Volatility Shock: Panic Is Spreading

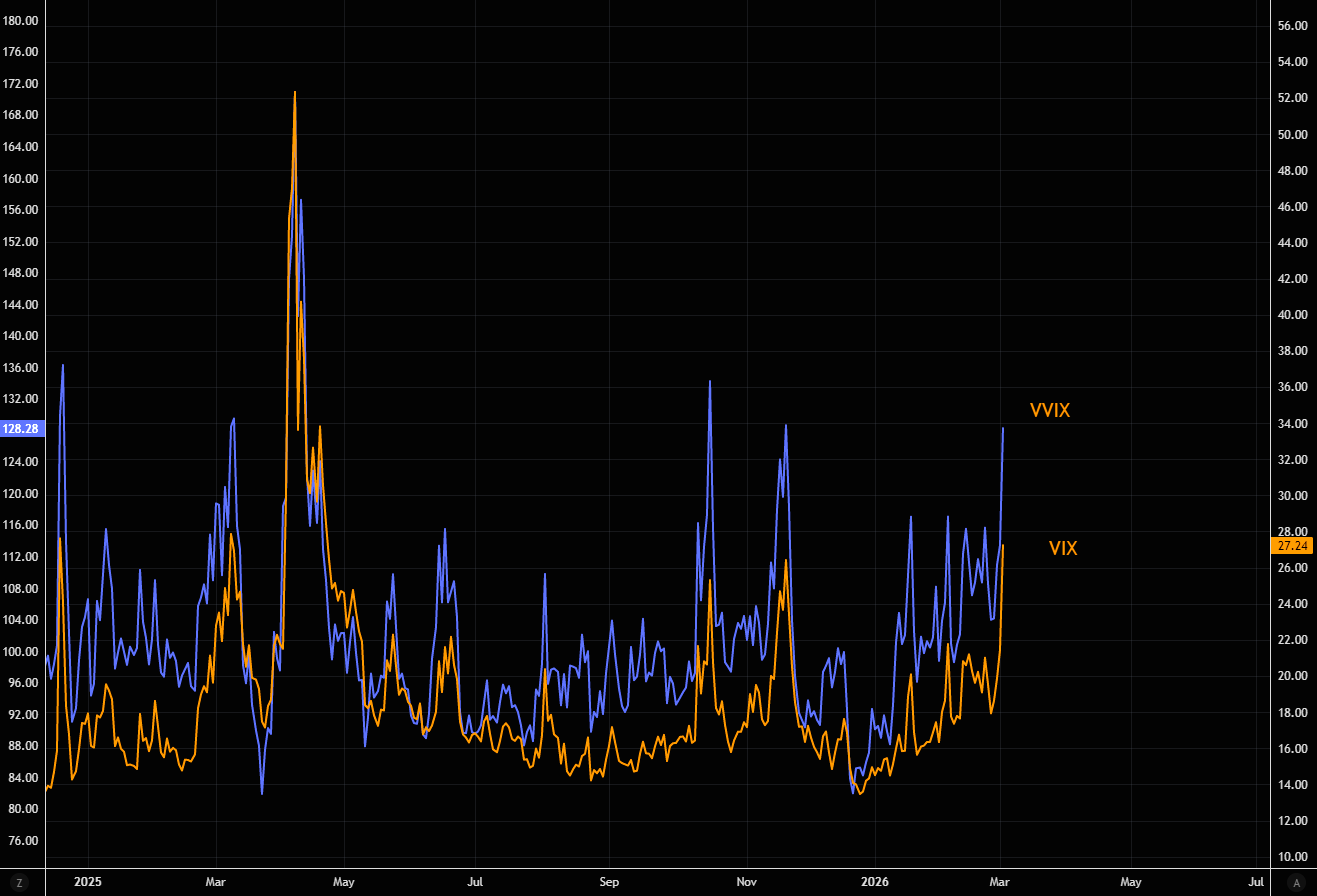

Say hello to panic

VVIX at 128 and VIX at 28 is not a normal market backdrop.

We outlined our VIX framework a few weeks ago, and the seasonal pattern (see chart 2) has played out well so far. That said, the setup becomes more complex from here.

Volatility shocks like this typically take time to unwind. But chasing volatility at these levels only makes sense if you believe a crash is imminent.

