EM Is Breaking… Brazil Isn’t

The Brazil exception

EM is cracking under rising rates, stronger USD, and geopolitical stress, yet Brazil keeps attracting flows, holding levels, and ignoring the panic. When everything else weakens and one market doesn’t, that’s where you look.

EM is trading macro stress. Brazil is trading commodities and flows. EM is breaking. Brazil isn’t.

Resilient EWZ

EWZ has pulled back from recent highs, but Brazil continues to trade bid through the chaos. The dip barely tested the 100-day, never even getting close to the longer-term trend, and price has already bounced back to the short-term downtrend. A close above that level could quickly reignite the squeeze.

Source: LSEG Workspace

Not all EM is equal

EWZ is showing real resilience versus a battered EEM.

Source: LSEG Workspace

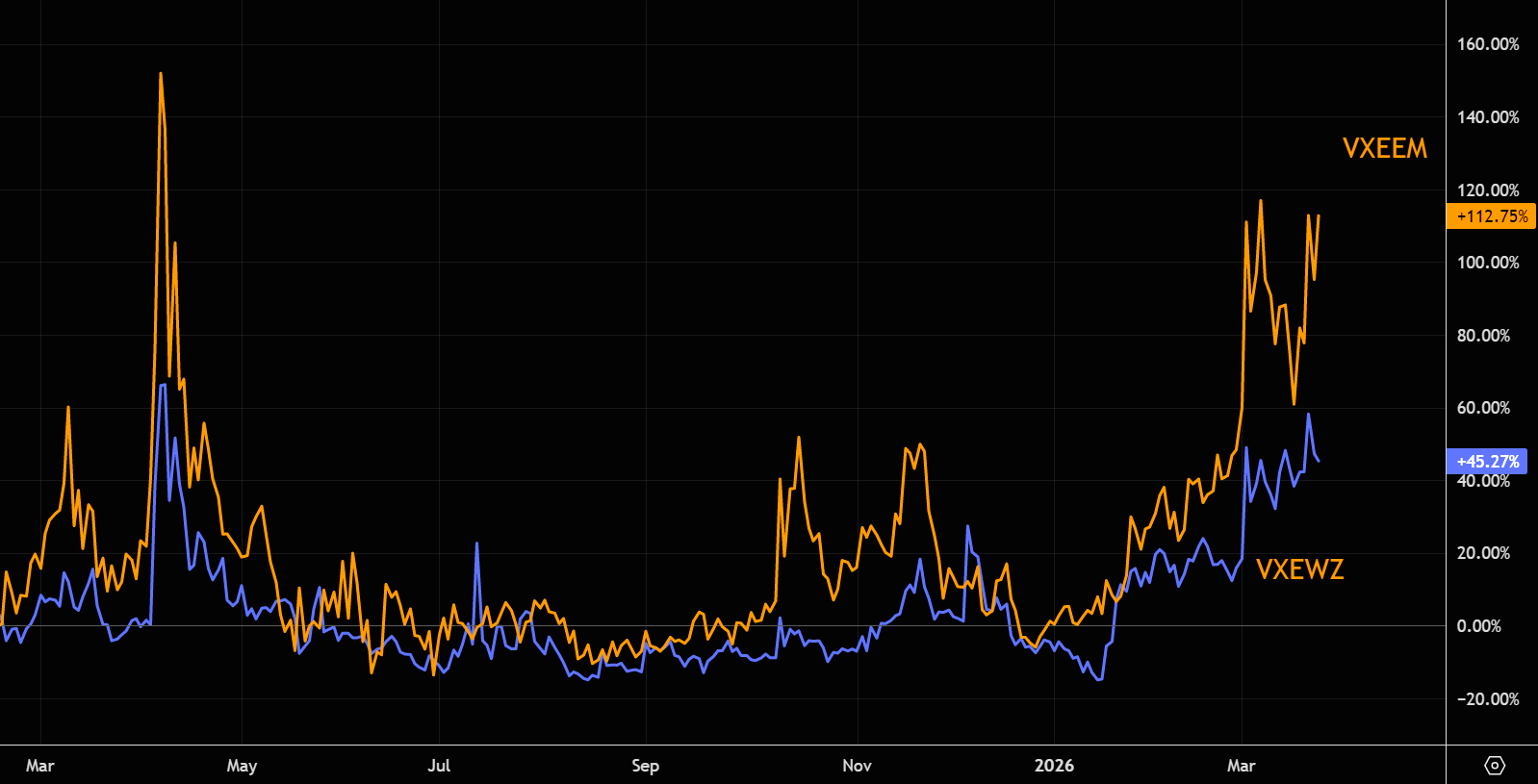

Less stressed

EWZ volatility (VXEWZ) has stayed relatively contained, while EM volatility (VXEEM) has spiked hard since the Iran war kicked off.

