Gold Is Not A Hedge — It’s A Crowded Trade

Gold is failing

Gold is doing something it shouldn’t be doing. In the middle of a geopolitical shock, with volatility elevated and oil surging, the “ultimate hedge” is breaking down. The move isn’t just about price, it’s about what gold is failing to do.

Gold cracks

We’ve been flagging fading momentum in gold for weeks (most recently two days ago). The metal is now printing one of its largest down candles since the early-February puke and is breaking below the 50-day moving average, a level it hasn’t closed beneath since last summer. Key support comes in at $4800, with the 200-day moving average near $4600.

Source: LSEG Workspace

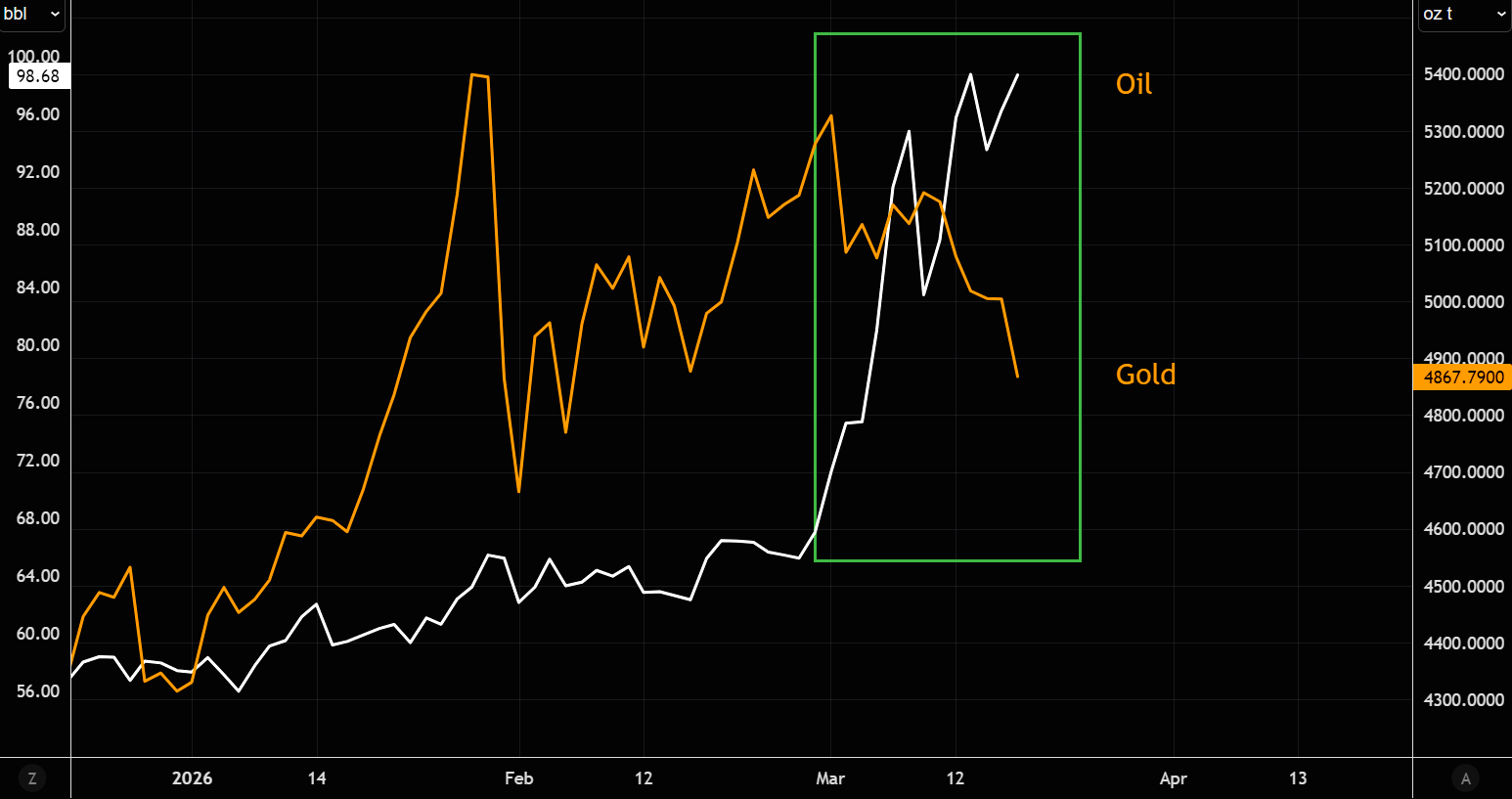

Not an oil hedge

Gold and oil have moved in opposite directions since the Iran war began, not exactly supporting the idea of gold as a reliable geopolitical hedge. Chart 2 (gold vs. oil, inverted) makes the relationship even clearer.

