More extended hedge fund positioning meets Trump's new tariffs

Perhaps a temporary pause

The European economy momentum is continuing to deliver on all cylinders (Volkswagen Polo style, not Audi RS7) and German equities continue to look cheap. But even though the new Trump tariff news won't derail this it will create short-term uncertainty. And hedge fund positioning has perhaps become a little too stretched. Let's have a look at the latest relevant charts in Europe.

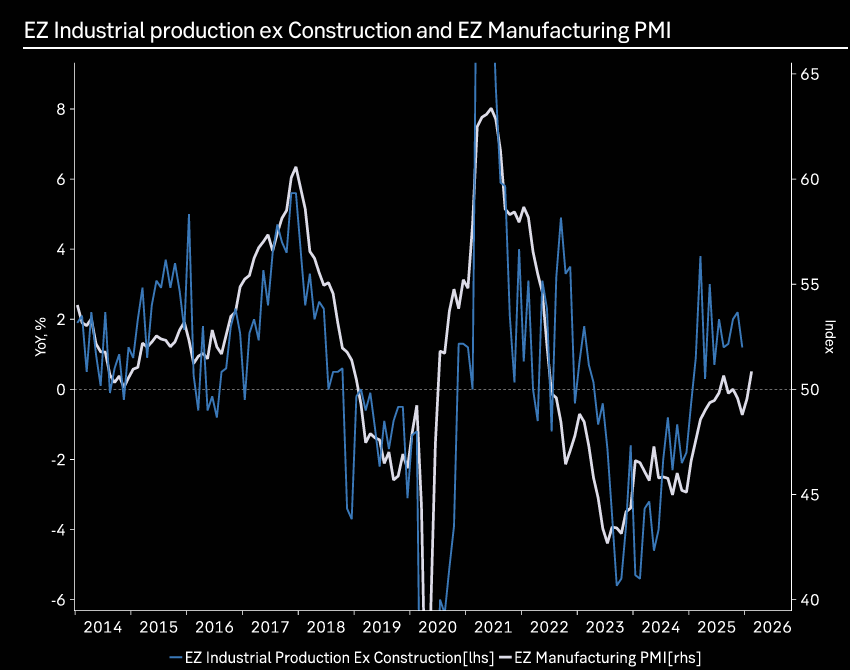

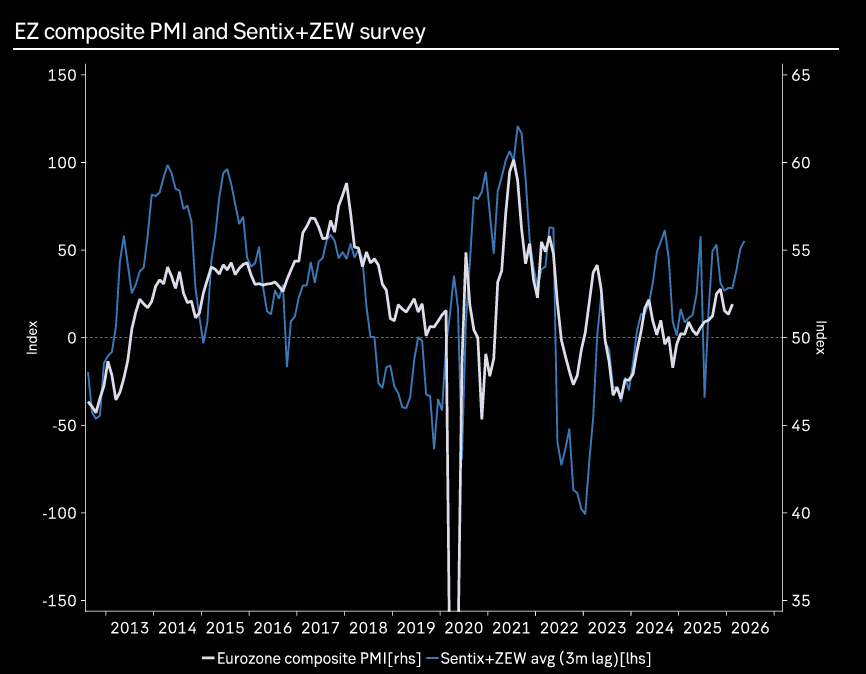

Marvellous macro

Eurozone manufacturing PMI leaps to the highest level since 2022, Sentix/ZEW rise too.

