"Europe to be hit by an inflation tsunami"

Stagflation fears return to Europe

Europe may be heading into another energy-driven inflation shock. Growth forecasts are being cut while inflation expectations are rising again, leaving policymakers facing the familiar risk of stagflation across the euro area. And hedge funds are voting with their feet with massive selling.

Fastest selling in almost a year

HFs net sold European equities last week at the fastest pace since mid-April ’25, driven almost entirely by short sales. Europe is now the most $ net sold region in March MTD.

Source: GS Prime

DAX darling debunked

Is it all over? Or put in a different way - was it just a blip in the structural downtrend?

Source: Bloomberg

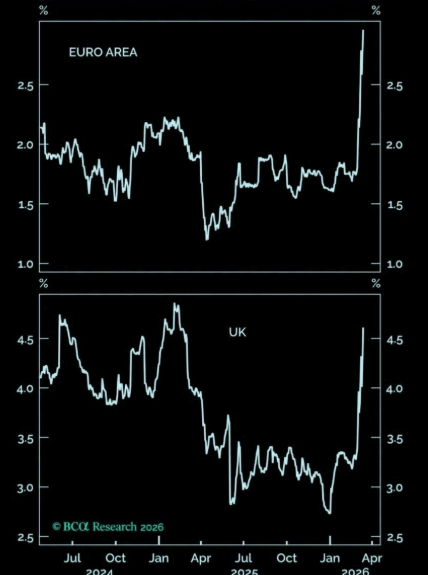

Inflation tsunami

Peter Berezin: "Europe, and to a lesser extent the US, are about to be hit by an inflation tsunami."

Source: BCA

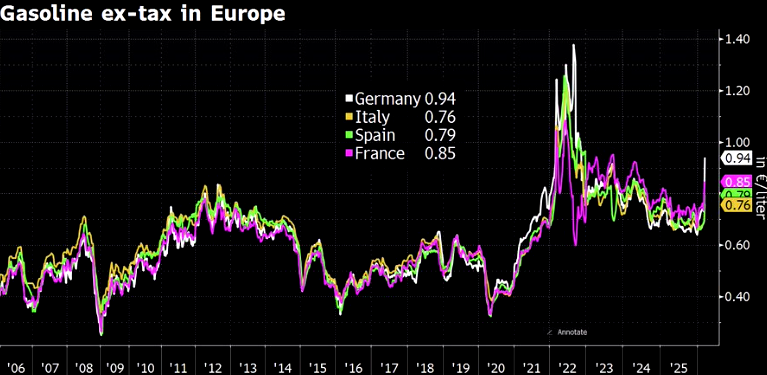

Filling up the car in Germany

In Germany, petrol prices have reacted much more sharply to the oil shock than in the rest of Europe. Excluding taxes and duties, petrol currently costs about 94 cents per litre at the pump in Germany, compared with 85 cents in France, 79 cents in Spain, and 76 cents in Italy.

Source: Bloomberg

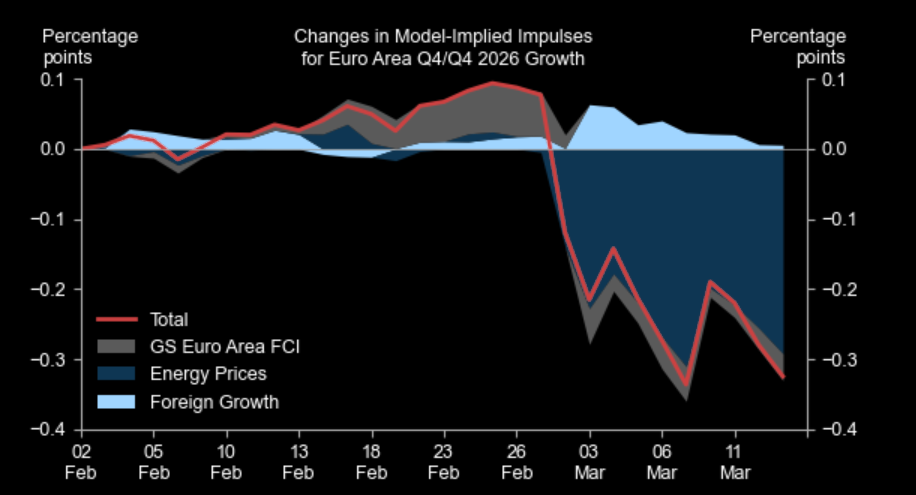

Hit it when it is already lying down

Goldman's model suggests the energy shock will reduce growth by roughly 0.3–0.4pp this year.