Source: LSEG Workspace

Source: LSEG Workspace

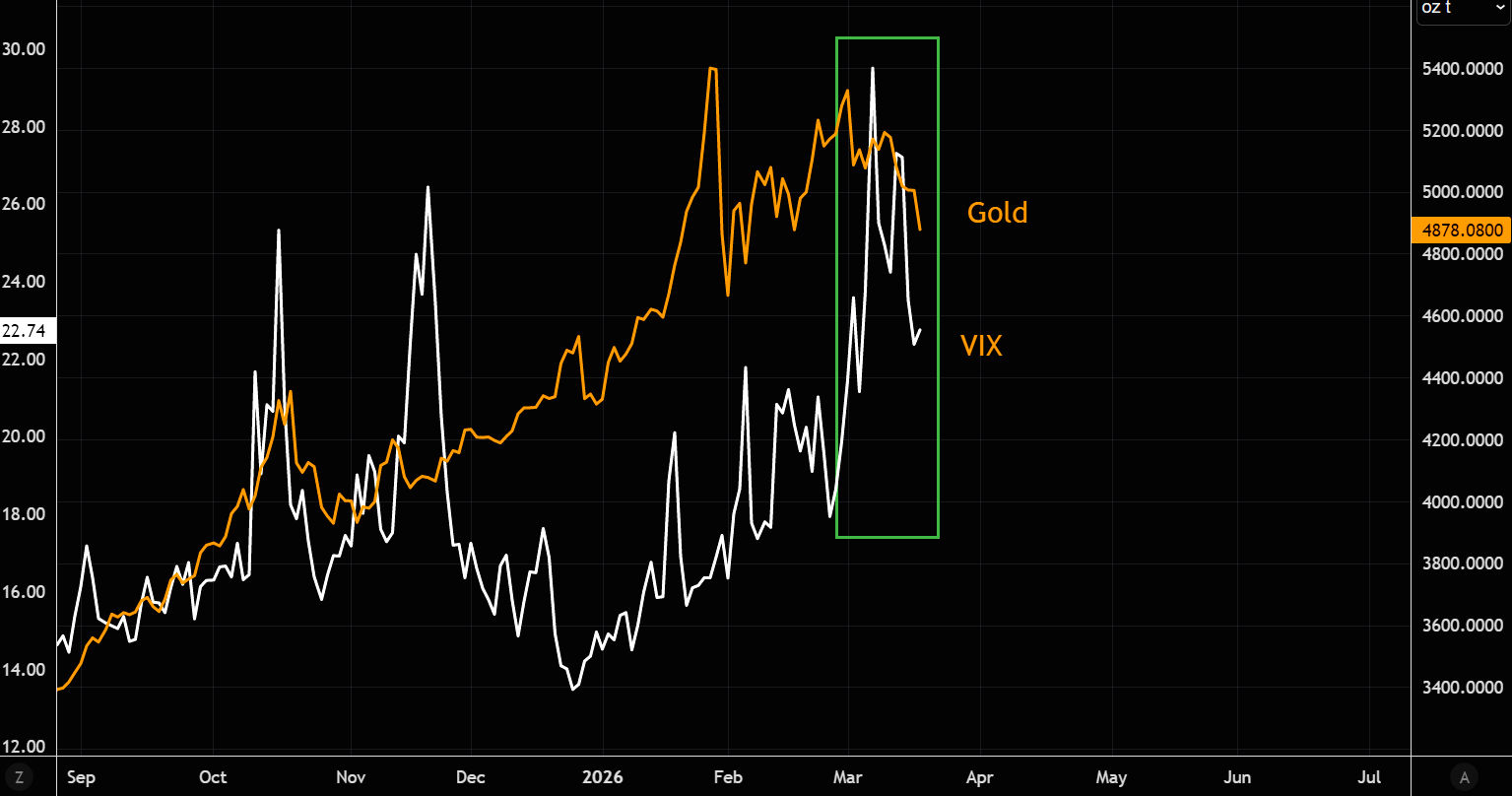

Not a VIX substitute

Gold has dropped from around $5300 to below $4900 as the VIX has spiked. While volatility tends to mean revert, gold is clearly not a reliable VIX hedge.

Source: LSEG Workspace

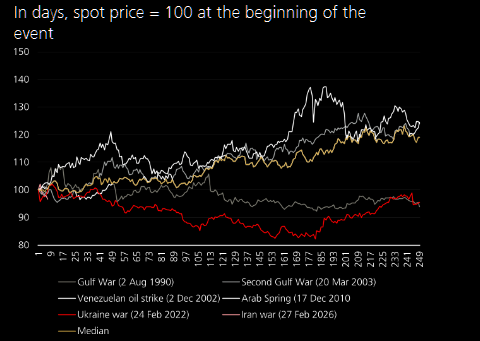

The war paradox

Gold is widely seen as the ultimate geopolitical hedge, but history says otherwise. It typically rallies on the initial shock, only to fade as markets shift toward liquidity and assets directly tied to the conflict, like energy. We saw the same in 2022: gold surged ~15% post-Ukraine invasion, then dropped 15–18% as the Fed tightened.

Source: UBS

Follow the beta?

