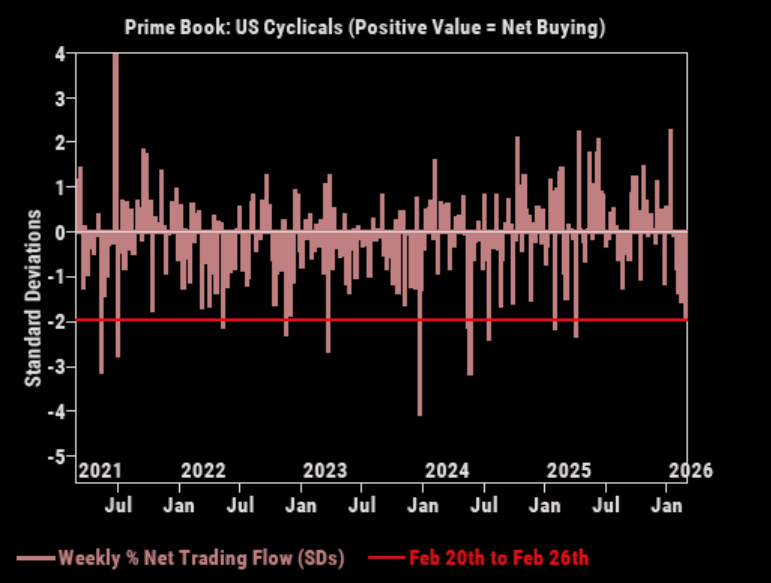

Cyclicals vs Defensives Had the Worst Week of the Year

All good things come to an end

Cyclicals have materially outperformed with blended industrials and materials having their best start in 20+ years. That changed last week. Cyclicals vs. Defensives were -3.4%, the worst week of the year.

GS trading desk: "A miss on ISM could cause pain for the cyclicals/industrials complex that has been heavily bought by the HF + LO community YTD. Given positioning, a cyclicals lower / secular winners & index higher move likely the biggest pain trade for the HF community."

Source: Bloomberg

All cyclical sectors sold

All US cyclical sectors, Energy/Materials/Industrials/Financials/Real Estate – were net sold last week and collectively saw the largest net selling since Liberation Day (-1.9 SDs 5-year), driven by long-and-short sales. US Cyclicals long/short ratio now stands at 1.79 (vs. YTD high of 1.89 seen in late January), in the 54th/45th percentiles vs. the past year/five years.

Source: GS Prime

Very high

US Capital Goods are trading on a very high multiple against the market.

Source: UBS

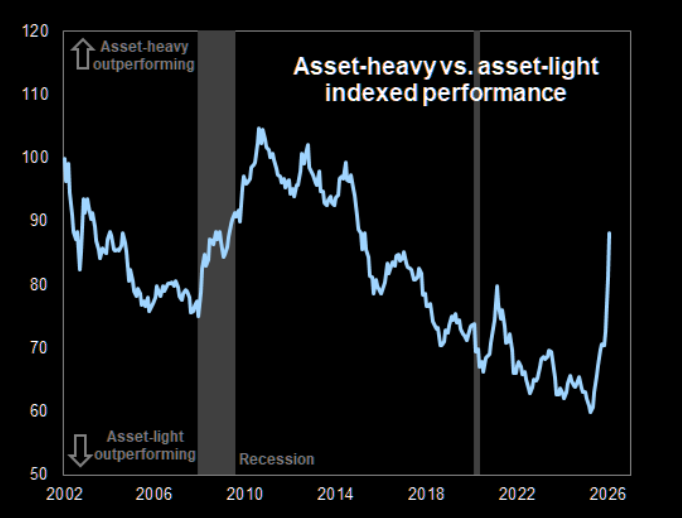

Asset heavy

Maybe the massive reversal in asset-light vs. asset-heavy stocks have gone a little too far.

