The Most Frustrating Market In Years

Grinding lower — but refusing to break

Markets are not crashing, they’re grinding. Hedging structures are failing, not because risk is low, but because the move is too slow. As volatility forces de-grossing, positions shrink and hedges get unwound, creating mechanical buying that cushions the downside. Flows, not fundamentals, are driving the market.

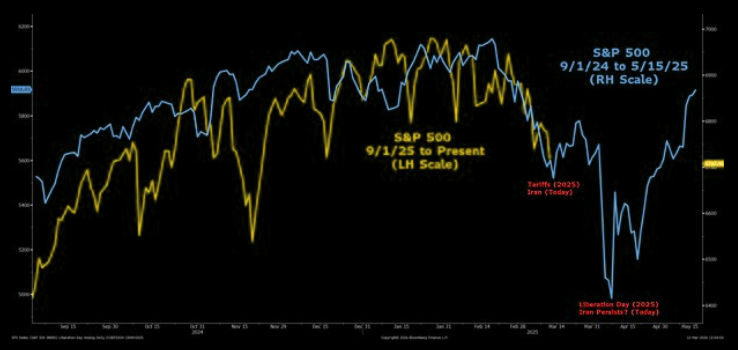

Following the path

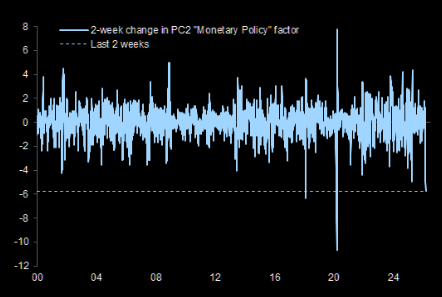

Morgan Stanley seems to find a similar déjà vu set up we have been talking about over the past weeks.

Source: MS

The grind that breaks hedges

Downside hedges are failing as the market grinds rather than crashes.

This slow bleed continues to weigh on already weak equity performance amid constant factor churn and reversals.

At the same time, high volatility is mechanically forcing de-grossing, shrinking positions across books. As exposure is reduced, those hedges are no longer needed and get unwound. The result is positive delta being bought back, creating offsetting flows that help cushion the downside and prevent a sharper sell-off. (McElligott)

Source: LSEG Workspace

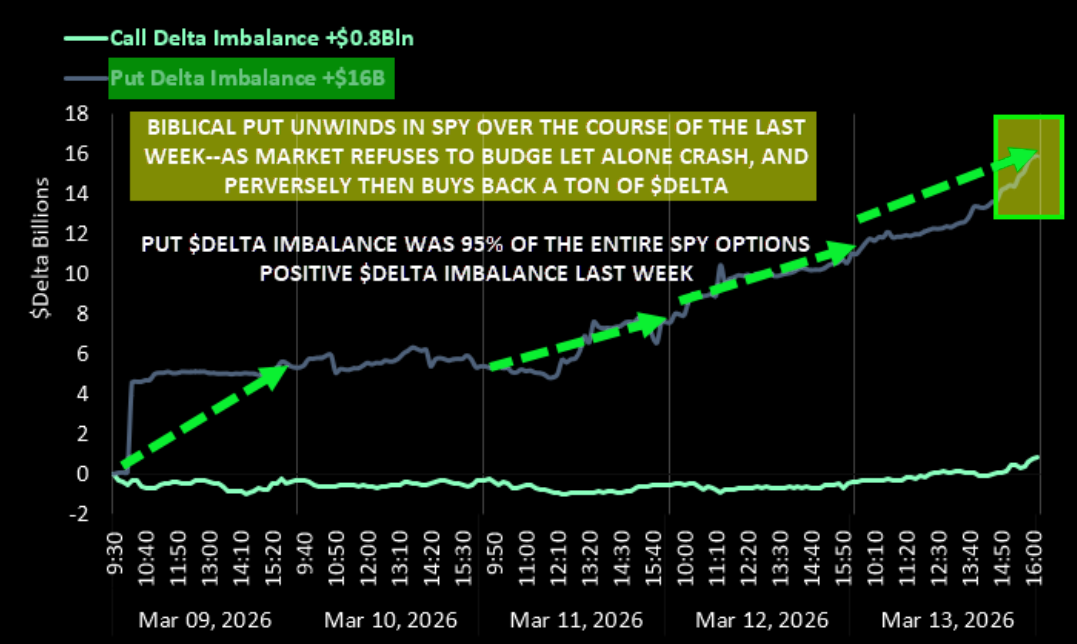

When puts don't kick in

Short-dated S&P downside hedges keep getting unwound in waves writes McElligott. As a proxy, last week’s net $delta imbalance in SPY options shows positive delta from sold puts massively outweighing call delta, as the market simply refused to crack.

