The Grand Old Man Of Strategy Warns: "Near-Term Risks Are More Elevated"

Signs of strain

Peter Oppenheimer, one of Wall Street’s most experienced strategists argues the risk backdrop for equities has changed. After an unusually strong post-pandemic rally, valuations across regions are elevated, equity risk premia have compressed sharply and leadership within the market is shifting. The near-term risk of a correction is rising even if the probability of a full bear market remains low.

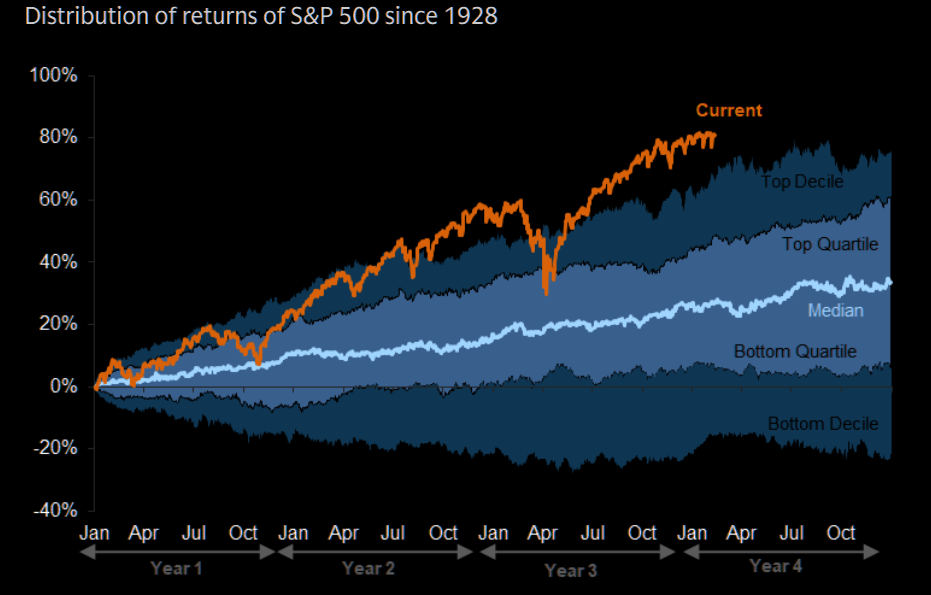

Unusually strong

Oppenheimer: "Near-term risks are more elevated given that the equity bull market, particularly from the pandemic lows and led by the US, has been unusually strong."