Source: LSEG Workspace

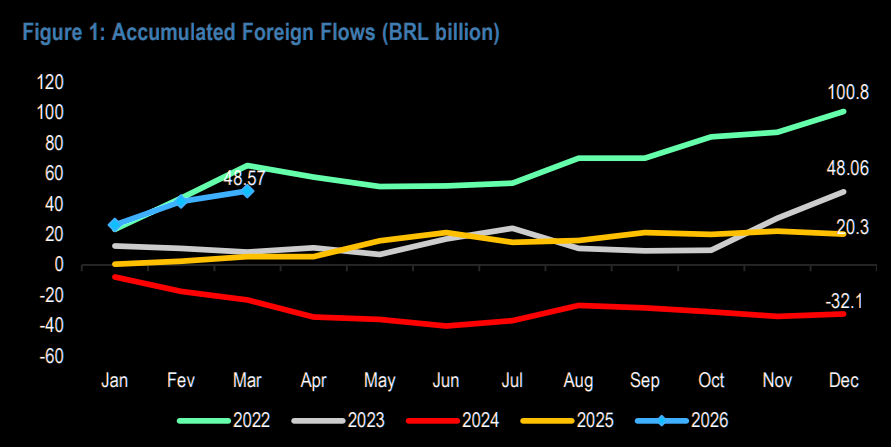

Healthy inflows

Brazil continues to see powerful inflows. Nearly $7bn has come in by March 19, taking YTD flows to ~$9.2bn, the second strongest on record after 2022. Out of 14 trading days in March, only 3 saw outflows, a clear sign demand remains persistent.

Source: JPM

The standout

It’s remarkable, Brazil is attracting strong inflows in the middle of a global risk-off. The USD is strengthening, yields are repricing, and EM has seen ~$8bn in outflows since the war started, yet Brazil keeps getting bid. This reinforces JPM's view: LatAm is acting as a safe haven within EM, and Brazil is leading the pack, reflected in its top-tier YTD and MTD performance. (JPM macro)

Brazil loves BCOM

Brazil is a pure commodity expression. When commodities bid, Brazil doesn’t just participate, it outperforms.

Source: LSEG Workspace

The "energy shield" effect

Unlike most EM that suffer from imported inflation during oil shocks, Brazil acts as a hedge. Rising production lets it capture upside from the Hormuz disruption without the same refinery cost hit, though reliance on diesel and gasoline imports remains a vulnerability.

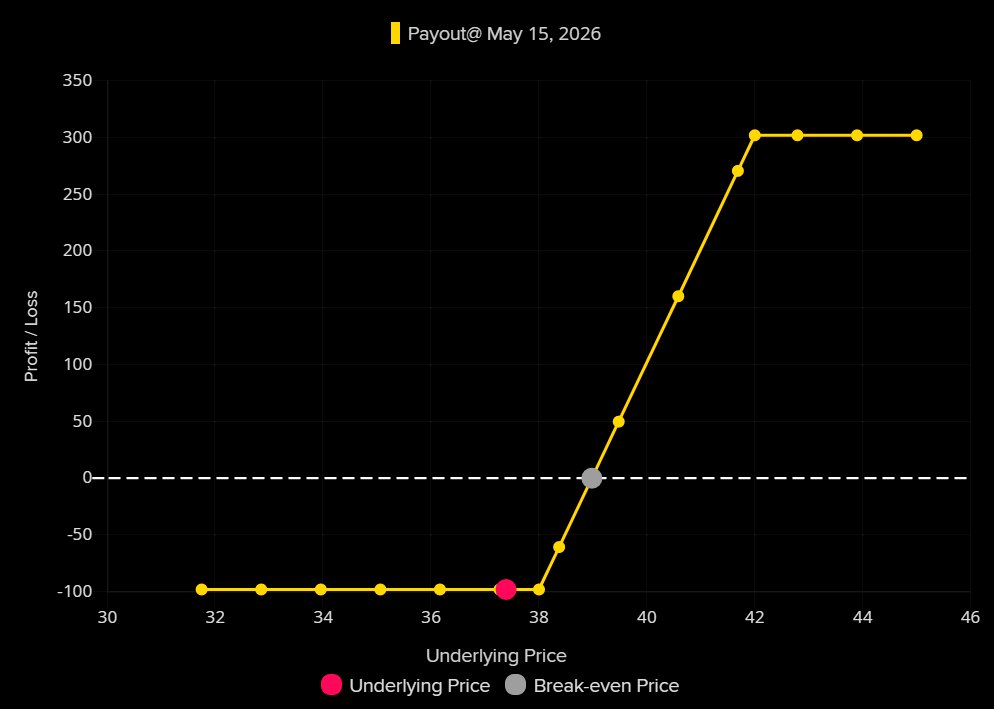

Brazilian options

Given EWZ’s resilience, positioning for upside via call spreads makes sense. The May 38/42 call spread offers roughly 4x max payout.

Flows are building, volatility is contained, and EWZ is holding key levels. If that short-term downtrend breaks, this turns from resilience into a squeeze, exactly where upside optionality pays.