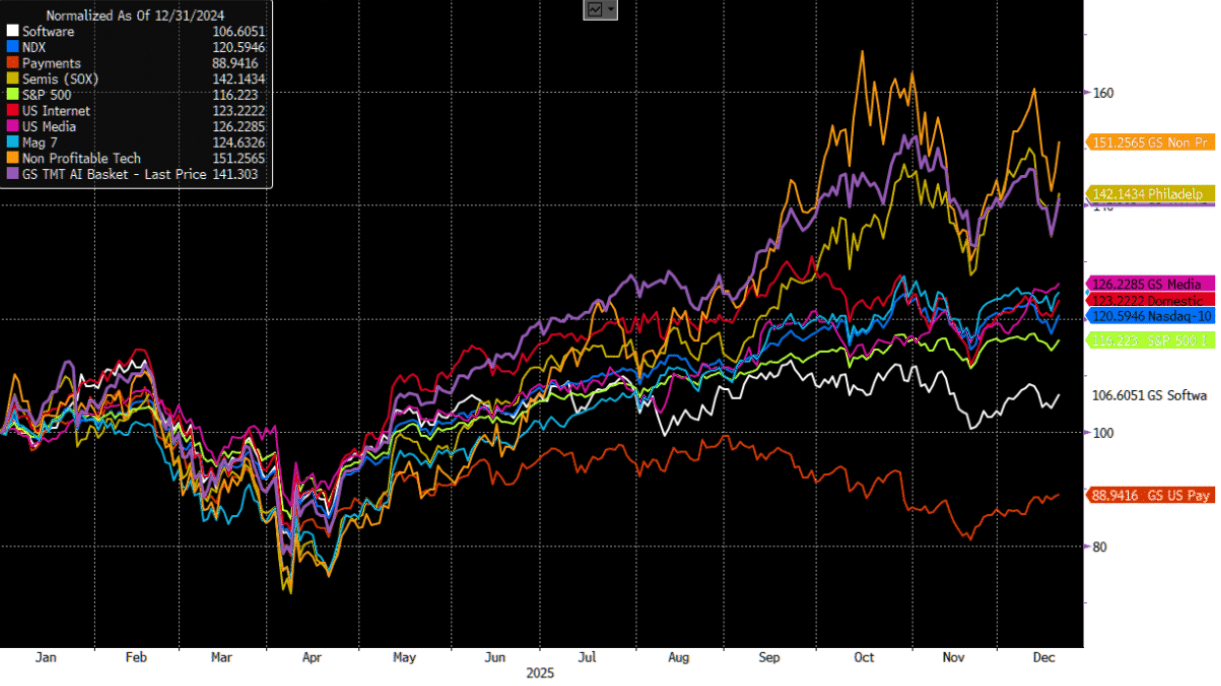

The scoreboard

Before we look at the news-flow, here is the 2025 end of year scoreboard in TMT, where of course semis and AI stocks are set to finish the year up 40%+. This can be compared to software +6% and payments down ~10%. Now, over to some news stories.

Source: GS

Amazon wants in on OpenAI. Again. And everywhere else

Amazon is reportedly in talks to invest $10 billion into OpenAI — a company already effectively married to Microsoft.

If that sounds odd, it shouldn’t. Amazon is also a major investor in Anthropic. Microsoft, meanwhile, has exposure to both as well.

This isn’t competition anymore. It’s AI cross-ownership.

Big Tech isn’t trying to pick winners — it’s buying optional control over the entire landscape. If one model dominates, they win. If another does, they still win. If regulation shows up, they’re already inside the room.

This is what late-stage platform capture looks like.

Three years, billions spent — and Amazon still isn’t Top 10

Amazon also quietly reorganized its AI division and changed leadership this week. Translation: things aren’t working fast enough.

Here’s the uncomfortable part:

Microsoft and Amazon have spent three years and tens of billions trying to crack the AI leaderboards.

They still can’t.

Meanwhile, Xiaomi — yes, that Xiaomi — made it into the top 10 this week.

This is what terrifies incumbents:

AI advantage is not proportional to cloud spend, headcount, or legacy dominance.

Which is exactly why they’re buying everyone.

Databricks raises $4bn at $134bn — welcome to series “L”

Databricks is raising $4 billion at a $134 billion valuation. Not an IPO. Not public markets. Not price discovery. A Series L. That’s not a typo. That’s the alphabet running out of letters.

Remember IPOs? Neither does this market. This isn’t late-stage venture — it’s capital with no exit pretending time doesn’t exist. Capital is no longer about funding growth — it’s about maintaining narrative dominance until someone else blinks.

OpenAI hires Shopify’s product chief — commerce is the next battleground

OpenAI hired a senior product executive from Shopify.

This is not about chat. This is not about answers. This is about agents that transact. AI that doesn’t just recommend — but buys, sells, negotiates, and executes.

Agentic commerce isn’t coming. It’s already being staffed. The endgame isn’t search. It’s intermediation. And whoever controls that layer doesn’t just take a cut — they rewrite how markets function.

If AI becomes the buyer, the seller, and the recommender, price discovery itself becomes "optional.”

UPS buys robots (no, not humanoids) — reality is less sexy and more profitable

UPS is buying hundreds of AI-powered robotic arms to unload trucks.

Not humanoids.

Not demos.

Not sci-fi.

Just steel, sensors, and machine vision — from a startup called Pickle Robotics (which might be the most honest name in AI).

This is the part retail investors don’t see:

AI adoption isn’t flashy. It’s industrial, boring, and immediately ROI-positive.

And it’s happening faster than anyone wants to admit.

Meta abandons the Metaverse (again) and doubles down on AI

Meta is quietly shifting budget away from Reality Labs and into AI, even pausing parts of its third-party headset strategy.

Translation:

The metaverse didn’t die — it just failed to monetize.

AI, on the other hand, is eating everything:

Capex.

Talent.

Strategic attention.

Meta isn’t pivoting because AI is trendy.

It’s pivoting because AI is the only thing left that might justify its cost structure.

The bigger picture: AI isn’t a sector — it’s a gravity well

Step back and the pattern is obvious:

1. Big Tech is investing in all major AI players

2. Private valuations are untethered from exits

3. Commerce, logistics, and labor are being quietly automated

4. Legacy moonshots are being defunded

5. Capital is clustering, not diversifying

This isn’t a bubble yet. It’s something stranger.

An AI ouroboros — where Big Tech eats its own, capital eats the future, and everyone pretends this is normal because there’s nowhere else to go.

The question isn’t who wins AI. The question is:

What happens when everyone owns everyone, valuations don’t clear, and the real economy gets automated faster than labor can adapt?

That’s not a tech story anymore.

That’s a macro one.