Heavy De-Risking In A Stuck Market — Is The Pain Trade Higher?

Still stuck

SPX futures remain trapped inside the same range that’s been in place since last autumn. Aside from a few failed breakout attempts, the SPX has essentially chopped around in a ~200-point band. We’re currently sitting just below the 50-day and above the 100-day moving average.

Support: 6800, 6700, and the 200-day (currently ~6765). Resistance: 7000. (futures)

Source: LSEG Workspace

NASDAQ

Tech futures remain stuck in the same range we’ve traded since autumn, but momentum here is notably weaker than in the SPX. We’re hovering near range lows, the 50-day is crossing below the 100-day as we write, and the 200-day is looming just beneath.

24,500 (futures) is the clear line-in-the-sand level, but from a positioning perspective, is a tech bounce now the real short-term pain trade?

Source: LSEG Workspace

MAG hopes

MAG bounced right on the range lows on Friday, putting in one of the bigger up candles we have seen in a long time. This space could easily bounce more, and still just be stuck.

Source: LSEG Workspace

AI is dead…

…long live AI? AIQ has managed to bounce, printing one of the larger up candles in some time. Despite all the noise and doom narratives, the broader AI trade has been range-bound for months, and from a pure positioning/technical perspective, it could easily squeeze higher from here.

Source: LSEG Workspace

Less roaring

Russell still the relative king YTD, but not so much over the past week...

Source: LSEG Workspace

Source: LSEG Workspace

Fast and furious

The crowd has been chasing everything but tech. Could we see a little mean reversion, with tech regaining some of that lost mojo? The chart shows the Russell/NDX ratio.

Source: LSEG Workspace

A nothing week?

For a week where “nothing happened,” global equities just saw the largest net selling since Liberation Day (not a typo). Gross activity continues to rise, driven almost entirely by short sales, and it’s not just hedge funds hitting bids. The long-only community finished the week -$4bn better for sale ($10bn better for sale month-to-date), marking one of the largest monthly sell skews from asset managers in four years. Other notable heavy sell months include Aug 2022 (-$18bn), Mar 2024 (-$14bn), and Mar 2025 (-$22bn). (GS PB, Garrett)

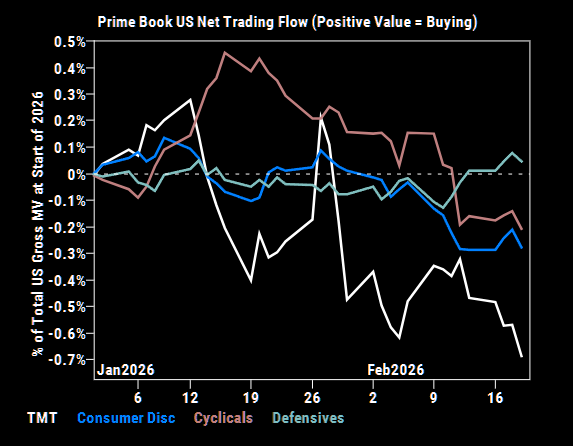

Selling TMT

Last week, TMT made up roughly 70% of total net selling in single stocks, with short sales outpacing long buys by 4.5 to 1, highlighting that the pressure was driven primarily by aggressive shorting rather than outright long liquidation.