Europe Is Getting Hit From All Sides — And The Euro Is Cracking

Europe is getting hit from all sides

An energy shock, a deteriorating macro backdrop, and shifting policy expectations are all converging, and the euro is starting to reflect it. What looked like a contained selloff is now turning into something more structural.

Soggy Euro

The euro has sold off aggressively in the wake of the Iran war. We briefly bounced at the range lows, but the move has been weak and lacks follow-through.

Now sitting well below the 200-day moving average, with the 21-day crossing lower, a clear shift to a bearish trend.

Last time this setup played out, the euro didn’t stabilize, it continued the move lower.

Source: LSEG Workspace

The oil sucker

The historically strong inverse correlation between oil prices and the euro has reasserted itself post-conflict escalation; Europe’s heavy reliance on imported energy makes it disproportionately vulnerable to Gulf supply shocks compared to the US.

Chart shows how euro and oil (inverted) have moved in very close tandem since the "mess" began.

Source: LSEG Workspace

Painful

Euro longs were crowded just in time for the latest puke.

Source: Soc Gen

More euros to sell?

Further drop in skew suggests investors aren't done selling the euro long. Positioning is unwinding, but not yet washed out.

Source: Soc Gen

Terms-of-trade shock

Unlike the 2022 Ukraine crisis where Russian pipeline gas was cut, the current shock hits all importers equally, but Europe lacks domestic production buffers. This creates a larger drag on GDP growth for the Eurozone versus the US, widening the interest-rate differential gap against the USD.

Chart shows Citi economic surprises (US vs. EU).

Source: LSEG Workspace

Policy trap

Rising energy costs are forcing the ECB into a corner.

If inflation re-accelerates, rate cuts get delayed. If growth weakens, easing becomes harder. Policy flexibility is shrinking just as the shock is hitting.

ECB's headache

Bund yields are set to reprice faster than Treasuries as inflation lingers.

If Hormuz stays shut for more than a month, oil could spike toward $150, forcing the ECB into emergency tightening.

Source: LSEG Workspace

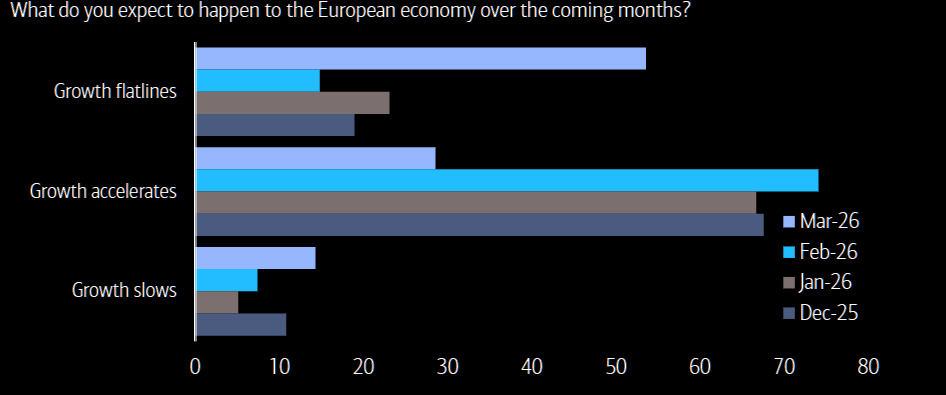

Throwing in the towel on Europe

BofA FMS: "54% of European investors expect growth in Europe to flatline in the months ahead, up from 15% last month, while 29% think the economy will accelerate, down from 74% previously"

This isn’t just a weak euro, it’s a market pricing a Europe that’s falling behind.