Oil Volatility Explodes As Markets Brace For A Bigger Shock

Welcome to pure panic

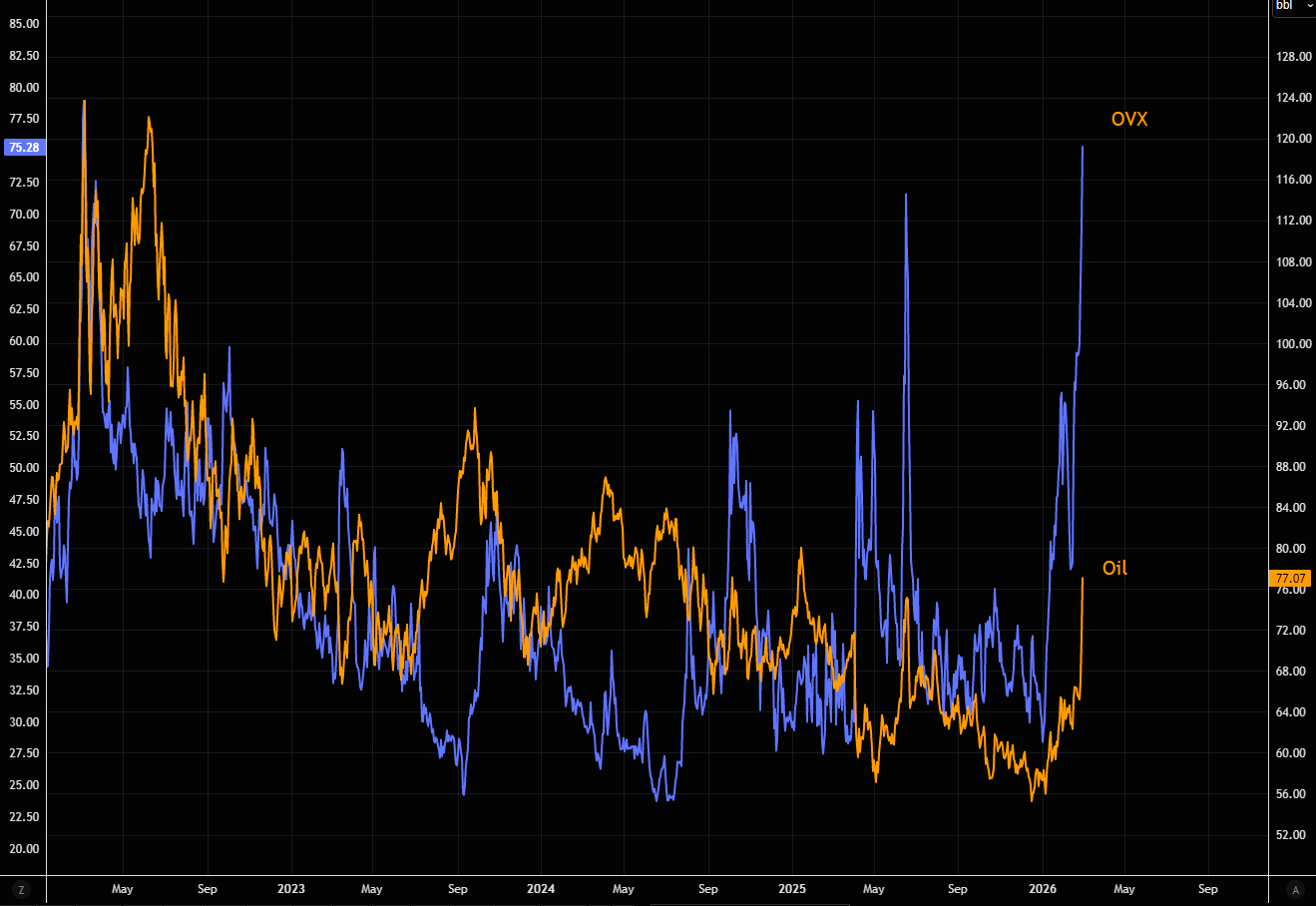

Oil volatility is surging. With OVX at current levels, the market is pricing roughly 4.7% daily moves in crude. That’s not normal volatility, it’s a market bracing for disorder.

Chart 2 shows OVX has only traded higher twice since oil’s “negative dive”, underscoring just how extreme the current move is.

Source: LSEG Workspace

Source: LSEG Workspace

Not calibrated for that timeline

Oil is trading well above the downtrend line that has been in place since September 2023. The 50-day moving average is now close to crossing above the 200-day.

Goldman's Privorotsky sums it up well: "Unless there is outright regime collapse, the asymmetric risk of even a partial closure can embed a structurally higher oil price. Trump suggested operations could last 4 to 5 weeks. I do not think markets are calibrated for that timeline".

Source: LSEG Workspace

That was quick

Oil is now at its most overbought levels since March 2022. RSI 79.