GS: "We have lowered our 2026 GDP growth forecast for the euro area by about 0.4pp and increased our inflation forecast by roughly 0.8pp."

Source: Goldman

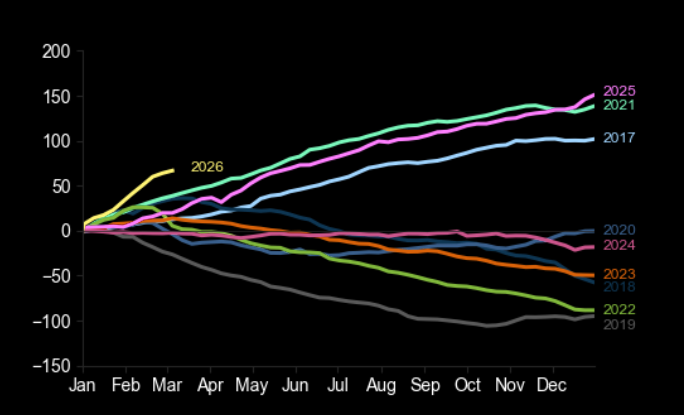

2026 stand-out year

Calendarised flows from Global investors into European equities, which means that there is...

Source: EPFR

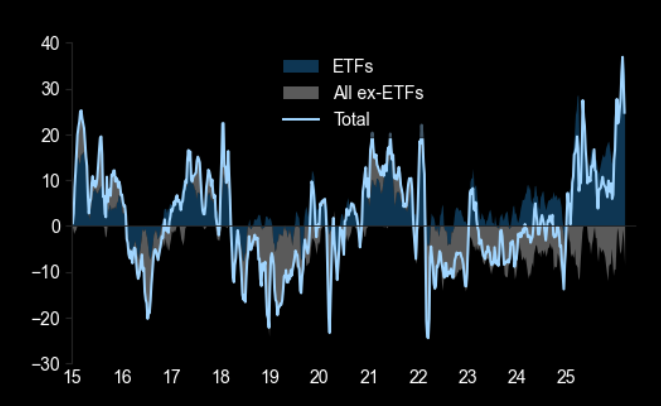

…room for reversal

1-month rolling flows from Global investors into European equities when presented like this looks unsustainably strong.

Source: EPFR

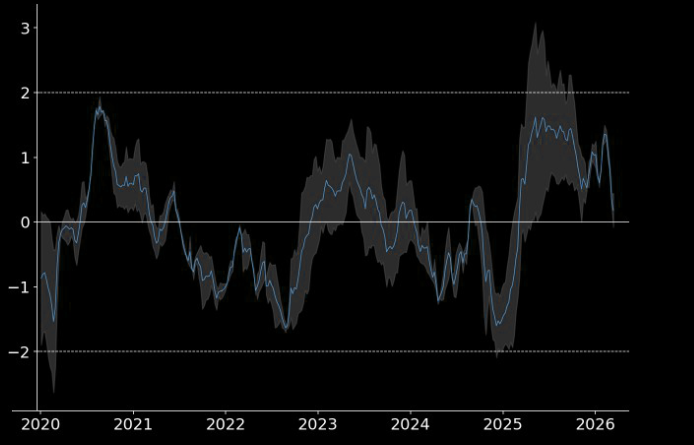

EUR/USD positioning reversed

Aggregate EUR/USD positioning proxies back almost fully to neutral. Chart shows JPM FX avg of EUR/USD futures positioning & options flows (10wk rolling, calls vs. puts). Z-score and range.