At the same time, equities remain de-risked: lower gross and net exposure, heavy asset manager selling in S&P futures, and one of the largest one-week selling episodes on record (around the 1st percentile). Full note here.

Source: Nomura

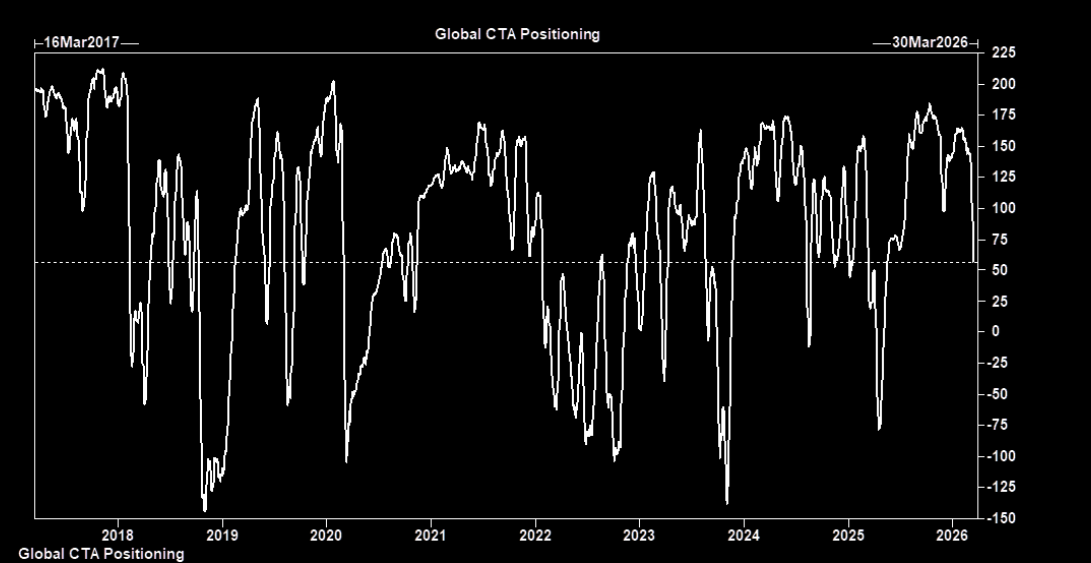

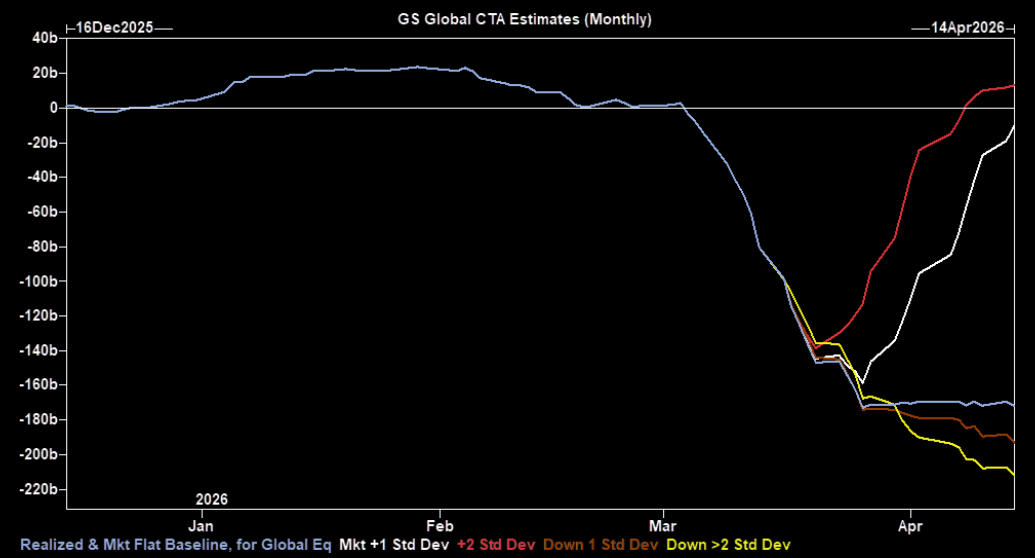

CTA positioning and flows

Goldman Sachs estimates the community has sold about $80bn of global equities over the past month, with CTAs and trend followers driving the bulk of the selling in the past week. In its baseline scenario, GS sees another $70bn of selling over the next week and roughly $100bn over the next month. Overall positioning has already dropped from above 8/10 earlier this year to around 6.5, and could move closer to 4.5–5 if those flows play out.

Source: GS

Source: GS

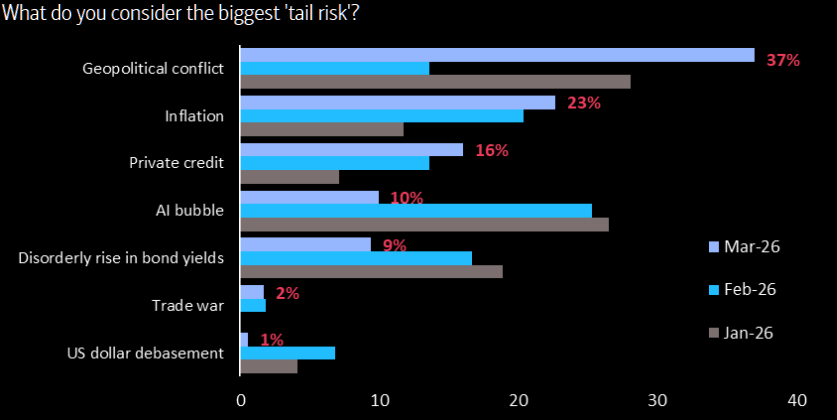

Geopolitics rising

Geopolitics is now the biggest tail risk according to the latest FMS.

