Yet Another "Annus Horribilis" For Europe

The bid disappeared

The tone has shifted from uneasy to fragile as the Middle East conflict continues to cast a longer shadow over the region. What initially looked like a relatively contained drawdown started to give way, with flows, headlines, and a clear reluctance to hold risk into the weekend all leaning the same direction. And when the bid disappears, it doesn’t take much to push things lower.

Source: LSEG Workspace

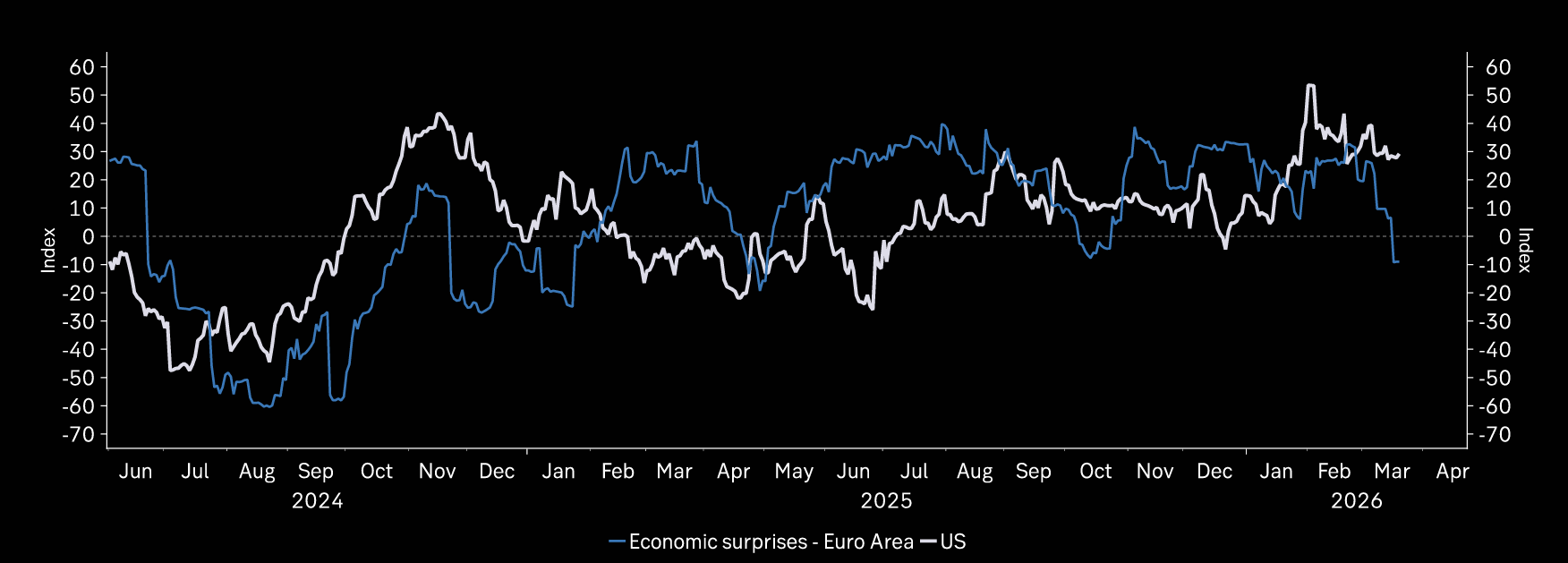

ECB stagflation dilemma

Macro surprises have turned negative in Europe, but so far, they remain resilient in the US.

Source: Macrobond

Inflation expectations

Inflation expectations have moved far more in Europe.