Source: JPM FX

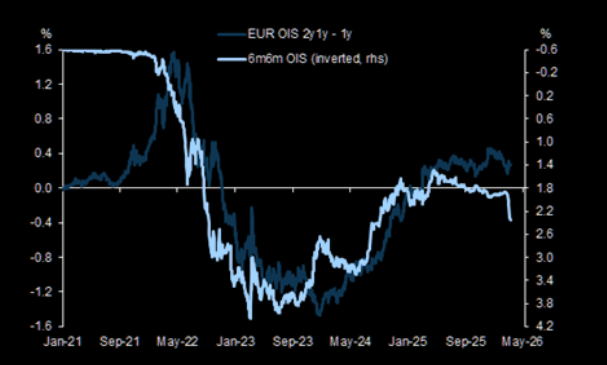

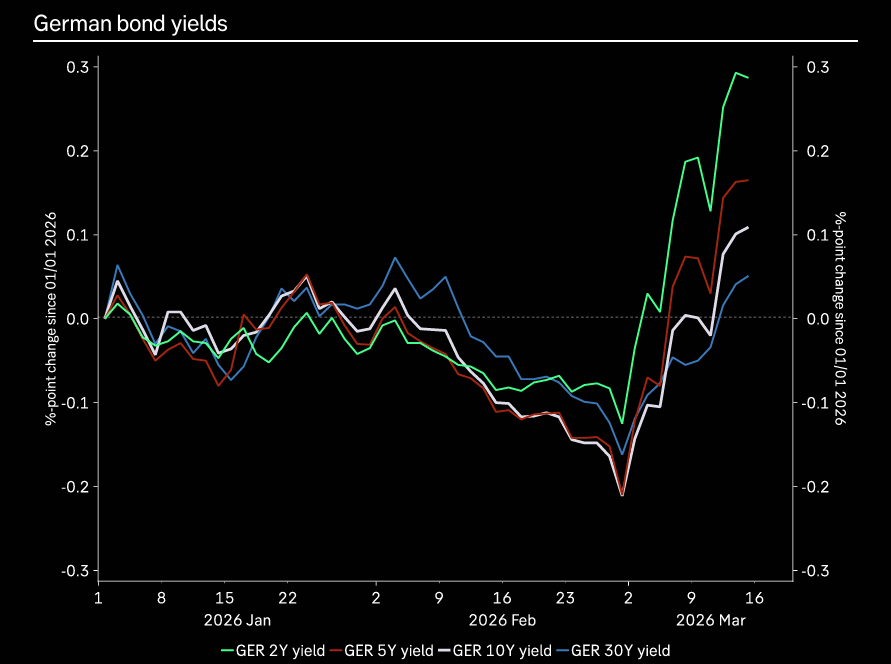

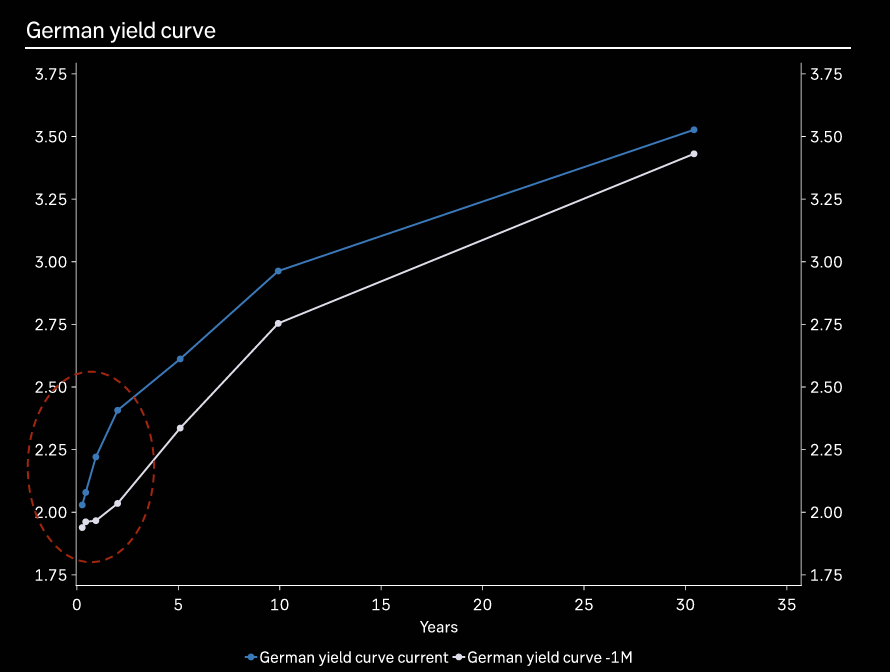

Bund yield upside harder to achieve

"...the growth-driven upside for Bund yields we have previously been expecting will be harder to achieve. As a result, we have revised our Bund curve forecasts flatter, with Bunds likely to stay around the 3% range for 2026 (rather than rise to 3.25% as we previously expected). In addition, the European front-end looks too steep for the level of hikes priced." (George Cole Head of European Rates Strategy).