Source: Macrobond

Source: Macrobond

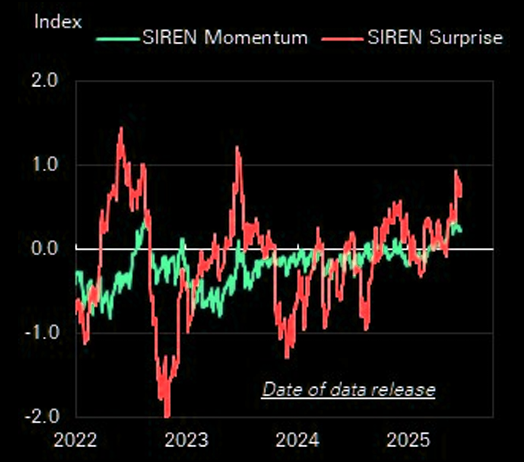

SIREN screaming

SIREN indices continue to show strong momentum on the back of positive Feb survey releases.

Source: Deutsche Bank

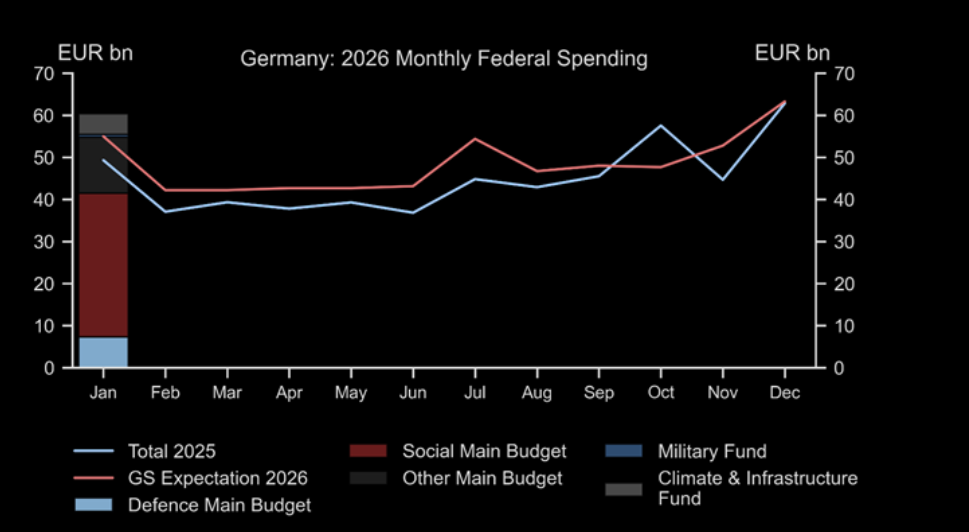

Spending all your money

"German federal expenditures in January came in at EUR 60.4bn, about EUR 5.4bn above our expectations and EUR 11.1bn above January 2025. The strong start to federal spending in 2026 supports our view of a notable fiscal expansion this year, which we expect to contribute around 0.5pp to our growth forecast of 1.1% this year."

