Everyone Is Hedged. That’s The Problem.

Rising fear

Despite the fact SPX has done very little this year, the VIX has continued to move higher and higher...

Source: LSEG Workspace

Tight

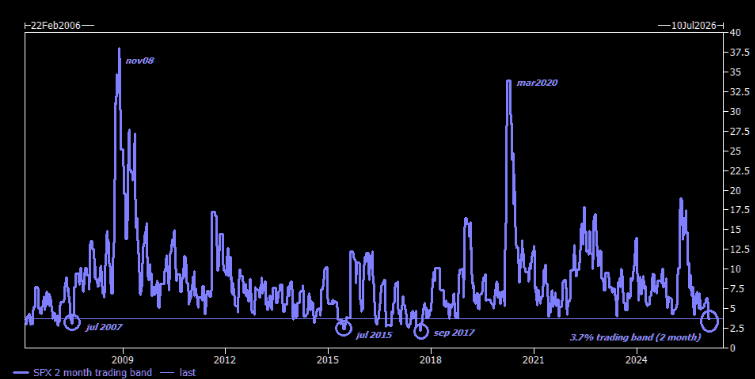

Doesn't feel like it but Garrett points out "...we just traded in one of the tightest two month ranges in history, with the 2month high/low closing range registering 3.7%, less than half the 20 year median of 8.6%".

Source: GS

but...

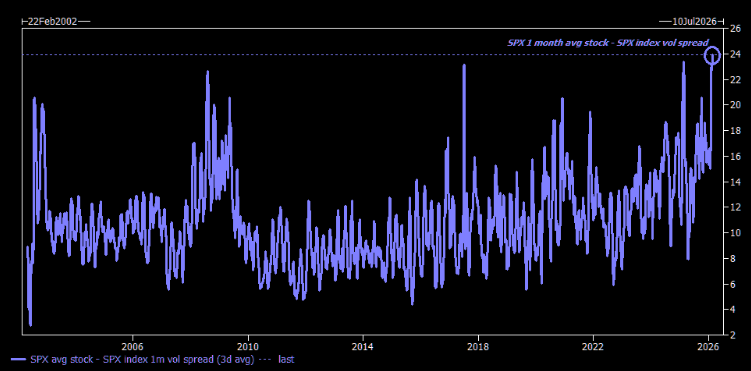

..."under the hood" this has been anything but boring, the realized vol spread of the avg single stock vs index just broke to the highest level on record with avg stock realizing ~25 vol points over". (There are plenty inverse dispersion quants still wondering what happened to their models telling them correlation was supposed to rise).

Source: GS

That feeling

Garrett nailing the "feeling": "The discomfort under the surface is (finally) manifesting in our weekly data … the quantum of selling / shorting / de-grossing / de-netting is more suggestive of a VIX at 35 vs a VIX at +/- 19 … investors continue to take down risk in what feels like preparation for the index to finally reflect what single stocks have been saying for a while (ie. “something’s got to give”)."

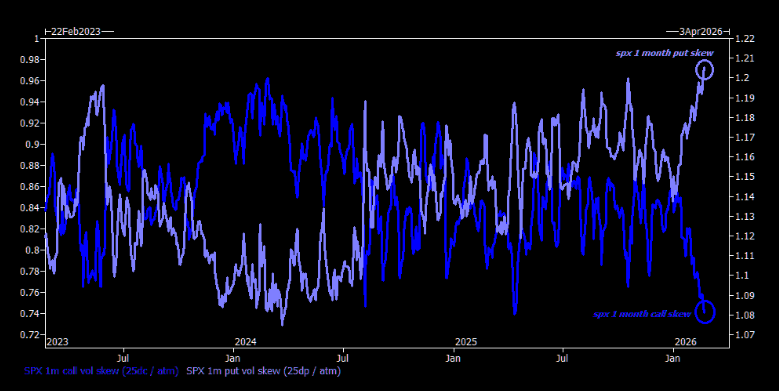

Extreme

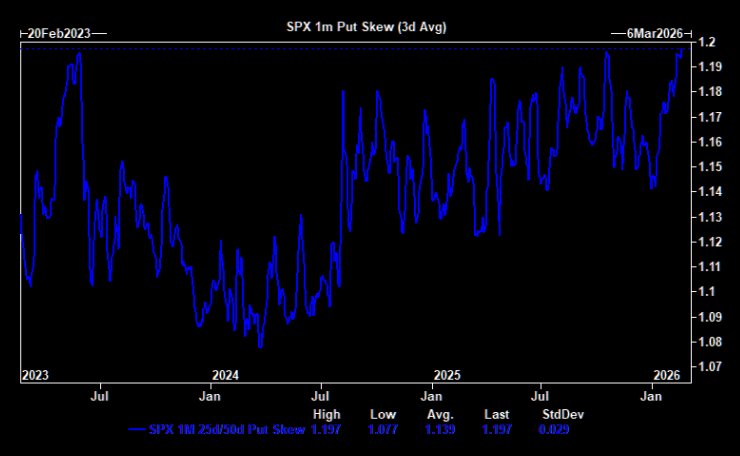

The rise in skew has been extreme year-to-date. The crowd is long and paying up for downside protection.

You can argue investors are “prepared” for a selloff and will monetize puts on a move lower, but also worth remembering, dealers who sold that protection become increasingly short gamma on a more serious move lower. That forces them to sell futures to hedge deltas dynamically, reinforcing and accelerating any downside move.

Source: LSEG Workspace

Use it

Elevated skew means that put spreads are priced relatively cheap as you end up selling the lower strike.

