Putin’s Ghost Haunts Europe Again—But The Setup Isn’t 2022

Putin's power

Markets are once again whispering the same word that haunted investors in 2022: energy. Putin’s geopolitical shadow is creeping back across European assets, but this isn’t the same setup. Gas prices are far below crisis peaks, earnings revisions remain positive, and Europe may be less fragile than the trade assumes.

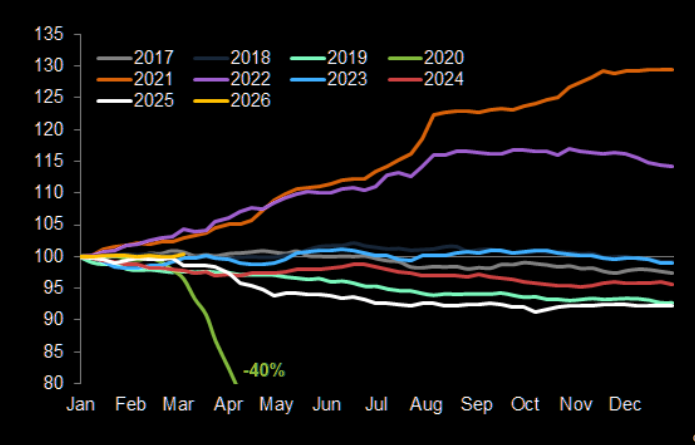

The hit in 2022

The de-rating in Europe was especially sharp in 2022.

Source: Datastream

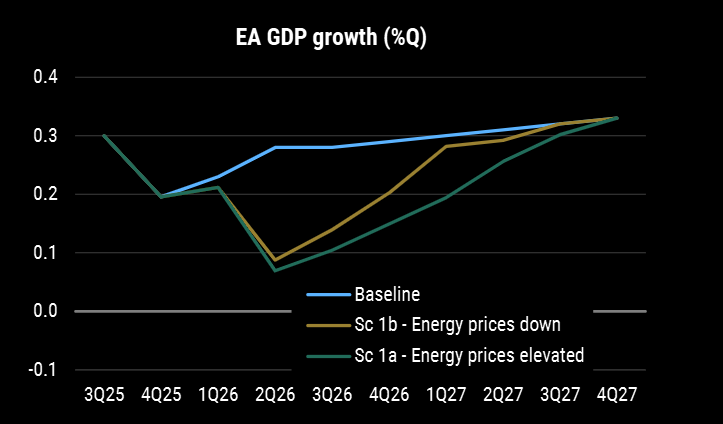

That GDP hit

Higher oil prices would be weighing on GDP growth for several quarters.

Source: Morgan Stanley

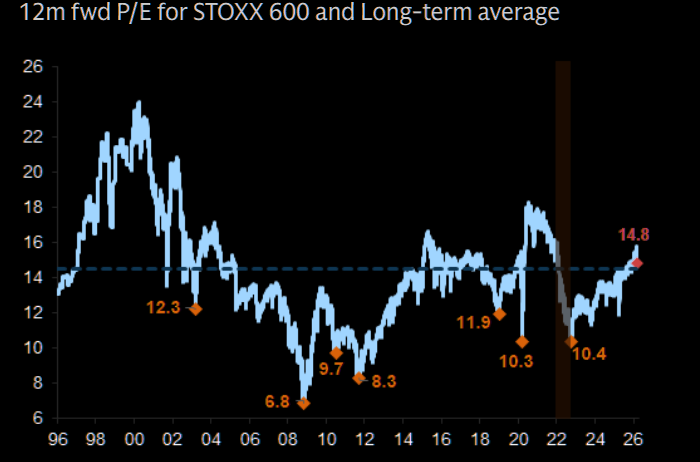

Not cheap this time around

Europe is trading at the 84th percentile of its historical valuation range.

Source: Datastream

Still cheap vs US

Europe trading at a deep discount to the US. Europe relative to US 12m forward P/E.

Source: Datastream

This looks vulnerable

Flows into cyclicals have been strong, again increasing vulnerability.

Source: EPFR

Some growth (to erase)

GS: "We forecast STOXX Europe 600 EPS growth at 5% and 7% in 2026 and 2027."

Who would be surprised if this mid single digit growth ends up at zero?

Source: Haver

Numbers actually up

There has actually been an upward revision of earnings for European companies since the start of the conflict. Chart shows EPS revision since start of the conflict (26th Feb, 2026).

Source: Datastream

2022 revisions

2022 was one of the best recent years in terms of upwards earnings revisions.

Source: FactSet

A 10% rise

A 10pp rise in Brent boosts SXXP annual EPS growth by 2pp, but lower growth would be an offset.

Source: Goldman

TTF well below

TTF natural gas prices remain well below their peak of 2022.

Source: Morgan Stanley

Consumers

Consumer confidence took a real hit in 2022 but adjustment of actual spending was much more progressive.