Source: LSEG Workspace

Source: Equity Clock

Violent VIX

The reaction in VIX has been rather aggressive so far. SPX vs VIX (inverted) chart for some perspective.

Source: LSEG Workspace

FOMO Momo Flush

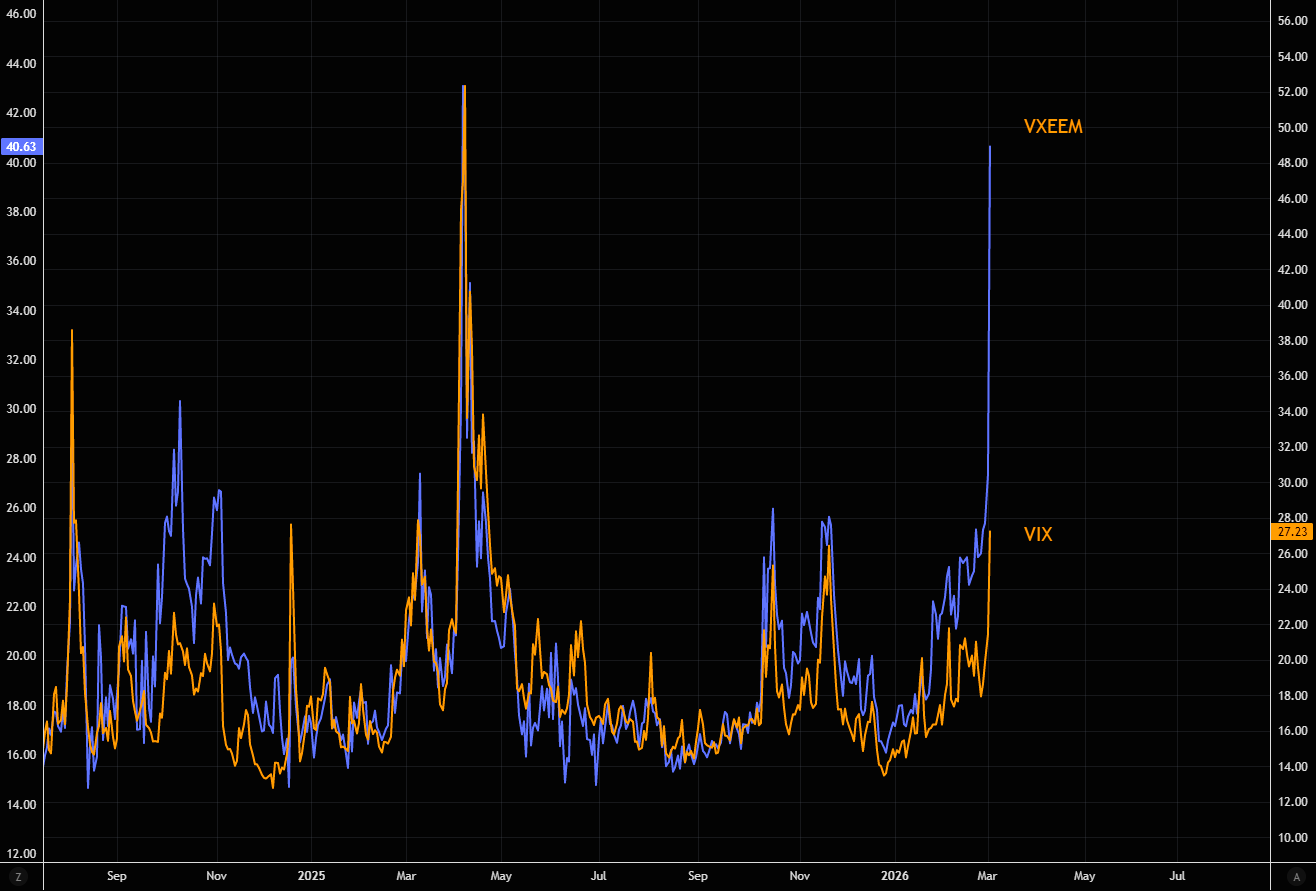

If you think the VIX has moved, take a look at EM “VIX”, VXEEM.

Emerging markets attracted plenty of late-cycle chasing from investors who didn’t fully understand what they were buying, nor what EM risk really entails.