Source: GS

The case for a squeeze

Nomura's McElligott explains how an options driven squeeze could play out:

Point being: if spot equities continue to stabilize, those crowded VIX calls are going to melt, with plenty of room for implied volatility to compress further.

That feeds into a virtuous loop: as hedges decay, delta flows flip to equity futures buying. Vol-control strategies mechanically add back leverage as VIX resets lower, while under-exposed investors who recently cut net and gross risk may be forced to buy higher.

The kicker? A chase for upside via relatively “cheap” calls could create a spot up, volatility up dynamic.

Chart shows that upside skew has imploded. Downside skew has exploded.

Source: GS

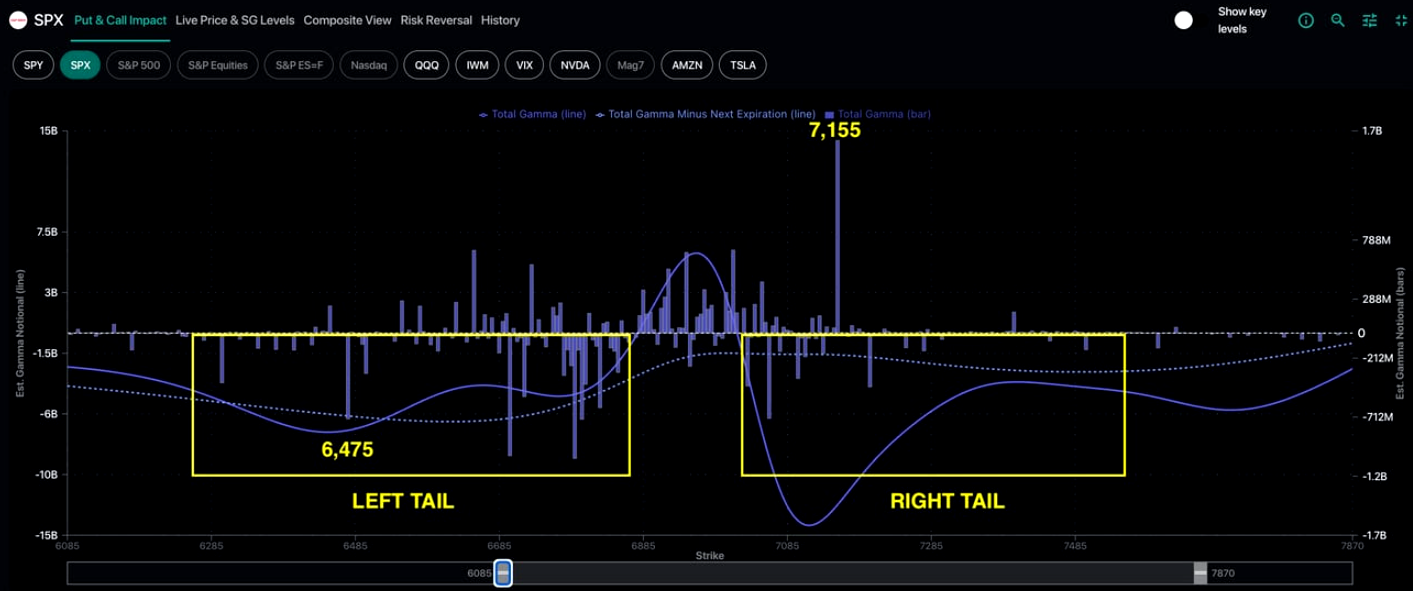

Gamma

The dealer gamma profile shows structural stability between 6,800 and 7,000, where positive gamma should dampen volatility. Outside of that zone, however, gamma flips negative, both above and below the range.

A sustained break in either direction would force dealers to hedge with price rather than against it, amplifying volatility. The key level into next week remains the 6,800 Risk Pivot.

Source: Spotgamma

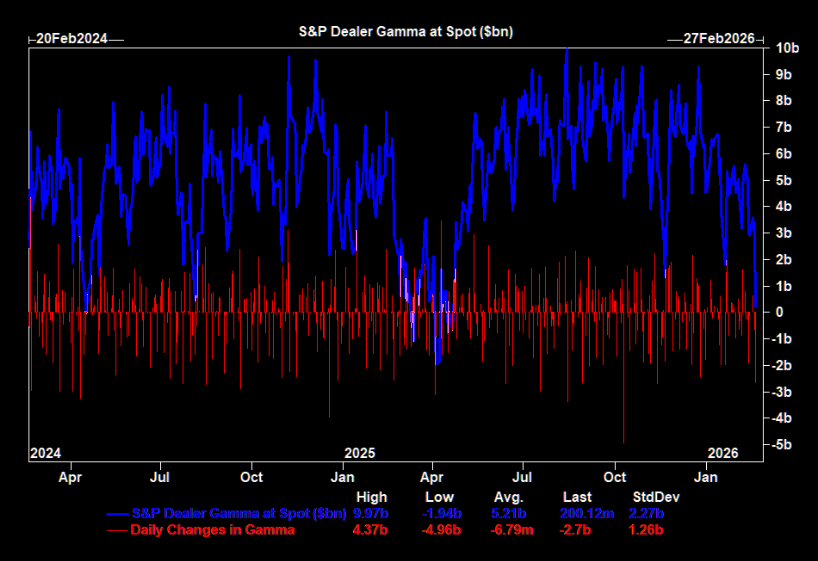

Will we move again?

Dealer gamma has collapsed toward zero after spending most of the past year in a supportive +$4–9bn range.

Low gamma isn’t directional, but it removes a key stabilizer, shifting the regime from grind/mean-revert to more reflexive, with bigger moves.