The Déjà Vu Breakdown

The Déjà vu breakdown

The setup we have been outlining for weeks continues to unfold almost step by step. Equities are breaking key technical levels, volatility remains elevated across assets, and positioning is shifting as systematic sellers press the tape. Yet much of the fast money has already adjusted positioning, creating an increasingly asymmetric setup. The question now is whether downside momentum accelerates further, or whether positioning has already adjusted enough to set the stage for the next move.

Playing out perfectly

SPX is now well below the 200-day and the range. The 21-day crossing the 200-day puts in the “light death cross”. 6400 (futures) is the level to watch, but downside momentum remains strong and we don’t like catching falling knives.

On a related note, Hartnett pointing out: "In a good market when the index falls below its 200-day moving average investors cover their shorts, but in a bad market that’s when they sell their longs."

Source: LSEG Workspace

Breakdown

NASDAQ’s light death cross (21/200-day MA) remains in place, along with the break below range lows earlier this week. Our déjà vu logic stays in play for now.

Source: LSEG Workspace

Oversold

SPX and NDX RSI are at the lowest levels since Liberation Day. As we all know, oversold conditions tend to stay oversold longer than many think possible. Technical damage is building quickly.

Source: LSEG Workspace

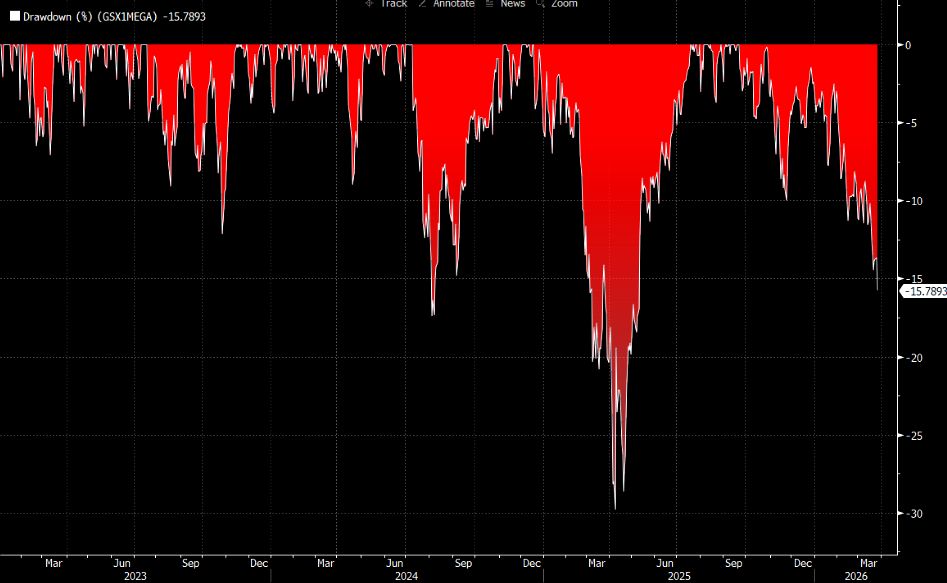

The MAG drawdown

Mag 7 is now down ~15% from the highs, approaching the scale of the Summer 2024 drawdown (per yesterday's close). More on MAGs here.