Source: Goldman

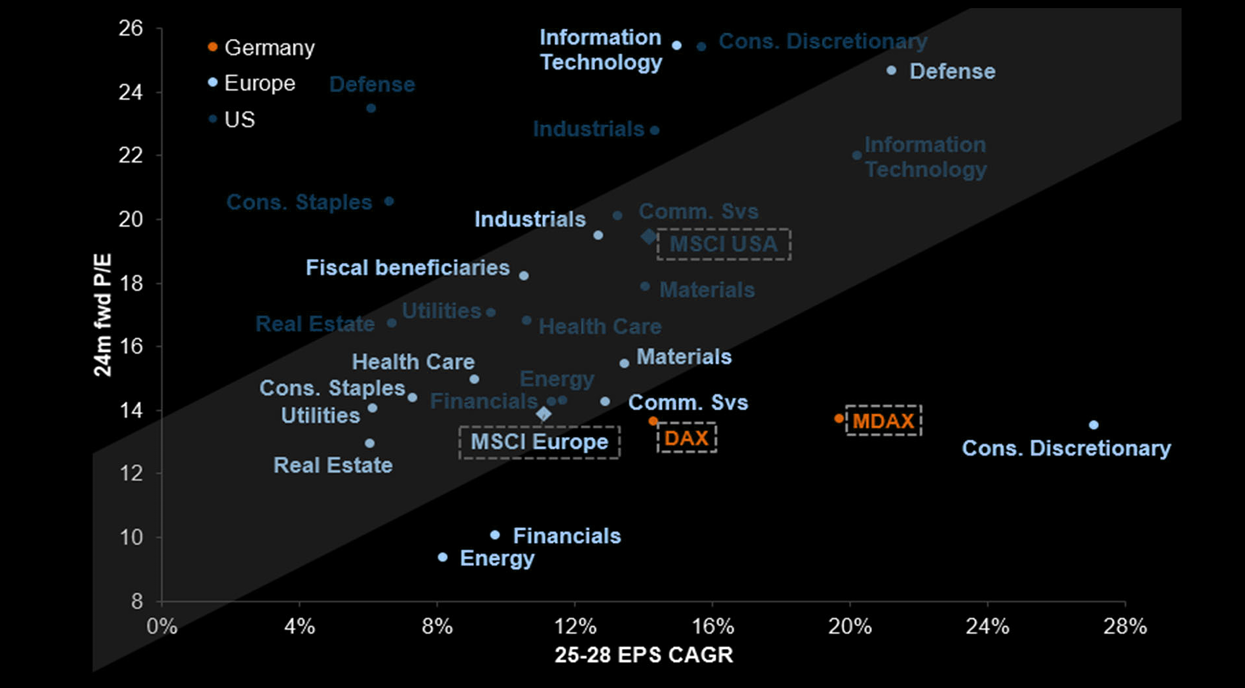

Cheap

German indices remain relatively cheap for their growth. Consensus forecasts 14-20% earnings CAGR over the next few years for Germany.

Source: Datastream

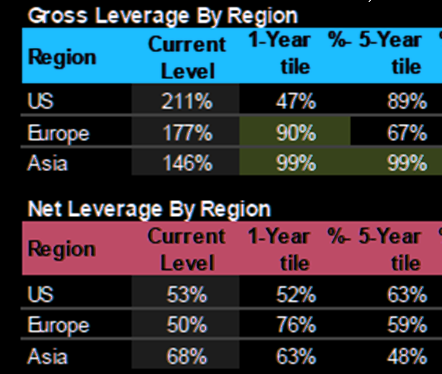

HF positioning

This is somewhat concerning. More "extreme" positioning in Europe than in the US for the first time "ever" (as measured by 1-year percentiles).

Source: MS Prime

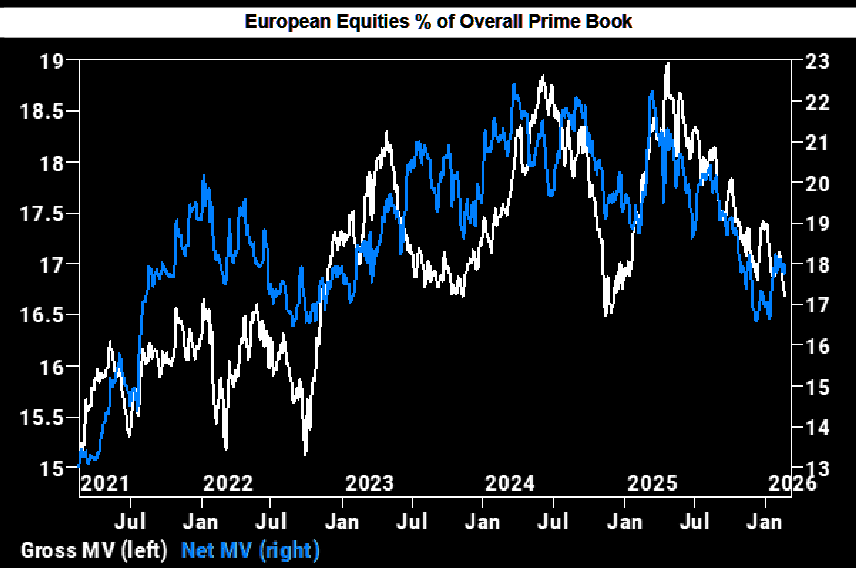

HFs losing their religion

HFs net sold European equities at the fastest pace in 5 months. The net selling was driven by long sales and to a much lesser extent short sales (5 to 1).