Source: Goldman

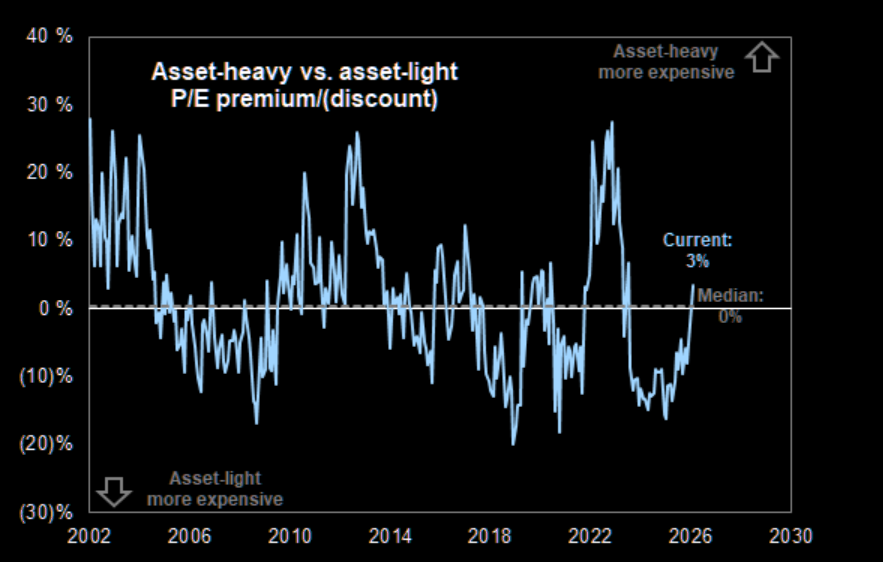

Now at a premium

Asset-heavy stocks now trade at a P/E premium to asset-light stocks.

Source: Goldman

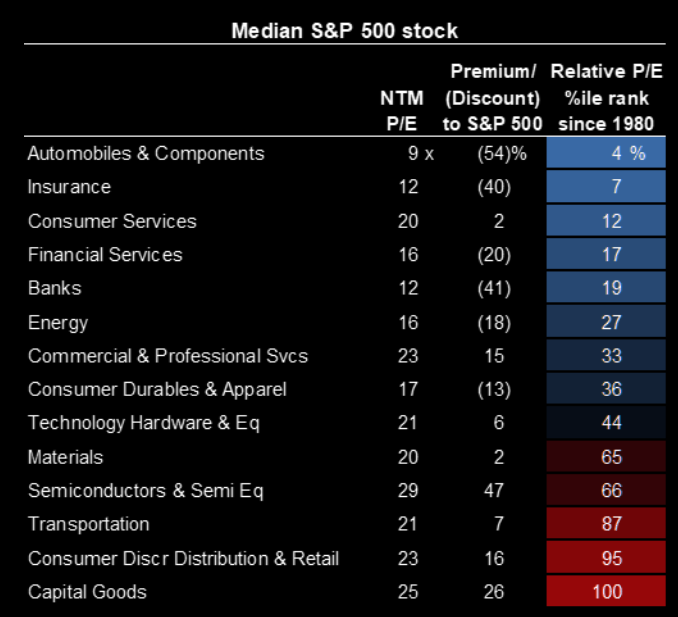

Some expensive - some cheap

Historical valuation of cyclical industry groups.

Source: FactSet

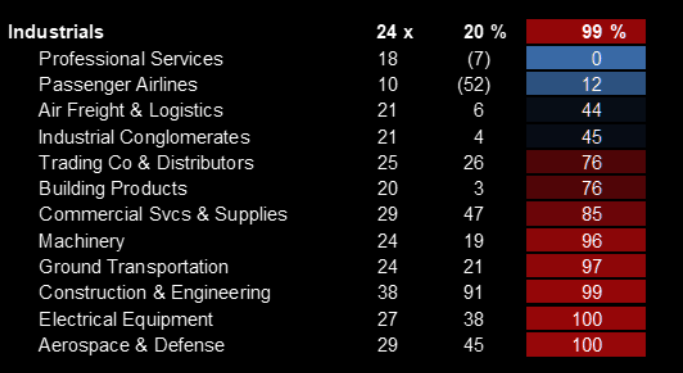

Industrial sub-sector valuation

Some of the industrial subsectors are outright expensive.