Source: Bloomberg/GS

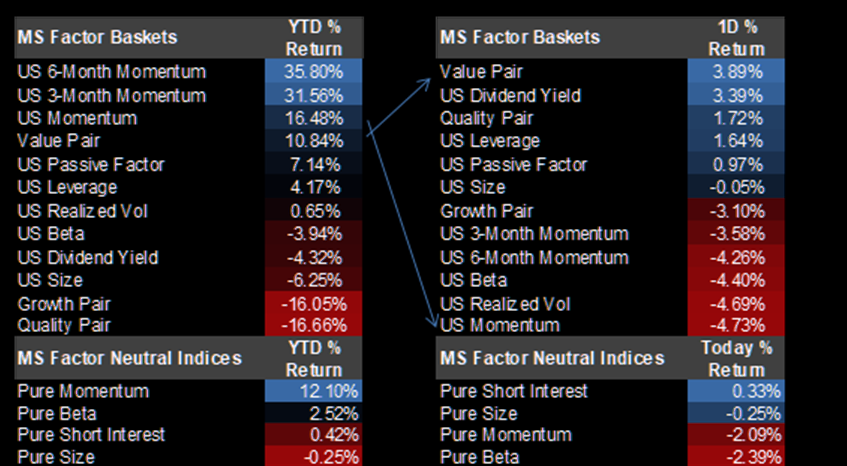

No active reduction in gross

Beneath the technical damage, flows are starting to shift. Morgan Stanley PB desk notes that yesterday we did see signs of long side conviction cracking as HFs unwound longs from some of the key crowded trades where capital has been stickier (Global Memory, Semis, AI Complex), while they also pressed shorts in size not only across ETFs but also single-names more broadly. Ultimately, there was NO active reduction in gross, as yesterday’s activity was driven by appetite to reduce directional risk. Splitting the flow by strategy, Equity L/S funds drove the selling by a wider margin as they sold longs and added to shorts, followed by Multi-Strat / Macro funds and Stat Arb / Quant funds, which ended as more modest net sellers.

Source: Morgan Stanley

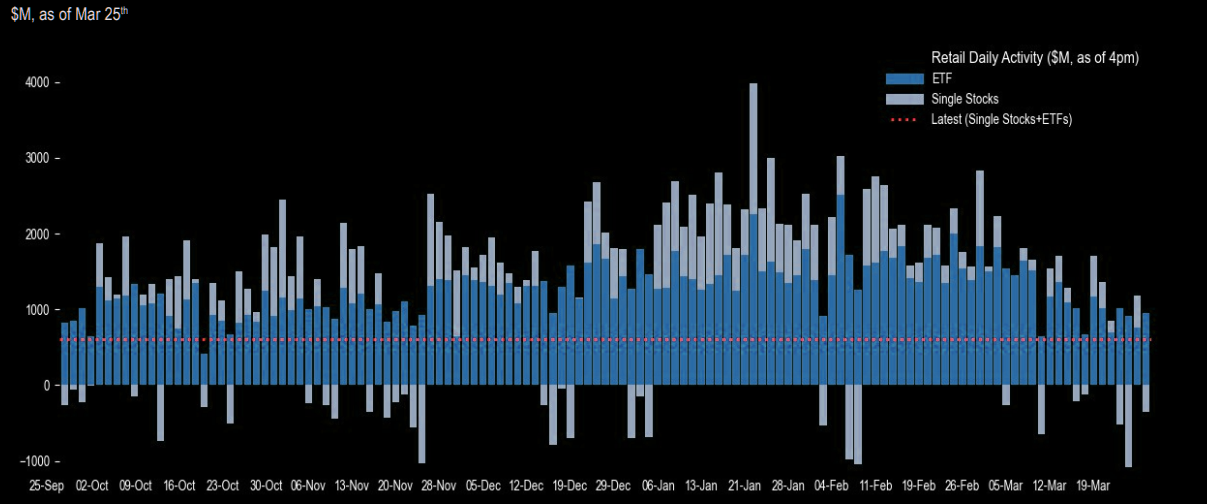

Retail retreating

Retail investors continued to scale back purchases, posting their slowest week in four months and now running about 70% below pre-conflict levels. More broadly, flows are starting to rotate more defensively across both ETFs and single stocks.