Source: Macrobond

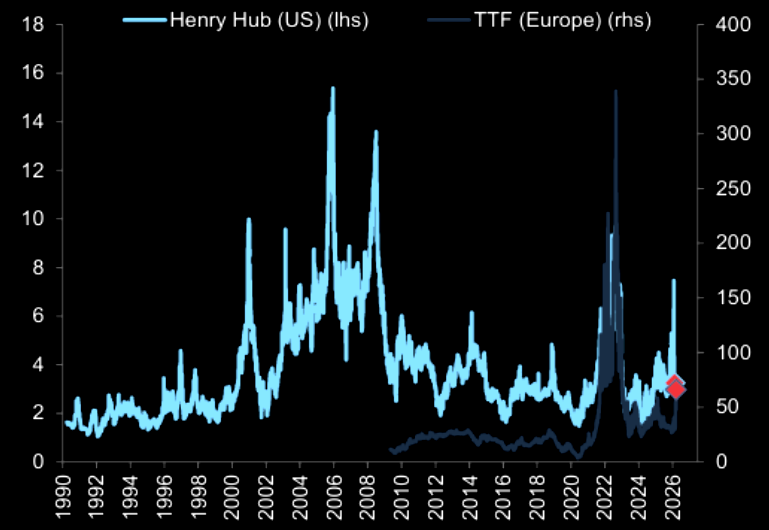

Gas

European natural gas prices have nearly doubled since the conflict began, while US prices have risen only ~11%.

Source: GIR

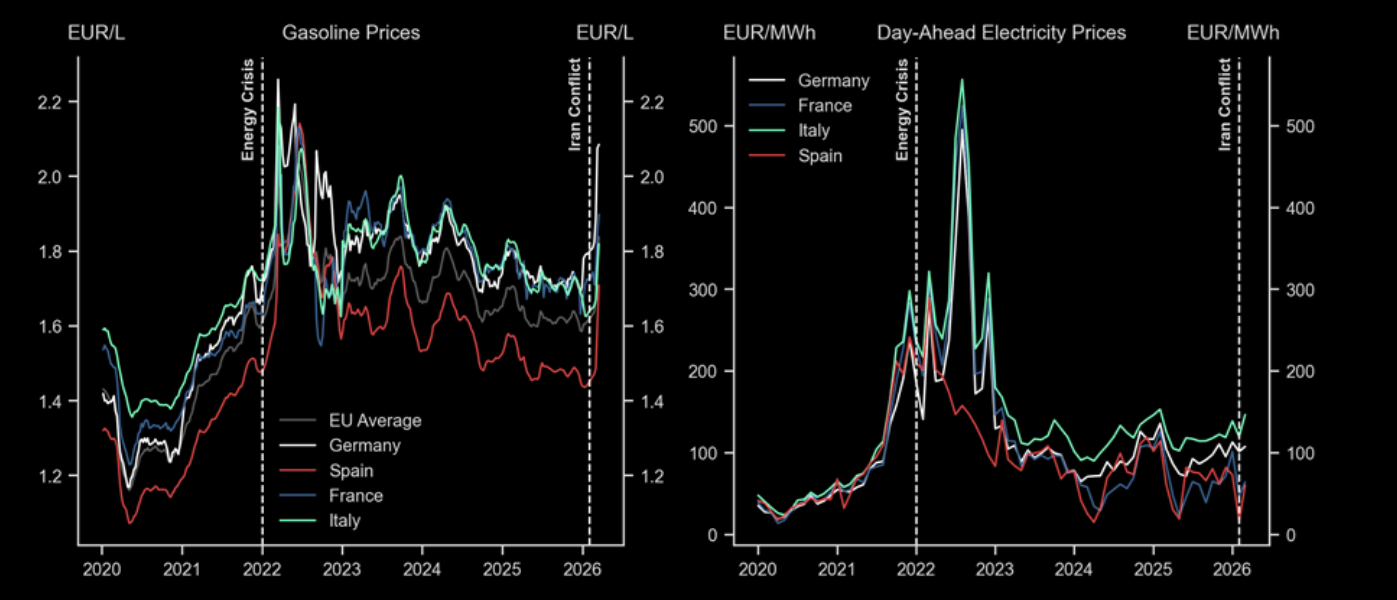

Energy prices

Consumer energy prices sharply up but not uniformly across Europe.