Source: GS Prime

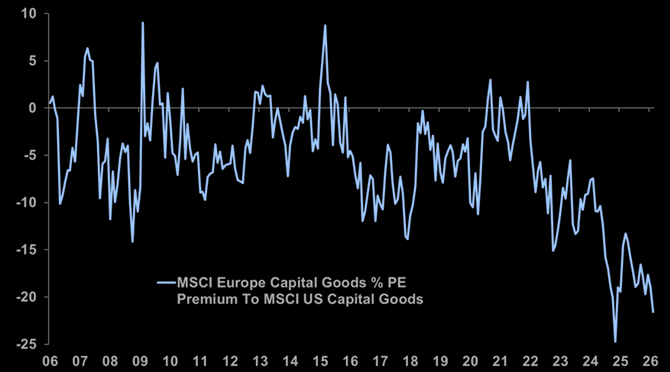

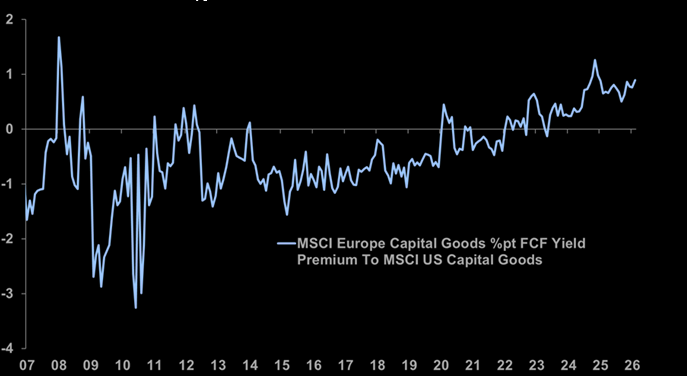

EU Industrials

EU Industrials sit at roughly a 22% PE discount to US peers, with capital goods offering about a full point higher free cash flow yield and ~30% discounts on EV-based metrics – levels rarely seen outside crisis periods. Macro signals are improving at the margin. Flash Eurozone composite PMI rose to 51.9, with manufacturing back above 50 and Germany leading. The UK printed a 22-month PMI high, strong retail sales, and a sizable budget surplus. ECB President Lagarde reiterated policy continuity through 2027. So, Europe might not be bracing for a storm – more like it’s waiting for confirmation the clouds are thinning. Valuations argue for upside, macro is stabilizing, but until earnings reactions normalize, it remains a selective opportunity set rather than a broad breakout. (Morgan Stanley)