Source: JPM

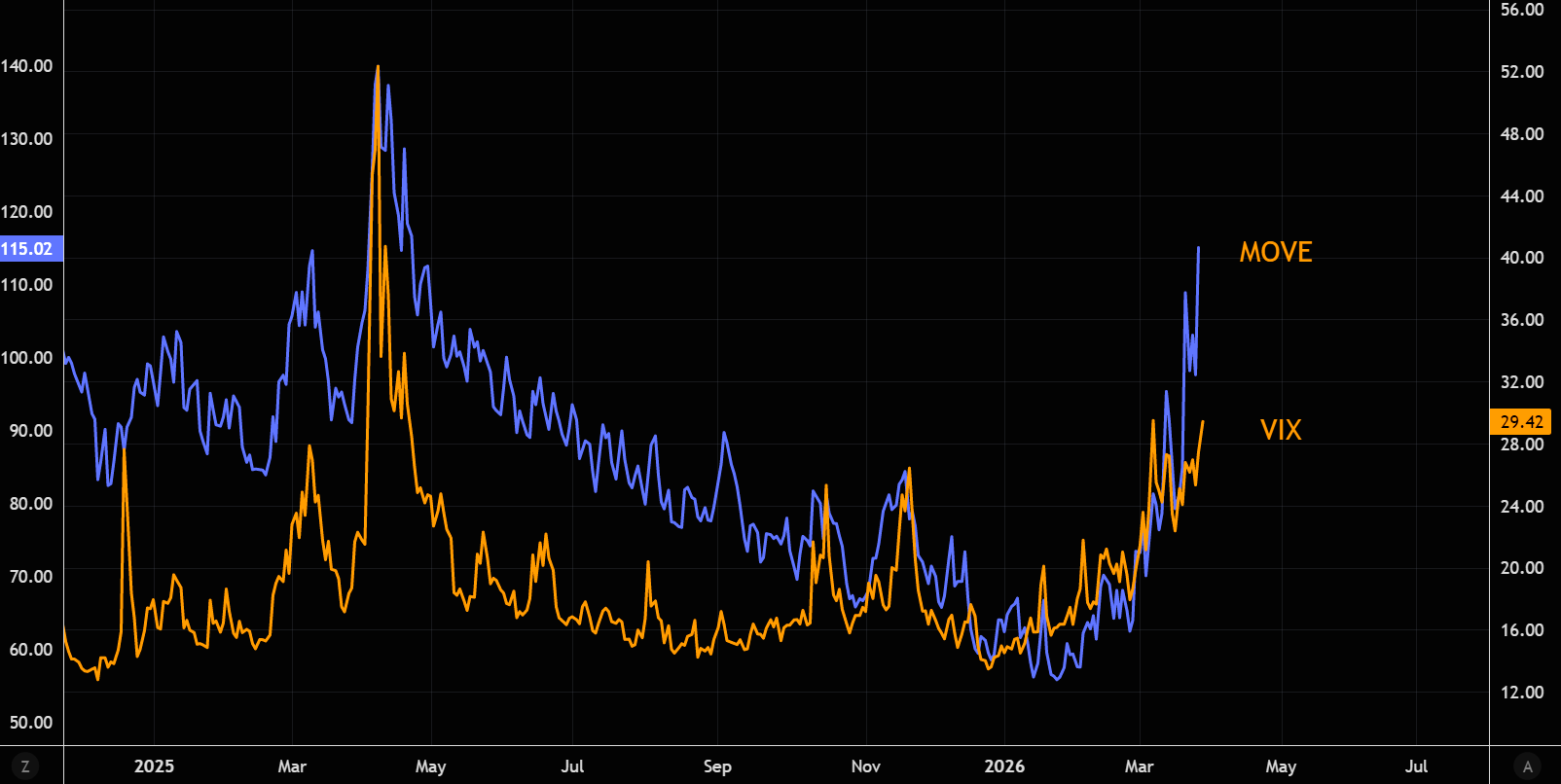

Bond vol unleashed

Believe it or not, MOVE isn’t far from the Liberation Day panic highs. Meanwhile the gap versus VIX has widened further over the past few sessions, a reminder that the real stress in markets is increasingly coming from rates, a dynamic that has historically forced equity positioning to adjust with a lag. Latest note on volatility here.