Source: FactSet

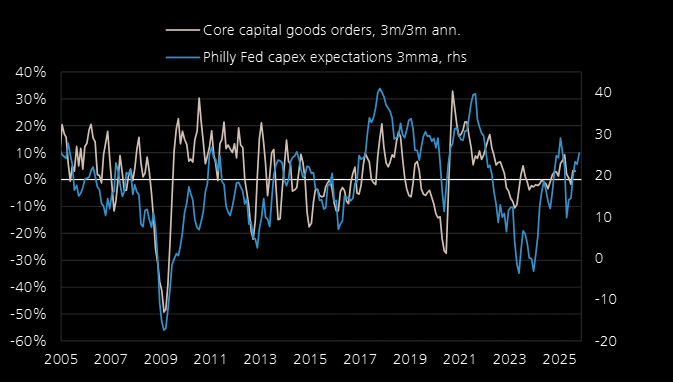

But the sector has the economic MoMo working for it

Capex pick-up

Philly Fed capital spending intentions would be consistent with a pick-up in capex.

Source: UBS

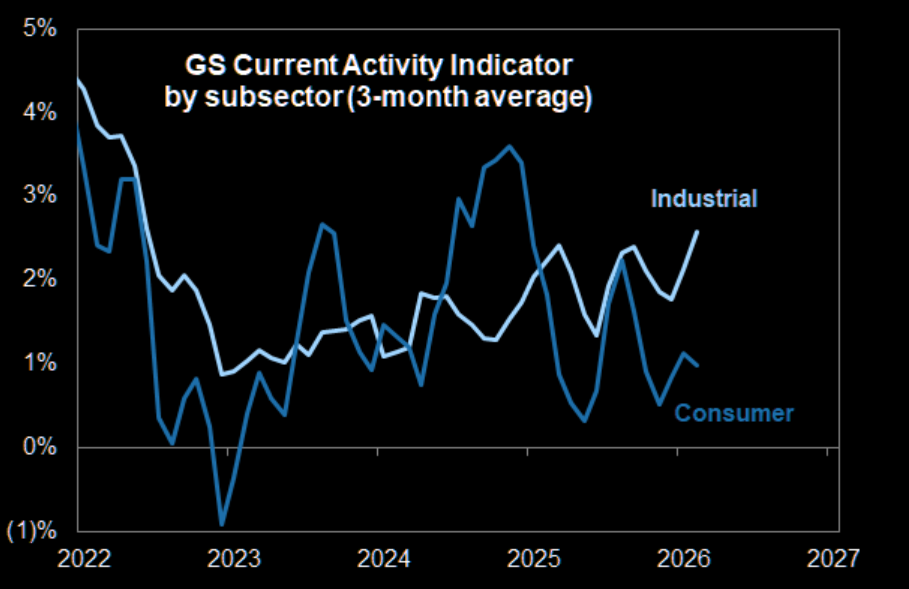

Improving

Industrial economic activity has improved in recent months.