Source: LSEG Workspace

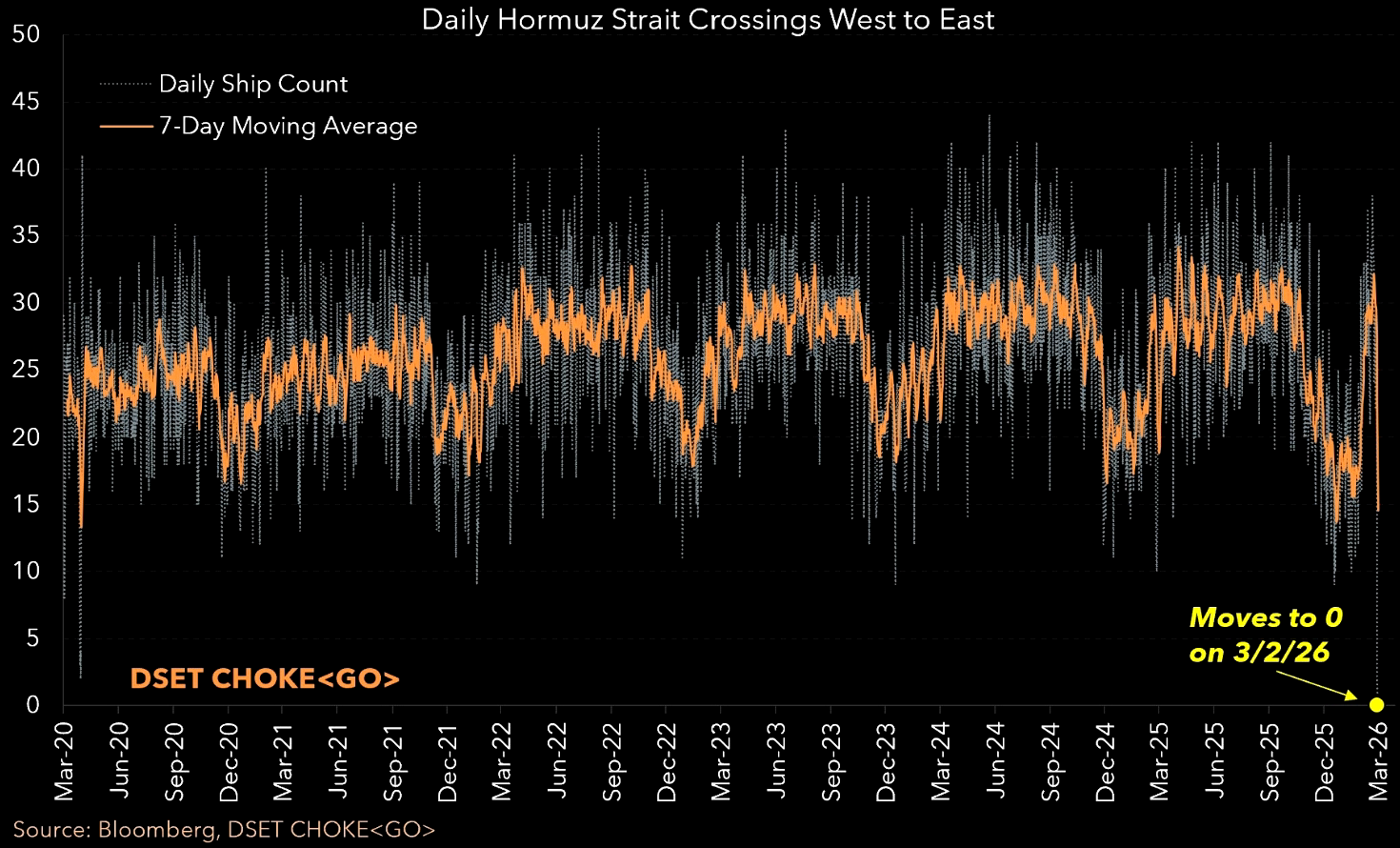

Zero

Strait of Hormuz traffic drops to zero.

Source: Bloomberg/@M_McDonough

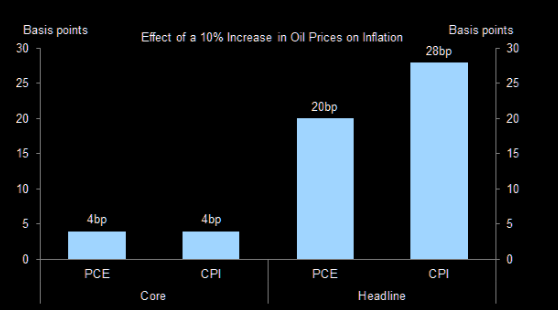

Oil and inflation

Higher oil prices feed directly into consumer energy costs. As a rule of thumb, a sustained 10% rise in oil tends to lift core CPI by around 4 basis points and headline CPI by roughly 28 basis points, writes GS.

In the baseline scenario, assuming oil follows their commodities team’s forecasts, year-over-year headline CPI is expected to edge up from 2.4% in January to 2.7% in May, before easing back to 2.0% by December 2026.

If oil prices remain elevated for longer, however, headline CPI could rise to around 3.0% in May and stay above the baseline path for the rest of the year.

Source: GS

The inflation gap

That oil vs US 10 year breakevens gap...

Source: LSEG Workspace

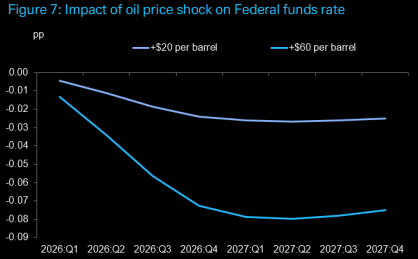

Oil and Fed

The recent rise in oil prices is likely to have only a modest impact on the broader economy, slightly weaker growth and marginally higher unemployment according to DB. The main effect would be on headline inflation, which could be viewed as transitory. However, if oil moves significantly higher, the economic impact would increase accordingly.

Fed models suggest such a shock would warrant a somewhat more dovish stance, with 10-year Treasury yields broadly tracking that response. The key variable is inflation expectations. After years of above-target inflation, persistently high energy prices risk unanchoring expectations. As a result, elevated oil prices are likely to reinforce the Fed’s current “wait-and-see” approach.

Source: DB

Rates disconnect

Oil vs US 10 year gap very wide. If oil stays here, something else has to move.