Source: LSEG Workspace

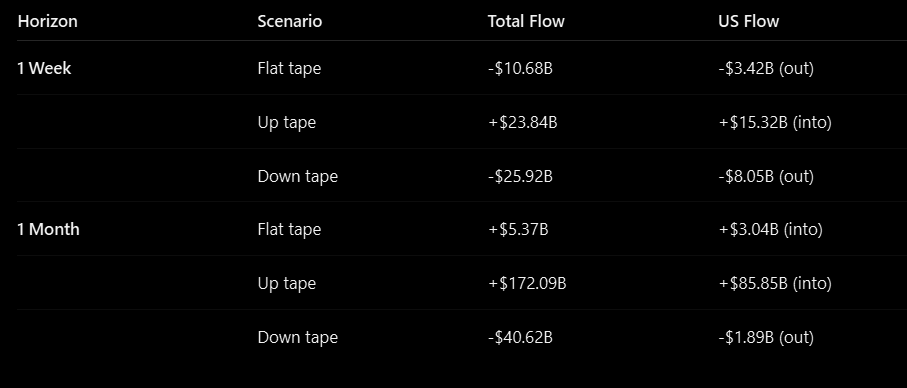

The long went short

Positioning is now starting to shift.

CTAs have sold nearly $55bn in US equities since the start of the month, leaving them short ~$18bn. With liquidity still poor, that pressure has been clearly visible in price action.

The good news, according to GS flow guru team, it’s largely behind us (absent a major macro shock), and the asymmetry now leans to the upside. Elevated vol has driven the selling, so a reset in volatility, while unlikely, could shift CTA behavior.

Source: TME/GS

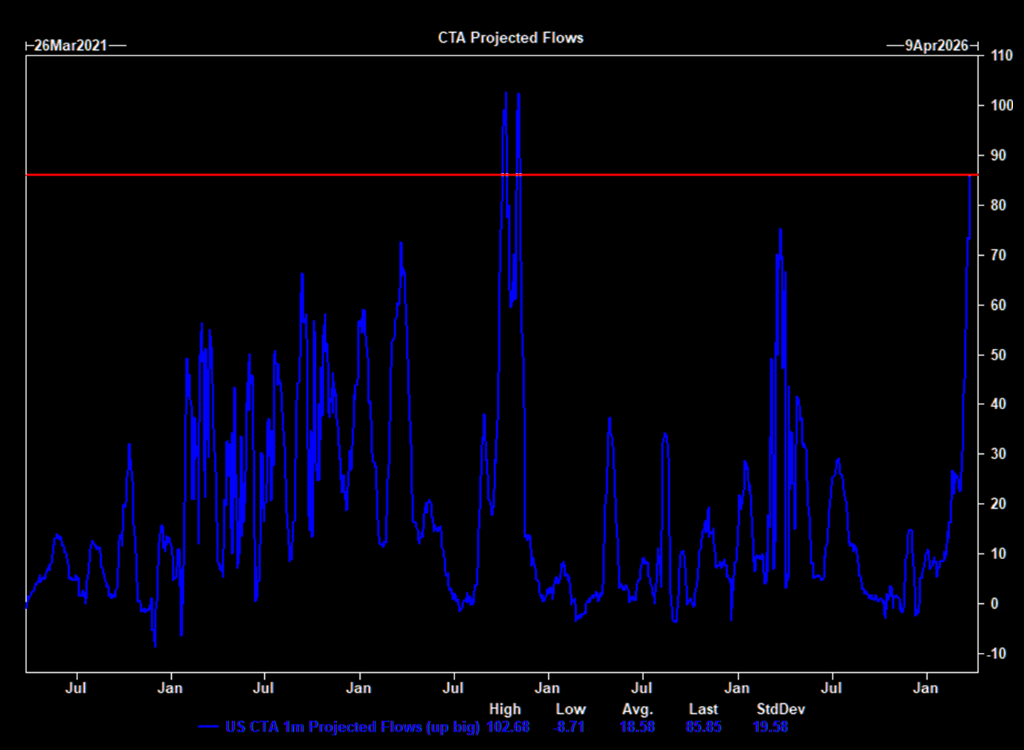

They could become big buyers

To the upside, CTAs could buy nearly $86bn of US equities over the next month if a sustained rally materializes, a move that sits in the 99th percentile over the past year.