You know the EM space is in full panic mode when the VIX spike looks tiny in comparison.

Source: LSEG Workspace

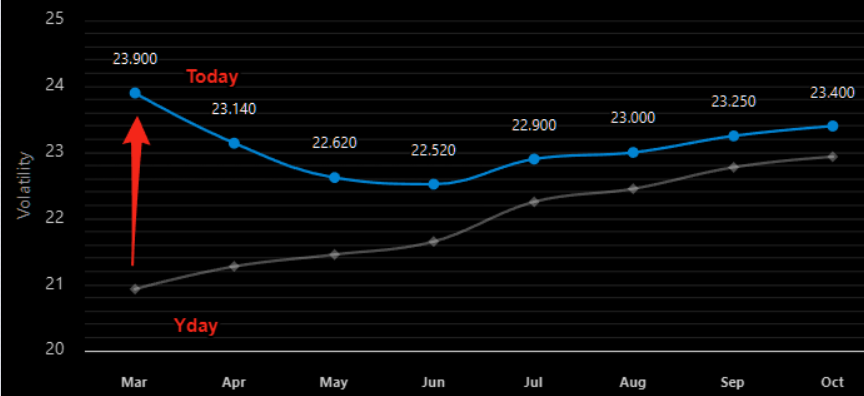

Panic in the structure

The VIX term structure is shifting aggressively higher, particularly at the front end of the curve. That’s where protection gets bid first when panic sets in.