Source: Goldman

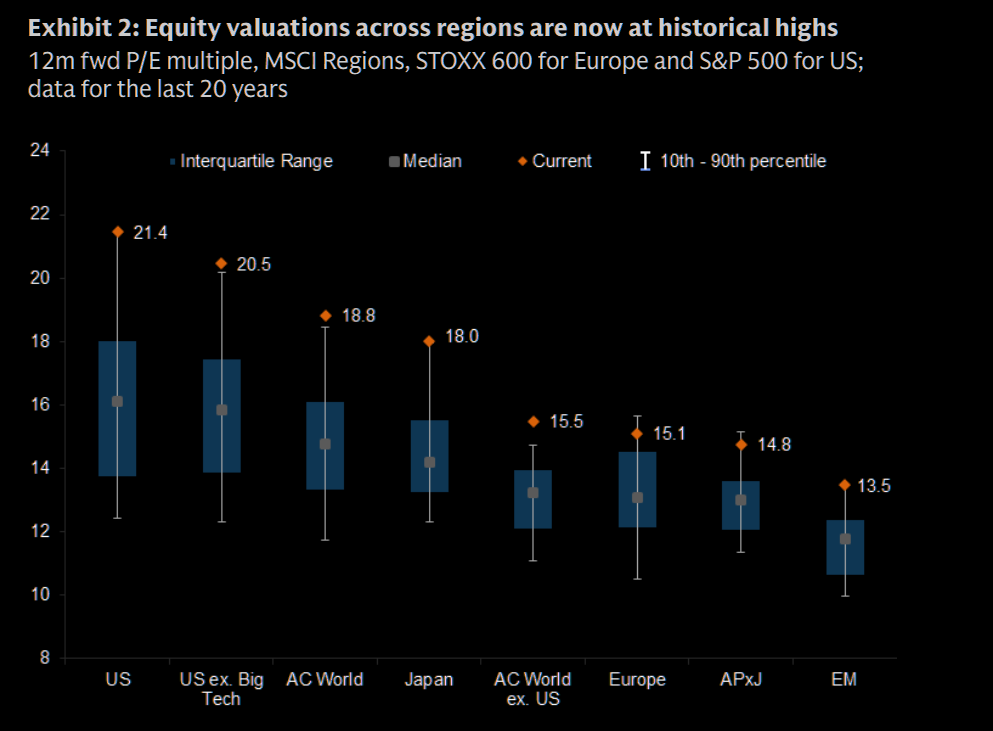

Elevated valuations

Oppenheimer: "...broadening of equity returns outside of the US market over the past year has resulted in all regions now having valuations above their own longer-term histories."

Source: FactSet

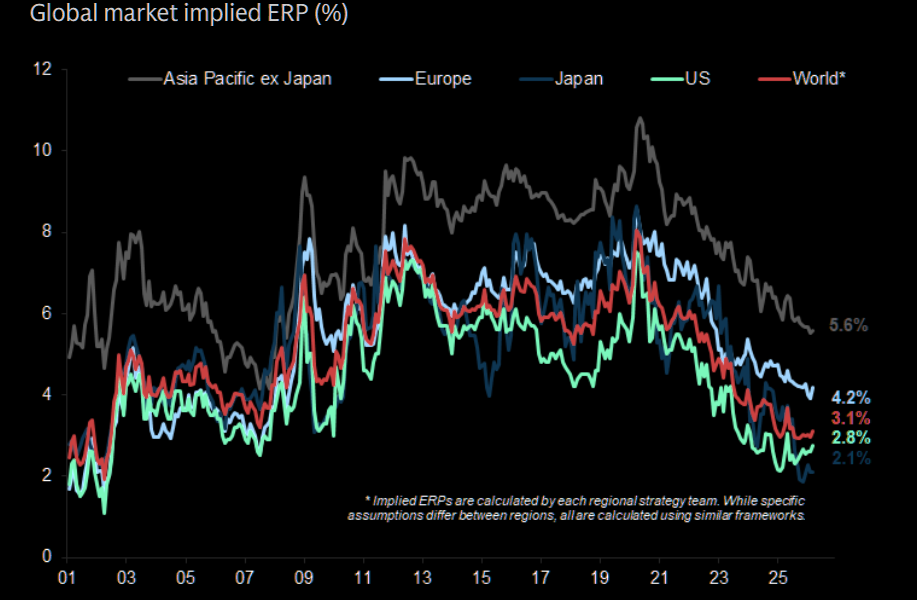

More vulnerable

Equity risk premia have fallen sharply and are now, mostly, back to levels seen in the run-up to the financial crisis.

Oppenheimer: "These valuations, while justified by improving margins and prospective returns on investment, have left equities more vulnerable to disappointments or shocks driven by technology competition or the growth/inflation mix that might worsen because of developments in the Middle East."