Source: GS

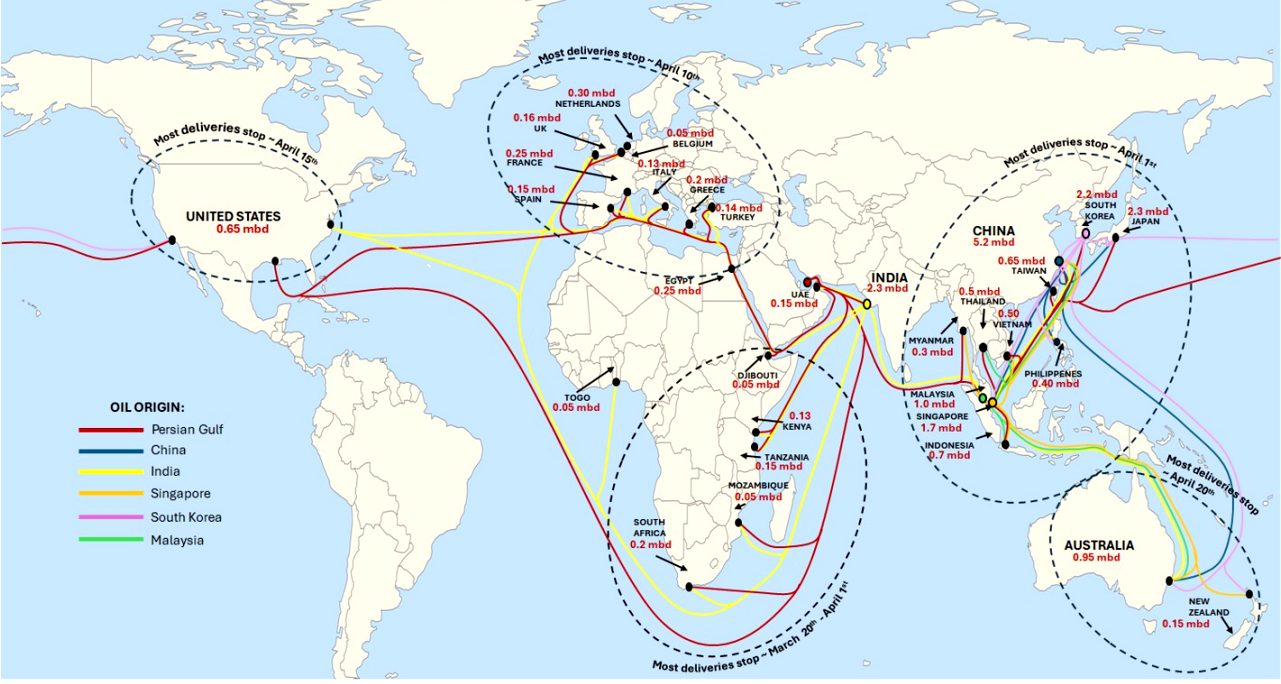

The clock is ticking

JPM's oil guru Kaneva:

1. Last tanker left Hormuz Feb 28 → the system is shifting from a flow shock to a stock depletion phase, where timing becomes as important as volumes.

2. Impact unfolds sequentially based on shipping times: Asia first (10–20 days), then Europe/Africa (20–35), with the US last (35–45).

3. Like COVID supply shocks, this is a rolling disruption moving westward, with uneven regional inventories determining how severe the impact becomes.

More on oil here.

