The Attack on Europe

Under attack

We have been bullish Europe for quite some time now as a "it can only get less worse" trade. The problem with being long Europe is that when "she" disappoints it is most often violently and with a bang. Europe has clearly been under attack this week and SX5E approached the huge trendline very fast. 5800/5750 is the short term must hold area (futures). Let's have a look at the latest in Europe and why we are nervous.

Source: LSEG Workspace

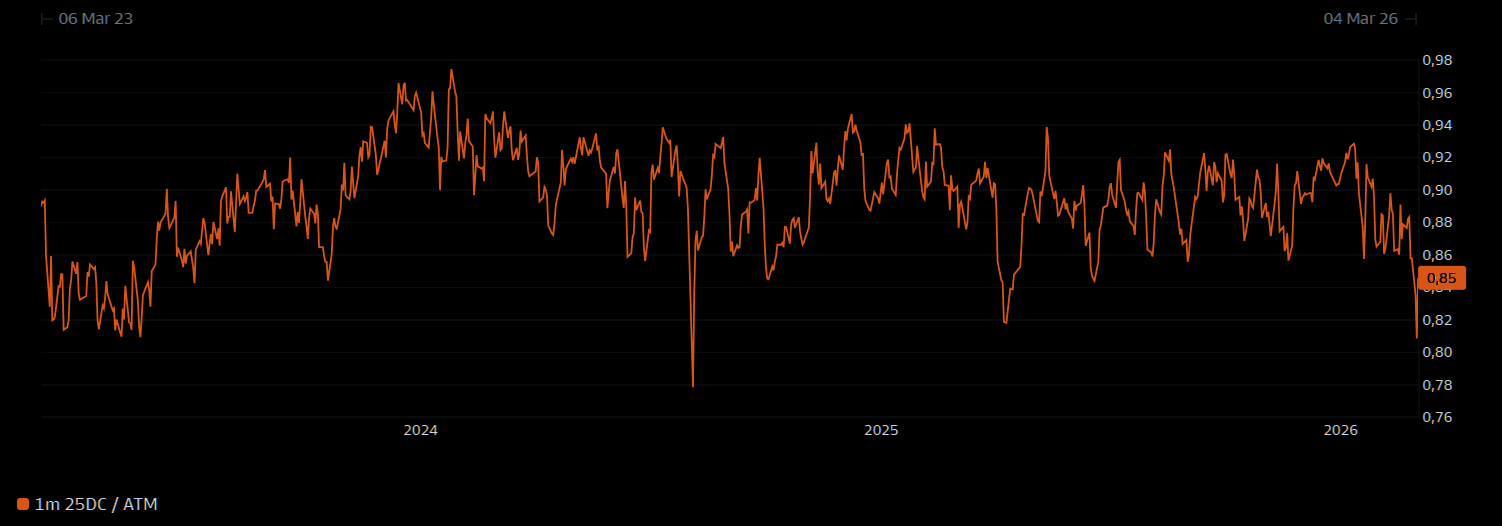

European fading enthusiasm

Investors are paying less for upside options relative to downside protection. That’s not extreme, but it’s a clear cooling in bullish positioning. Investors are dialing back upside bets in European equities.

Source: Marquee

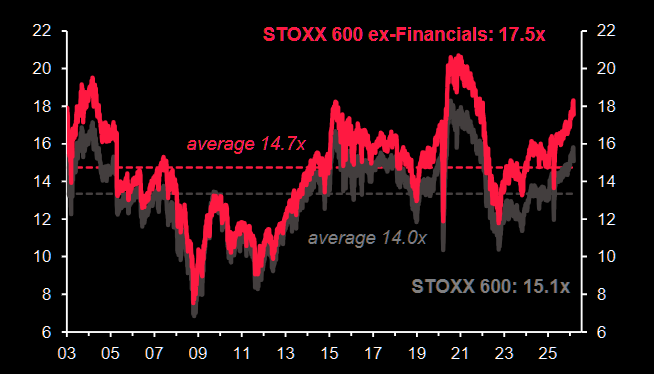

12m fwd European P/E remain elevated

European equities enter this crisis with richer valuations. The starting point matters and the STOXX 600 index was trading with a fwd P/E of 15.8x as of end February (18.5x excluding Financials), a level close to our bull-case scenario published in our 2026 outlook. Despite the last two days sell-off, the rise in bond yields is keeping the equity risk premium tight.