Source: Goldman

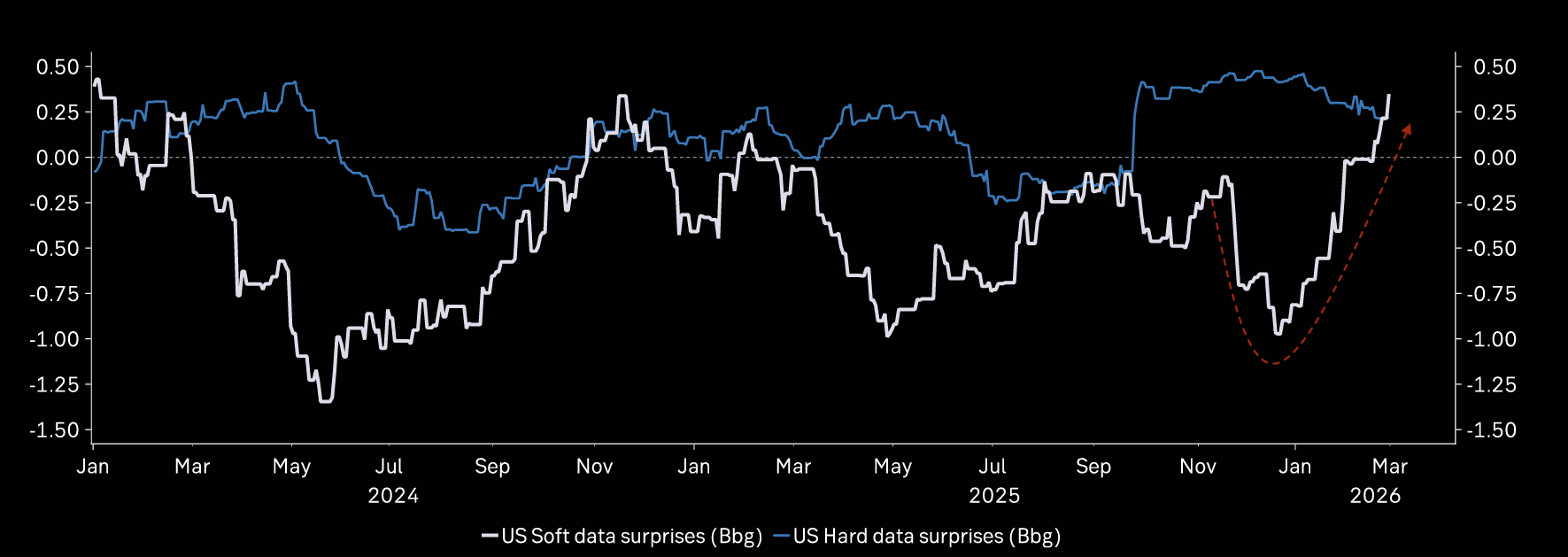

Gaining strength

US soft data surprises converge on hard data surprises in positive territory: positive signal.

Source: Macrobond

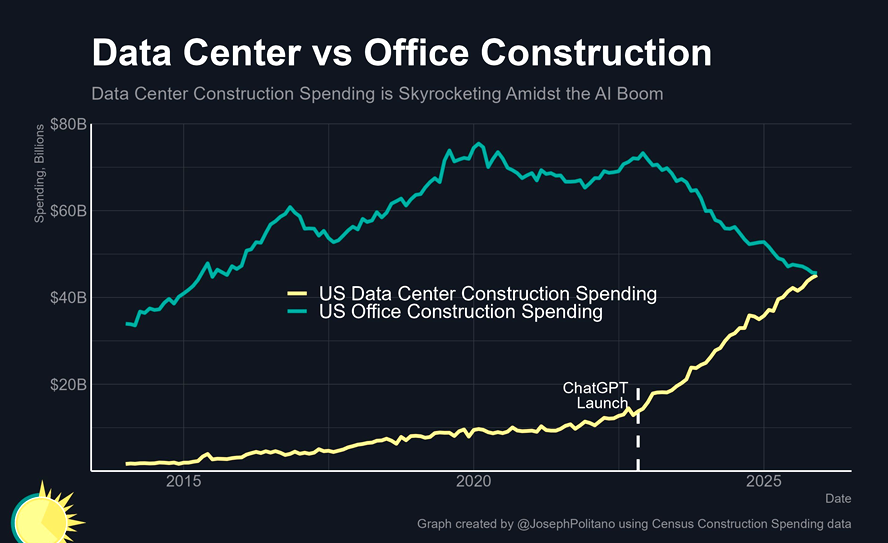

Construction spending

"The US now spends basically as much on data center construction as on office construction."