Gold miners continue puking. Last time GDX traded here, gold was at $4500.

Source: LSEG Workspace

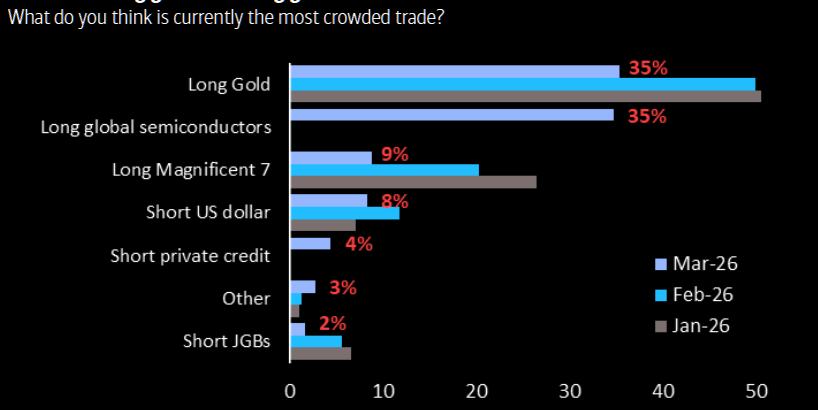

Crowded gold

Gold still in pole position when it comes to being a crowded trade.

Source: BofA

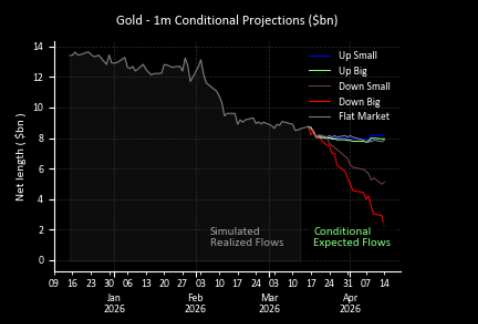

Downside convexity

CTAs needing to sell gold.

Source: GS

Rate cut dissapointment

HSBC warns: "Should anticipated cuts fail to materialize in 2026, we may see a break in the gold rally."

Gold and SPX

Gold correlations to equities have picked up; expect continued beta exposure during broad risk-off moves (e.g., selling gold to fund equity hedges).

Overall conclusion: This isn’t a hedge unwinding, it’s a crowded trade getting exposed.

Source: LSEG Workspace