Source: Haver

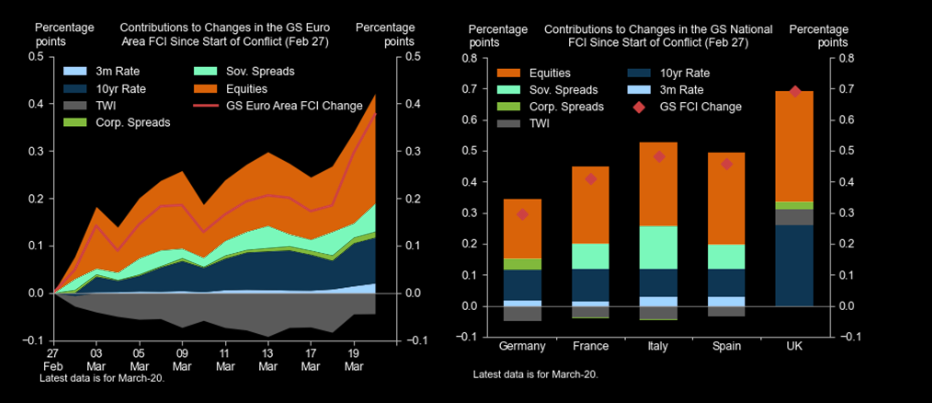

Tightened

Euro area FCIs have tightened by around 40bp since the start of the war.

Source: Goldman

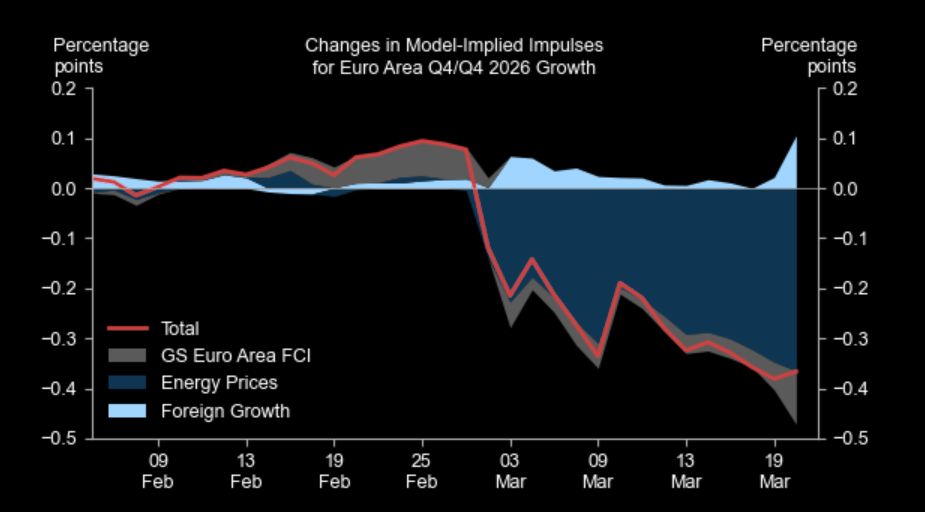

Not what the continent needed

GS: "Our model points to a 0.4pp drag on growth this year from the energy shock."

Source: Goldman

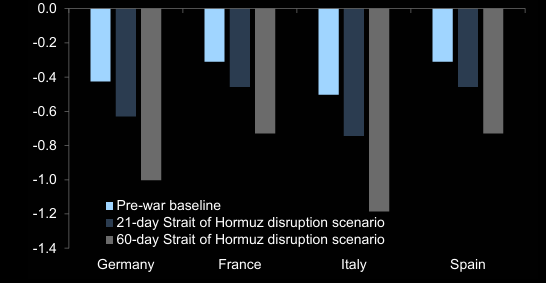

Energy price shock to growth

Model-implied peak effect of energy price shock on the level of real GDP vs. pre-conflict baseline, %.