Source: BofA

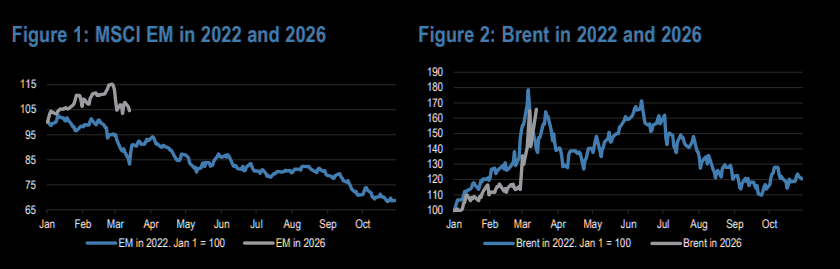

EM déjà vu?

Are we following the 2022 path?

If this resembles the Ukraine shock, oil may not fade quickly. Back then, Brent didn’t return to its Jan 1 level (~$77/bbl) for nearly a year, while EM fell over 30% from the peak.

Today, we’re only ~9% off recent highs, leaving room for further downside. The risk may even be greater given the stronger run-up into 2025 (+31% vs. -5% in 2021), as higher starting points tend to mean heavier downside tails.

There’s also upside tail risk: a prolonged Strait closure could send oil sharply higher. Recall Brent exceeded $130 in 2008 (~$200 in today’s dollars) without a full disruption (JPM macro).

Source: JPM

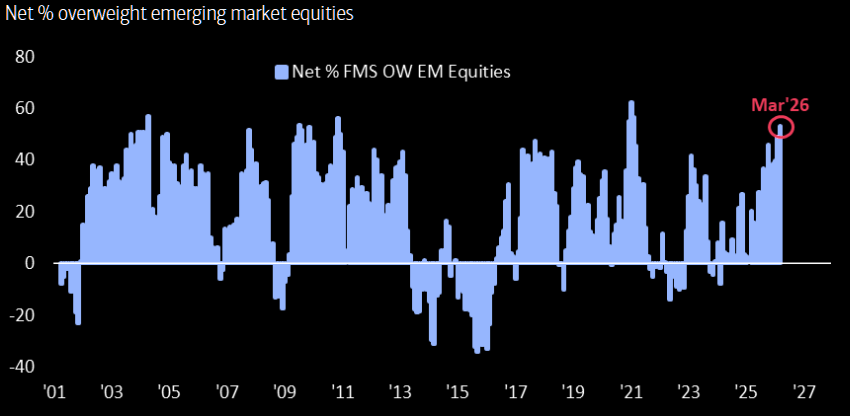

EM love is huge

Allocations to EM at the highest levels since Feb 2021. What could possibly go wrong? Latest note on EM here.