Source: VIXcentral

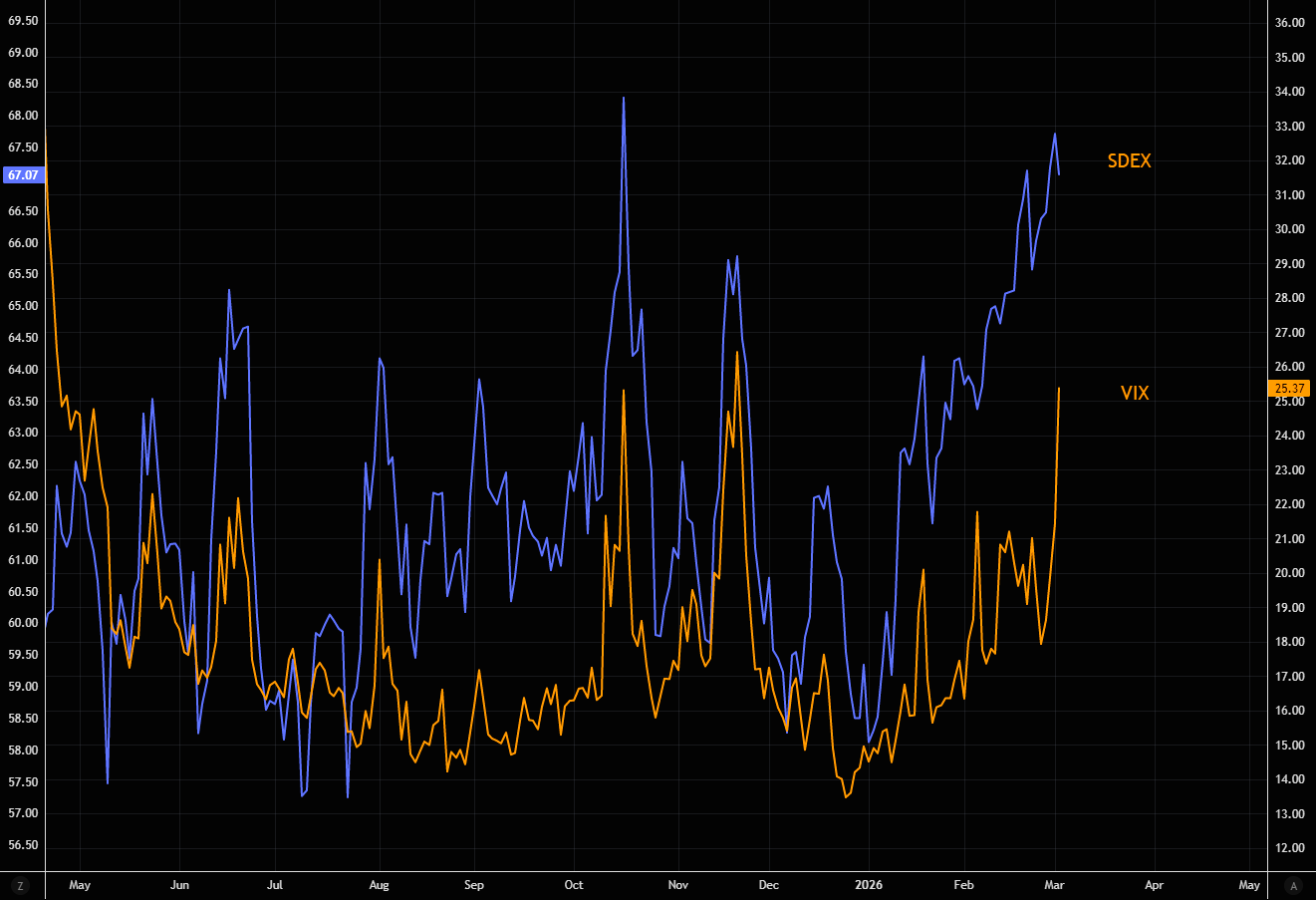

Green shoots?

VIX is exploding higher, yet SDEX is actually slightly down on the day.

That divergence is notable. If skew isn’t rising alongside spot volatility, it suggests panic demand for tail protection isn’t accelerating further.

Are we seeing the first signs that this latest volatility spike may be nearing a pause?

Source: LSEG Workspace

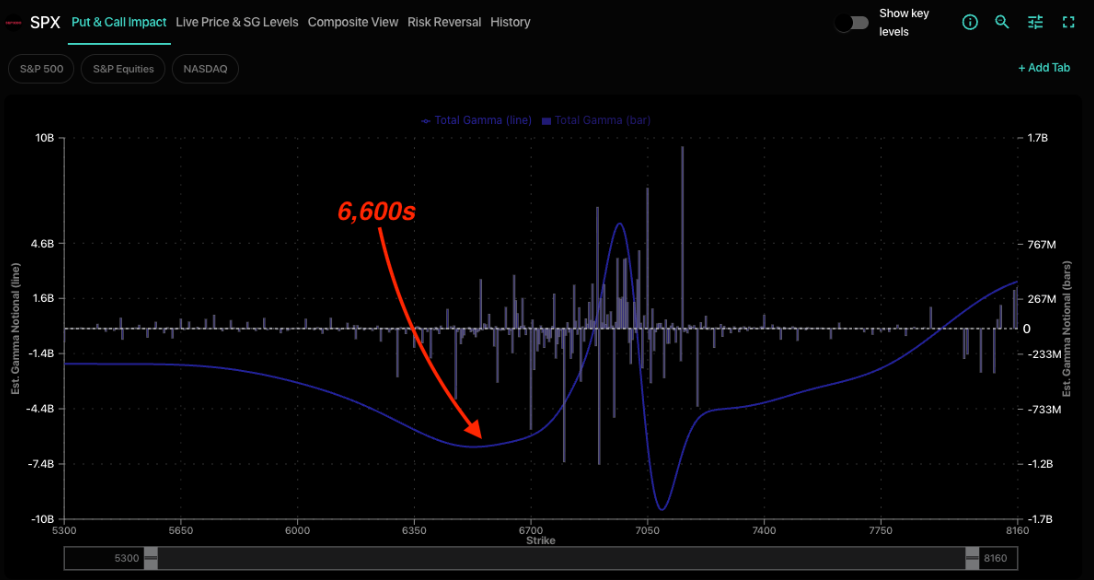

Gamma

Negative gamma still troughs in the 6,600s, and a move toward that area would likely coincide with VIX pushing closer to 30. That’s where equity re-entry becomes more interesting in Spotgamma's view as downside negative gamma exhausts and the volatility risk premium (VRP) potentially becomes attractive.

With that in mind, the 6,600s is the zone where selectively adding long delta exposure could make sense. Until then, Spotgamma remains in the “sell the rip” camp rather than buying dips.

Notably, yesterday’s dip was bought aggressively, but the flow was dominated by put selling. Put selling is effectively short covering, and rallies built on short covering tend to be unstable. This is stress, not yet capitulation.