Source: GIR

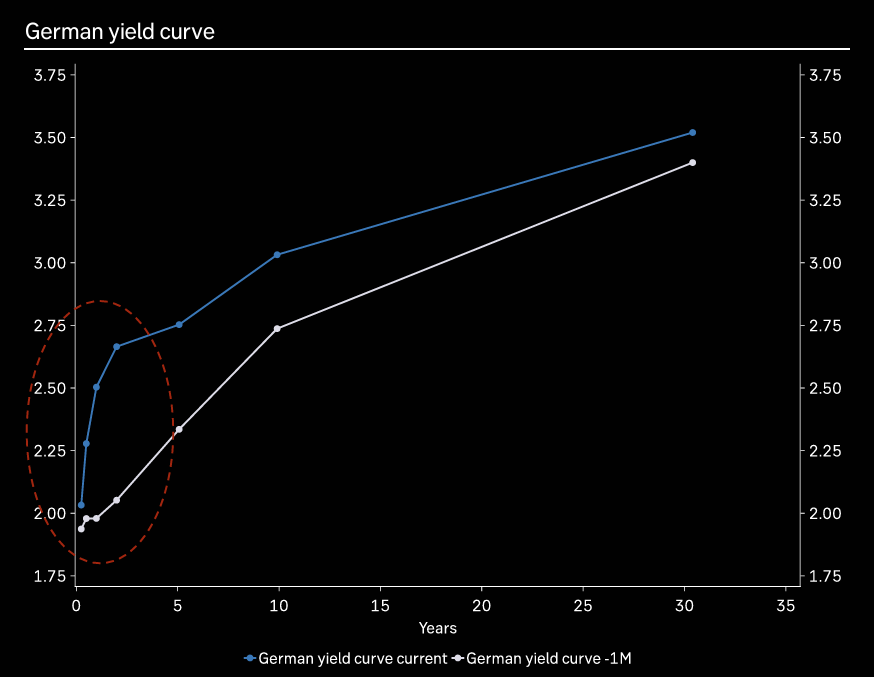

Steepens / flattens

European 0-2 year yield curve steepens sharply, while the 2-30 year curve flattens.