Source: Soc Gen

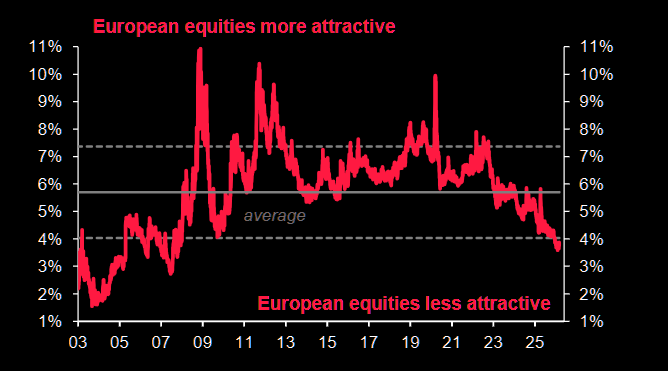

In "less attractive" territory

STOXX 600 forward Earnings yield minus German 10Y bond yields.

Source: Soc Gen

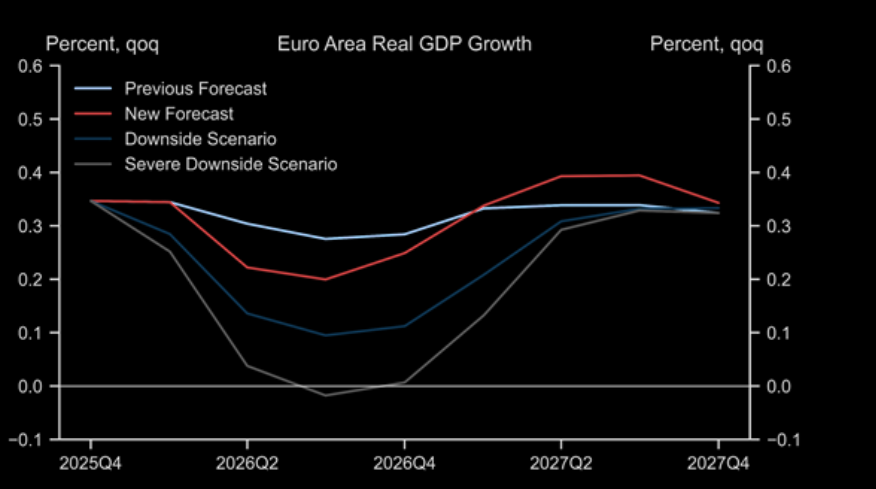

The hit from higher oil

Not massive but for sure not what a suffering Europe with hardly any growth needs...

Sven Stehn: "For the Euro area, we estimate that our new energy price forecasts will lower real GDP by 0.2% by end 2026 relative to our previous forecast, with modest downgrades to quarterly growth over Q2-Q4. In the downside scenario, GDP would be 0.7% lower, and growth would slow to +0.1%qoq. In the severe downside scenario, GDP would be 1.3% lower, and growth would slow to a halt over the next few quarters."