Source: JPM

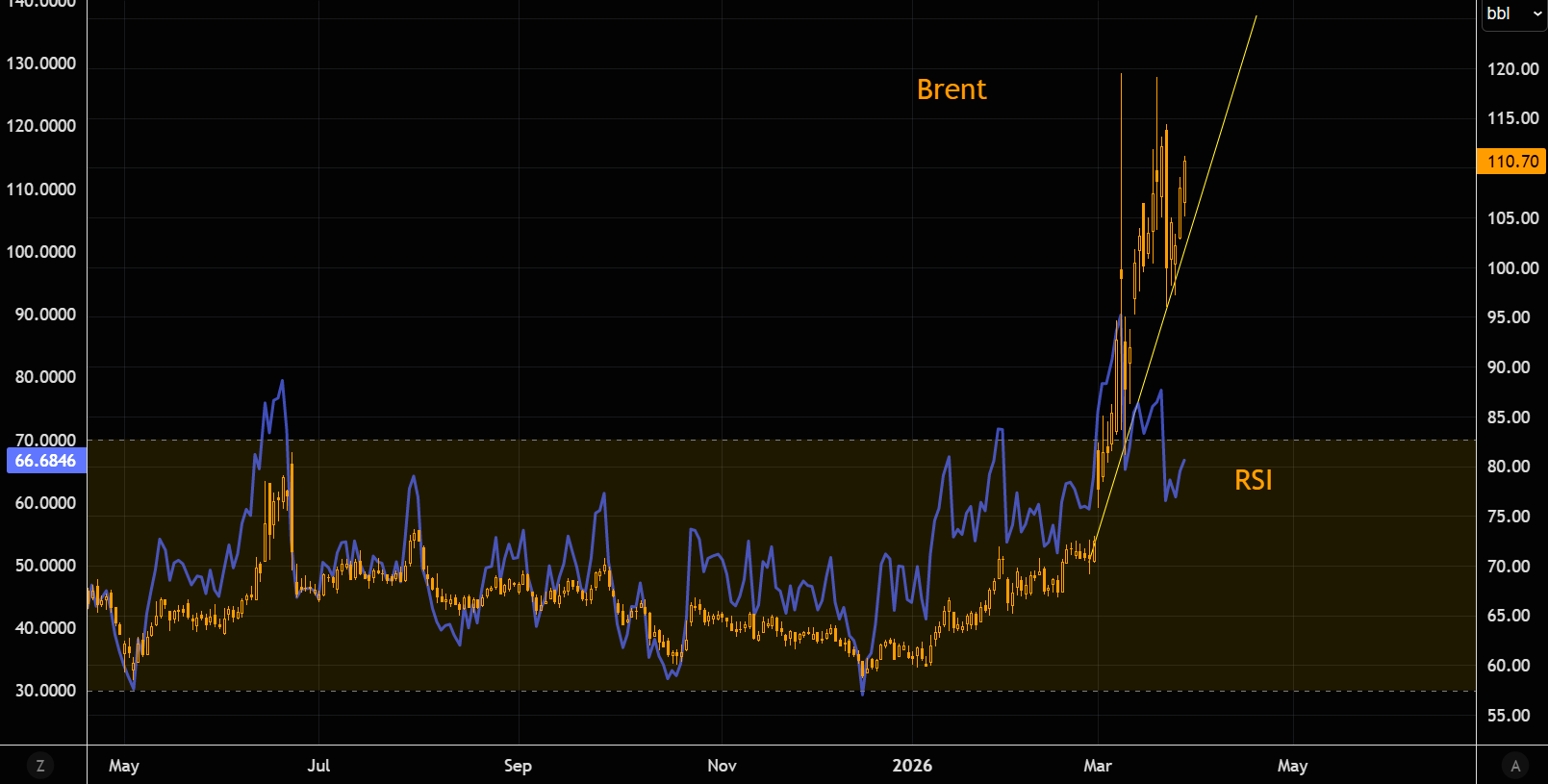

Not even very overbought

Brent RSI at 67. Overbought, but far from panic overbought levels we have seen over the past weeks.

Source: LSEG Workspace

Nervous into the weekend

Momentum remains lower for now, but fast money has already sold in size. Those same players could quickly flip into buyers if conditions stabilize, but for now markets still trade like momentum is in charge.