Source: MS

Source: MS

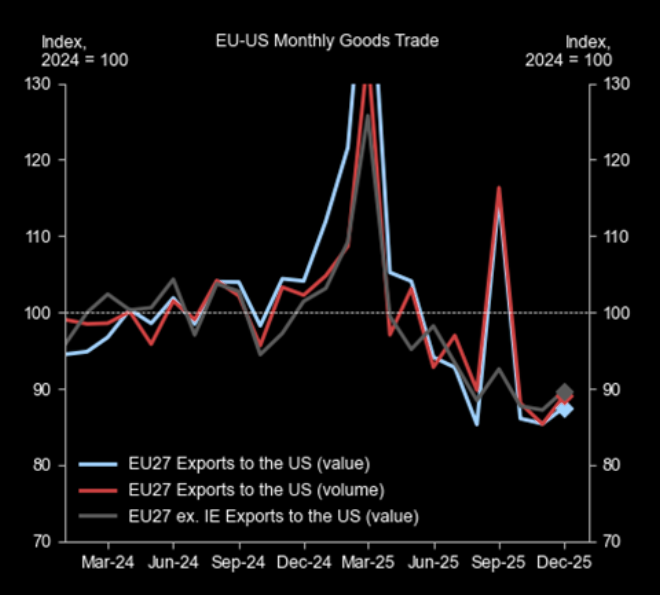

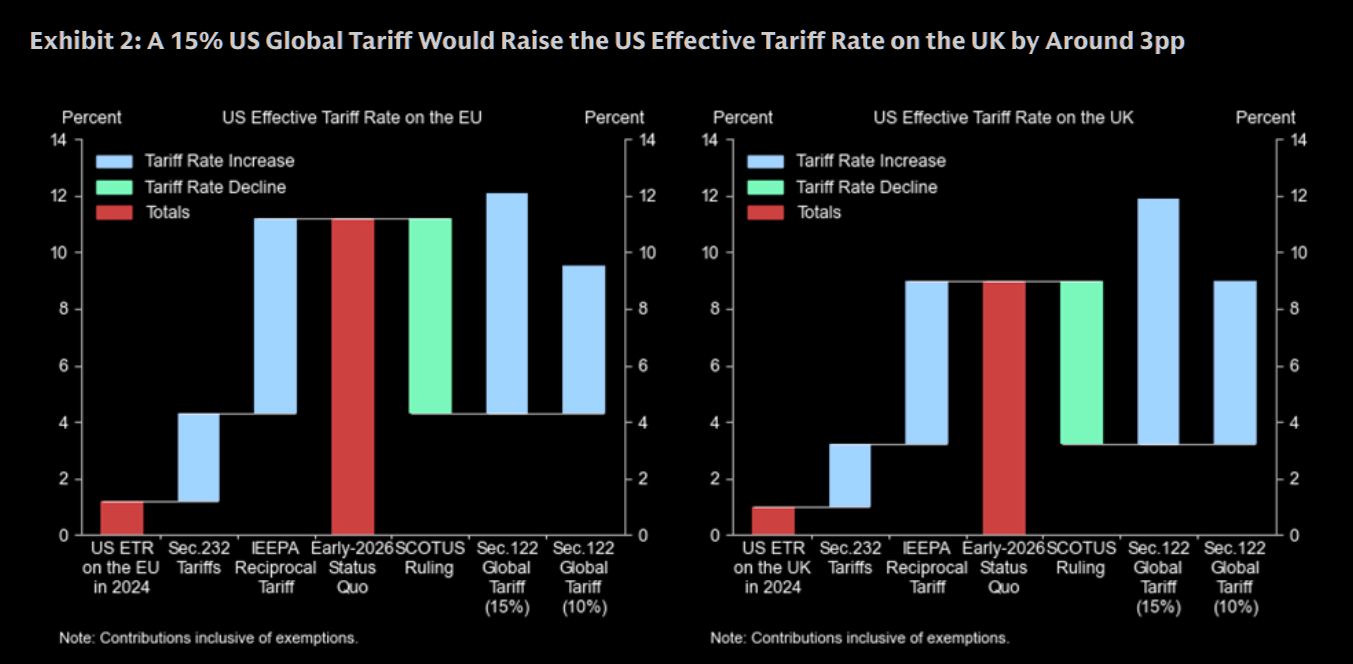

Those new Trump tariffs

Limited implications

"The replacement of IEEPA tariffs with a new 15% global tariff would raise the US effective tariff rate on the EU by 0.9pp to 12.1% and by 2.9pp to 10.9% for the UK but would be essentially neutral for Switzerland and Norway, although uncertainty remains elevated on a number of dimensions."

Source: Goldman

Uncertainty

"Uncertainty remains elevated on a number of dimensions. First, it is unclear whether the new 15% global tariff will apply also to countries that had struck deals for lower reciprocal tariff rates, such as the UK, or whether preferential treatment will be granted. This uncertainty could lead to strategic postponement of European shipments to the US and to higher volatility in exports data in the near-term. Second, it is unclear how European policymakers will respond to the recent policy announcements. Third, uncertainty remains on the tariff regime that could apply following the expiration of the new global tariff on July 24th." (Giovanni Pierdomenico, GIR)

Mostly behind us

The effect of existing US Tariffs on European exports has been mostly realized.