Source: Goldman

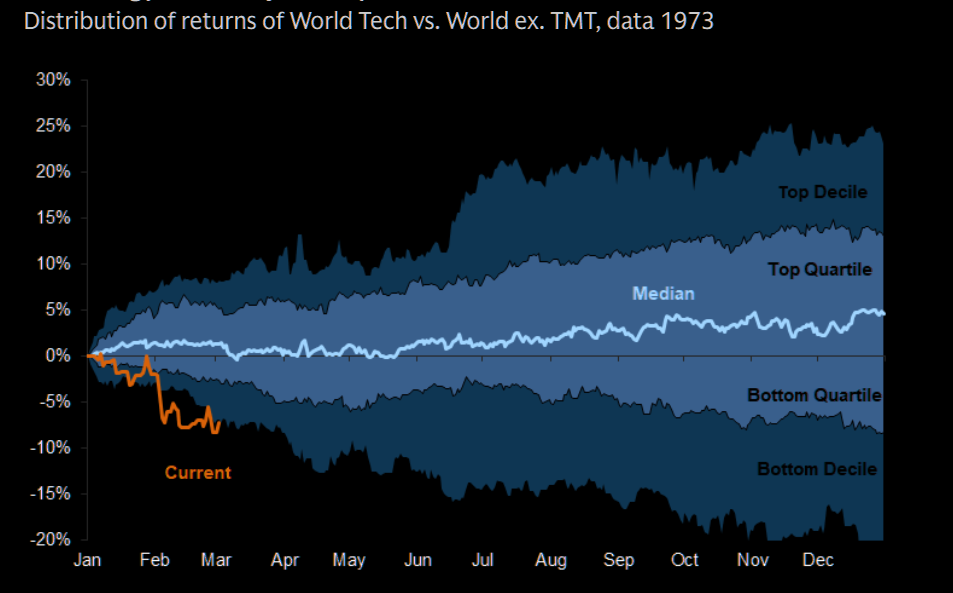

Terrible tech

We have of course seen one of the weakest periods of relative returns for technology compared with other sectors over the past 50 years.

Oppenheimer: "Recent anxiety about tech valuations, capex plans and the disruption to business models (particularly in areas around software) has resulted in a de-rating of longer-duration cash flows in favour of more certain nearer-term returns in physical capex and infrastructure."

Source: Datastream

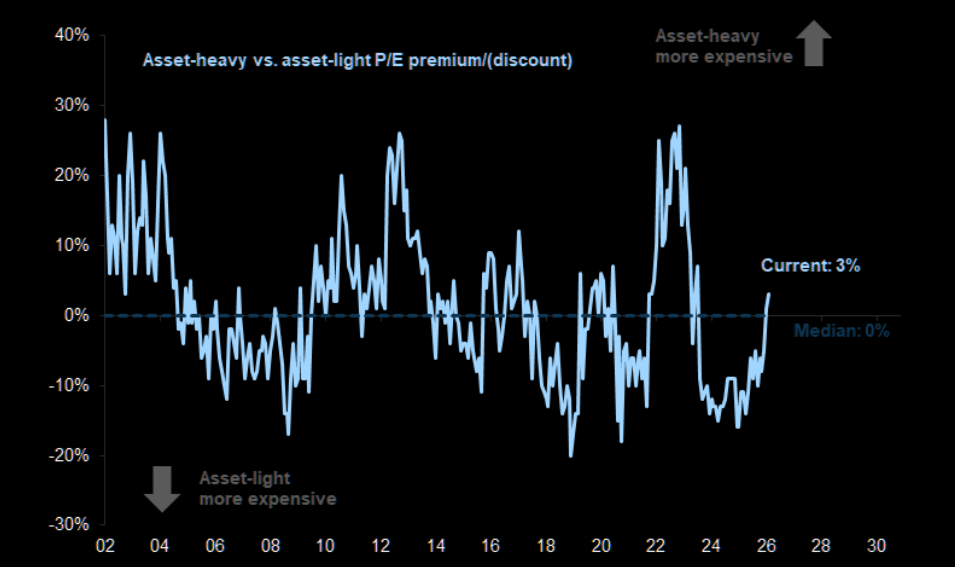

New! Asset heavy at a premium

US Asset-heavy stocks now trade at a P/E premium to asset-light stocks.