Source: BofA

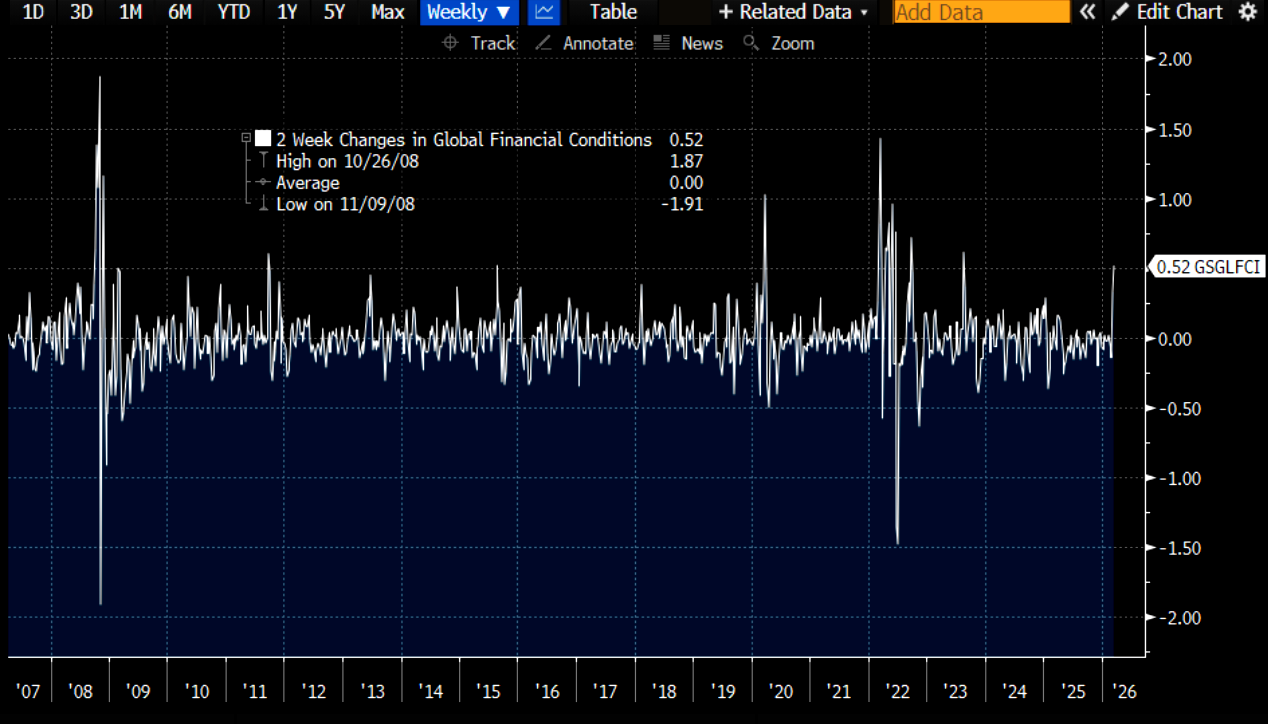

Tighter financial conditions

The biggest development over the past two weeks has been the sharp tightening in global financial conditions. The GS Global FCI has risen more than 50bps over that span – the strongest tightening impulse since August 2023 and one of the largest moves outside of true crisis periods.

Source: Bloomberg

Sharp hawkish repricing

The last 2 weeks saw one of the sharpest hawkish re-pricings since 2000. More on the tightening shock here.

Source: Goldman

Credit is getting attractive

The recent widening means current levels are starting to look attractive. Spread to benchmarks and ASW spreads are at the widest levels in over eight months and credit yields are now at the highest levels in 20 months. If the conflict is set to be short lived, these levels are becoming very attractive. This is the opportunity within the grind. More on credit here.

Source: Soc Gen Cross-Asset

Main takeaway

Despite all the stress, markets continue to absorb selling without breaking. Until a real macro shock hits, expect grind, not crash.