Source: Goldman

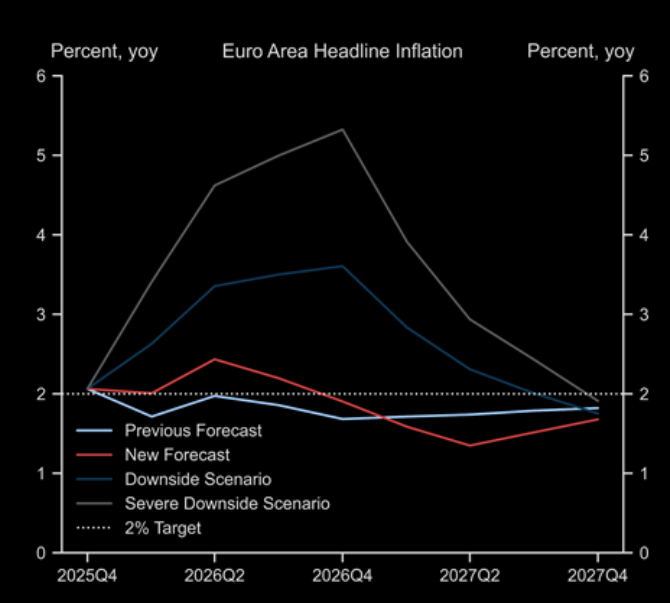

Implications for inflation

Higher energy prices will boost inflation for all countries.

Sven Stehn: "For the Euro area, we estimate that our new energy price forecasts will boost year-over-year headline inflation by 0.3pp over the next year. Headline inflation by 2026Q4 would be 1.9pp higher in the downside scenario and 3.6pp higher in the severe downside scenario."

Source: Goldman

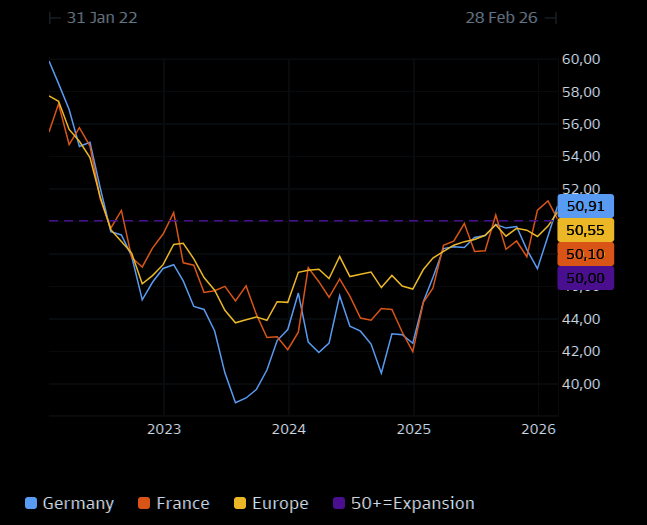

What about that economic momentum?

Europe has crawled out of a deep dark hole but PMIs at just around 50 is of course not very impressive.

Source: Marquee

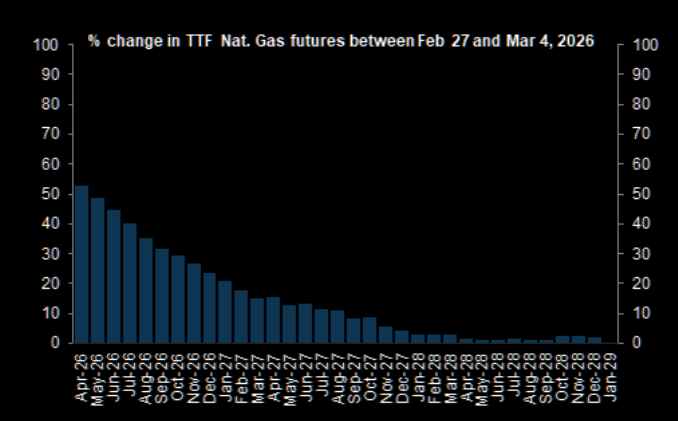

Bad, but not as bad as 2022

The current shock has been priced into the European natural gas curve as a more temporary disruption with limited moves in late 2027 and 2028 forwards. Instead, in 2022, the overall price move was larger and, even in the first few weeks, the Russian supply shock was reflected across the curve with large increases in 2023 and 2024 forwards as well.

Source: Datastream

Iran & the EURO

"The impact of the Iran war on EUR/USD boils down to one thing: energy. FX is tracking the combined moves in oil prices and natural gas prices tick-for-tick. The market reaction is reasonable and very similar to what happened during the closure of the Nordstream pipeline in June 2022. There is a negative supply shock under way which represents a direct tax on Europeans that has to be paid to foreign producers in dollars."