Source: Datastream

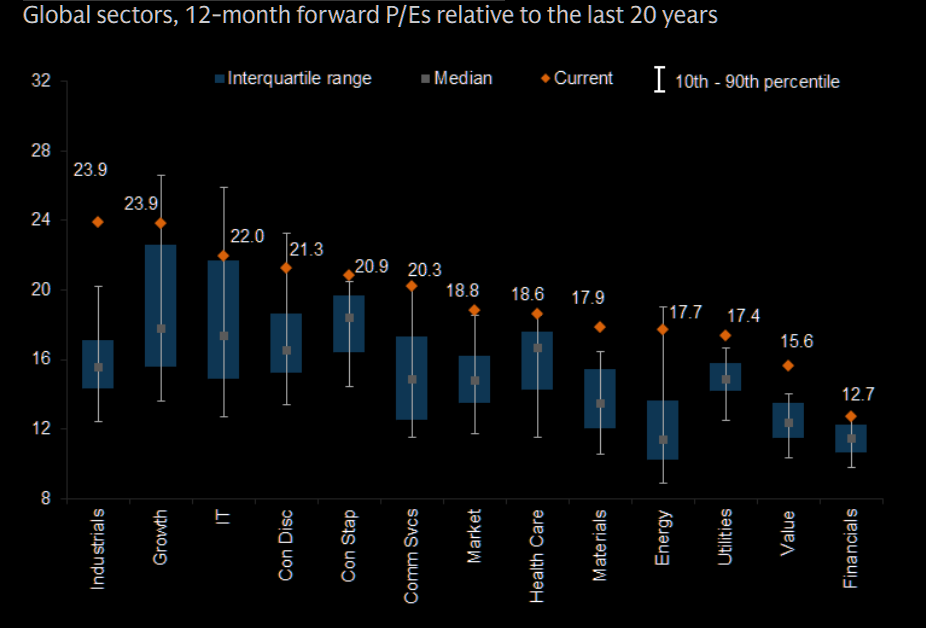

New! Industrials > IT

Global Industrials now trade at premiums above 20-year averages, surpassing IT sector valuations.

Source: FactSet

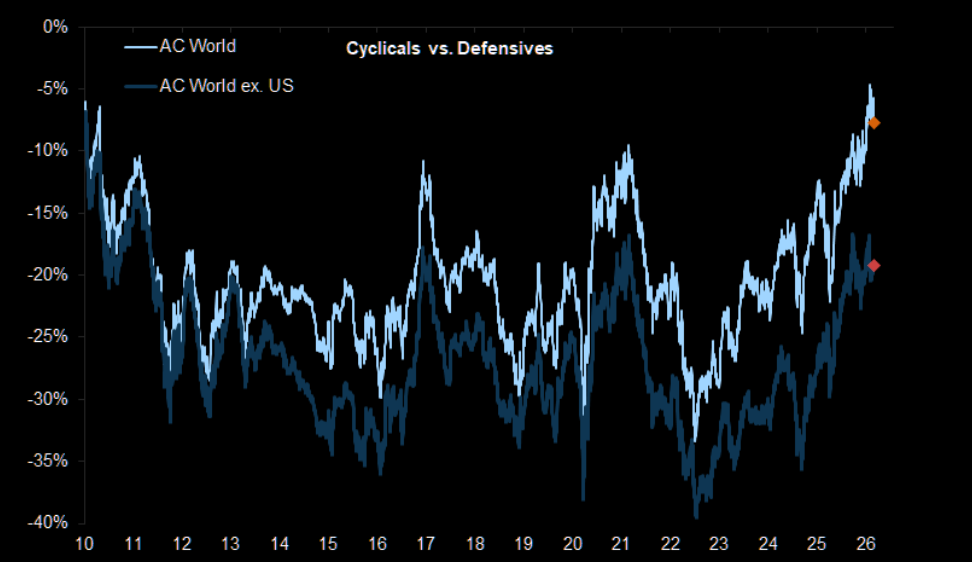

New! Cyclicals are now as expensive as defensives

Oppenheimer: "Cyclicals are vulnerable to any erosion of confidence in the short term if oil prices rise further or if there is increased disruption to trade. There is also a risk that the waves of de-rating that we have witnessed in many areas of technology that are feared to be ripe for disruption spill over into more concerns about rising unemployment."

Source: Goldman

Low risk that it morphs into a bear market

Oppenheimer is not long-term worried...

"The growing concerns about technology and geopolitics point to further near-term correction risks at the broad equity index levels rather than the sharp rotations beneath the surface that we have seen so far this year. But the depth and extent of any correction are likely to be limited, in our view, with relatively low risk that it morphs into a bear market."

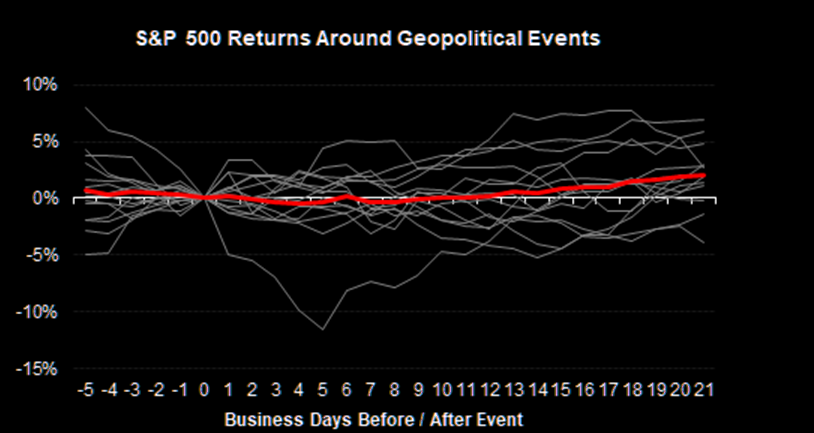

US equities are generally resilient to conflicts

Oppenheimer: "It is worth noting that most geopolitical shocks in recent years have not had a long-lasting impact on markets."