Source: Macrobond

Source: Macrobond

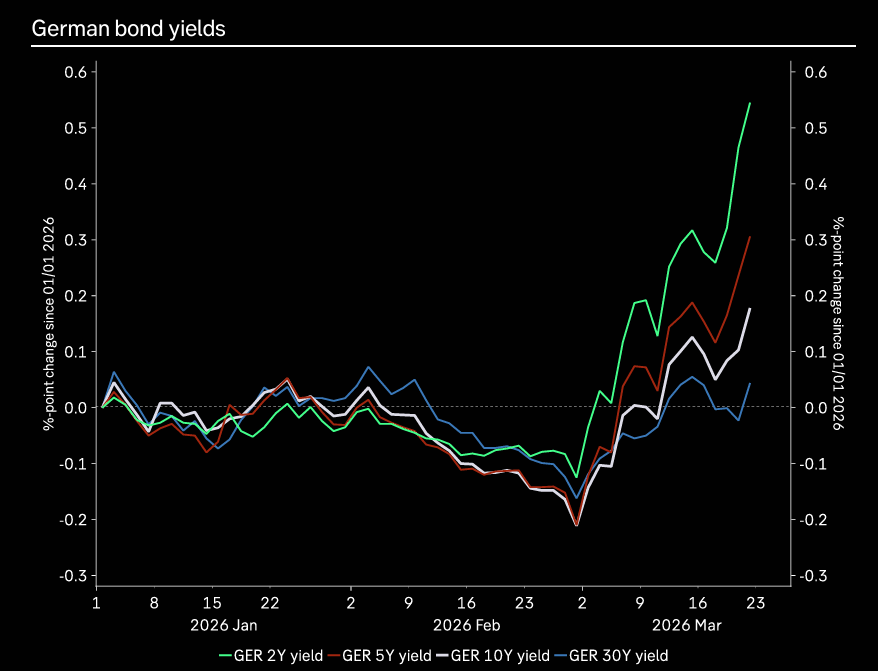

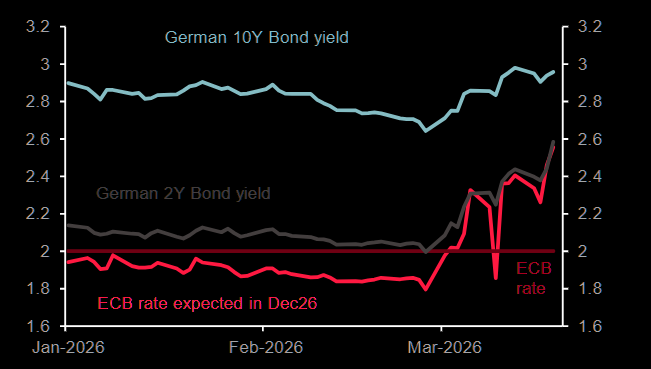

Lifting the entire yield curve

ECB repricing has been lifting the entire yield curve.

Source: Soc Gen

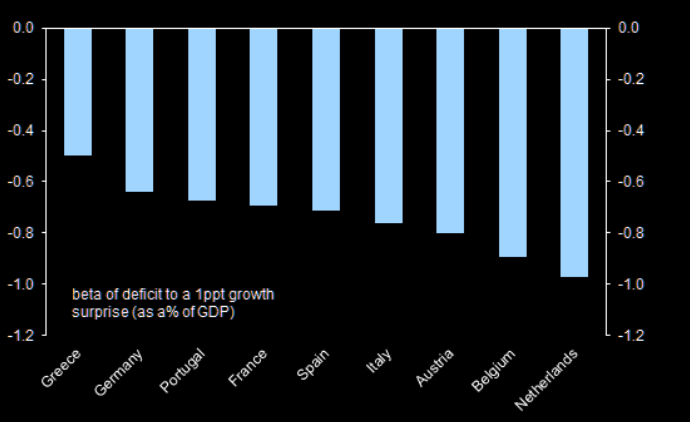

Deficits

Weaker growth typically leads to wider deficits.

Source: European Commission

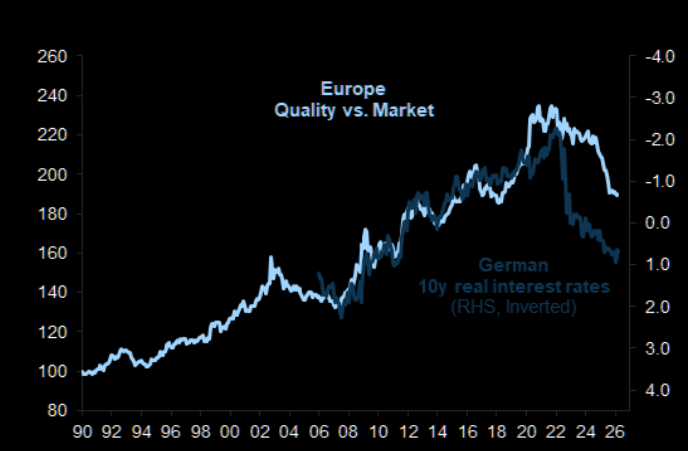

European "quality"

Quality stocks in Europe have significantly lagged the broader market recently.

Source: Datastream

Least eager

Europe doesn’t have a structural growth story to fall back on – no AI cushion, no obvious cohort to absorb flows when macro pressure builds. Positioning reflects that reality: selling has picked up, but similar to other regions it feels more like a lack of conviction, with growing interest in hedges underscoring the discomfort. Add in a macro backdrop where central banks risk tightening into a potential growth shock and the setup looks increasingly asymmetric. For now, Europe isn’t just lagging… it’s the part of the bracket investors seem least eager to bet on.