Source: GIR

The curve

European 0-2 year yield curve steepens sharply, while the 2-30 year curve flattens.

Source: Macrobond

Source: Macrobond

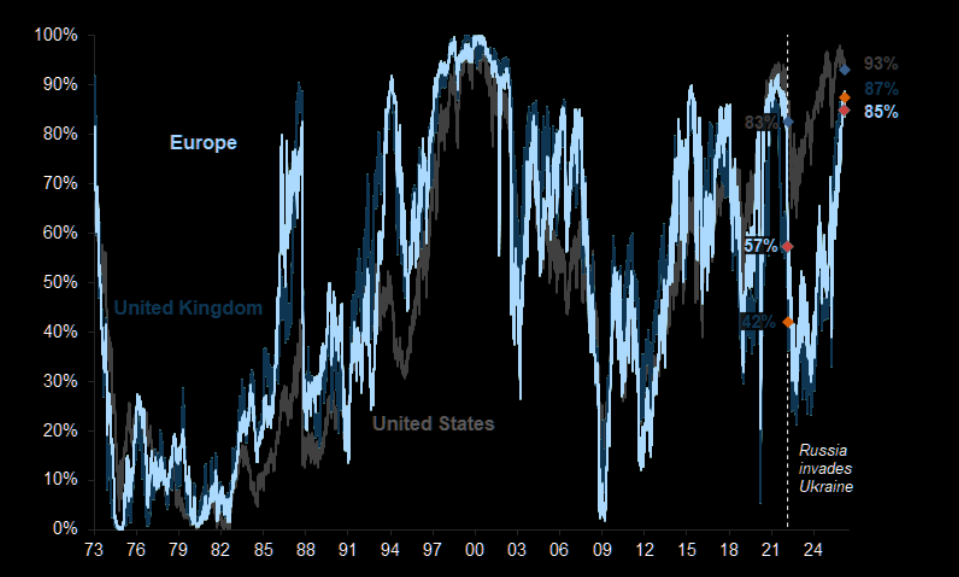

84th percentile

Europe is trading at the 84th percentile of its historical valuation range. Not cheap vs. history...

Source: Datastream

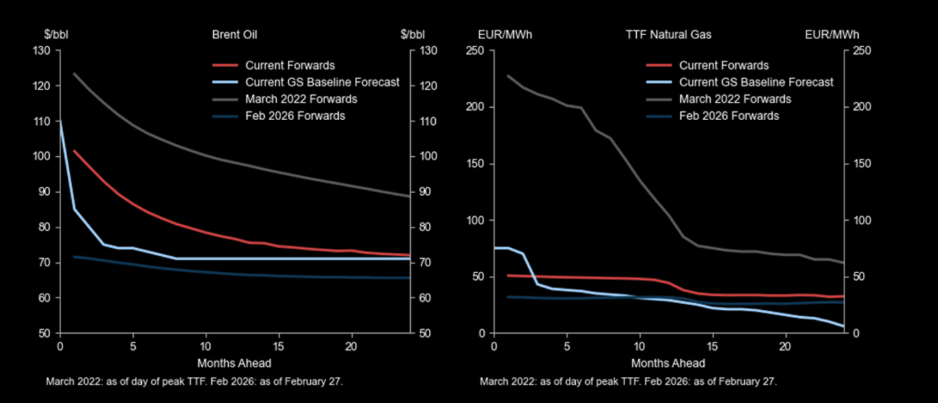

Less worse than 2022

Current shock is expected to be less persistent than in 2022 however. As always in Europe, hope springs eternal.