This is similar to what Morgan Stanley wrote yesterday.

MS: "While this is not an exhaustive study, based on 14 events over the last few decades (generally major, as well as some recent smaller Iran related incidents) the S&P 500 is generally range bound following the start of a conflict. The event causing the largest drawdown in this sample was September 11th, 2001."

Source: MS QDS

3 macro hedging trades from the GS trading desk

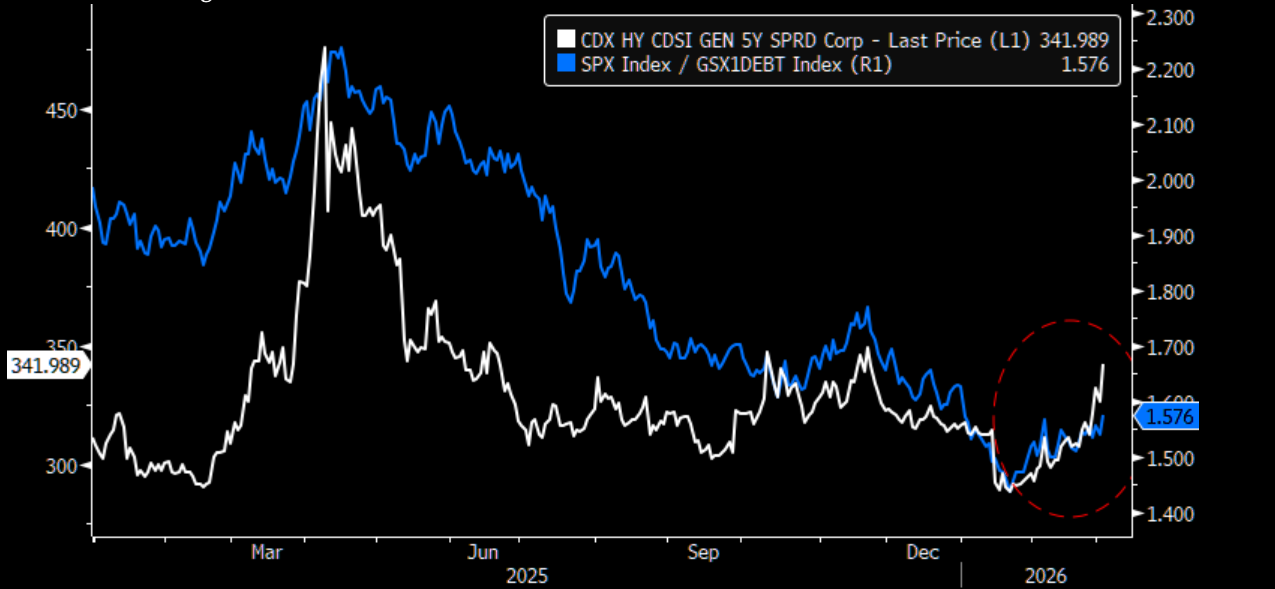

Trade 1: Shorting high yield sensitive equities

"We like going short our basket of high yield sensitive equities: GSXUDEBT, given high yield credit spreads are expected to widen in-line with GS forecasts. The GSXUDEBT basket is composed of CCC-rated issuers and non-rated companies with similar fundamentals (negative free cash flow and high debt ratios)."

Source: GS trading desk

Trade 2: Long geopolitical basket

"Our Geopolitical basket (GSXUGEOP) is composed of defense (GSXUDFNS), oil producers, and oil tankers. Relative to the S&P excluding AI (SPXXAI), the basket is up ~23% YTD driven by both the defense and oil exposed names."

Source: GS trading desk

Trade 3: Short high beta long low beta

"In a market drawdown, being short high beta vs long low beta names have paid off every time. Our Beta pair (GSP1BETA) have proven to be an efficient hedge during the top 10 SPX drawdowns in the last 10 years (100% hit rate)."